By Roberto García-Castro and Dr. J. Mark Munoz

AI technologies are spreading fast across industries, but adoption varies widely. This article helps managers understand where and how AI is gaining ground across the main U.S. industries in the 2020-2024 period, based on large-scale textual analysis of annual corporate 10-K reports.

Introduction

The increasing relevance of artificial intelligence (AI) and data-driven technologies across sectors has prompted growing interest in measuring their adoption across firms and industries (Cockburn, Henderson, and Stern, 2018). While anecdotal evidence points to the widespread integration of analytics, machine learning, and automation into business models, systematic evidence remains limited, particularly outside of the technology sector (Seamans and Raj, 2018).i

This article explores AI-related adoption patterns across US industries between 2020 and 2024, using a large-scale textual analysis of 10-K filings. By tracking the frequency of AI-related keywords in regulatory filings submitted to the Securities and Exchange Commission (SEC), the authors constructed a novel, replicable dataset that offers insight into how different industries disclose and potentially adopt AI technologies over time. The dataset consisted of annual 10-K filings from 7,883 unique US firms, downloaded using the Edgar package in R, which interfaces with the SEC’s EDGAR system. The filings span the years 2020 through 2024 and are parsed as plain text for computational efficiency. Each filing is tagged with its firm’s industry using standard SIC codes, which we mapped to broad industry categories for visualization purposes. In total, we analyzed 131,603,450 words in all US filings available in the EDGAR system. The average 10-K filing contained 23,037 words of text.

The methodology builds on prior work that uses natural language processing (NLP) techniques to study digital transformation (Chen and Srinivasan, 2020; Li, 2010). Specifically, the authors follow a keyword-based approach to proxy for firms’ engagement with AI, drawing on terms such as analytics, automation, big data, cloud, and machine learning. These keywords, drawn from both academic and consulting literature (Bughin et al., 2017), represent complementary dimensions of what is often broadly referred to as AI. The attached heat map visualizes the result of this exercise and reveals patterns in the diffusion of AI-related discourse across industries and years, highlighting both the heterogeneity in adoption and the concentration of AI-related language in certain sectors.

Increase in Ai Engagement and Diversity of Industry Usage

Following existing literature on digital adoption (Chen and Srinivasan, 2020), we define a dictionary of AI-related terms covering six core categories: AI, analytics, automation, big data, cloud, and digitization. The dictionary with the keywords used is shown in Table 1 below.

This set of keywords aimed to capture different dimensions of how firms discuss the integration of AI-related technologies into their operations. We also included a composite count (“total”) that aggregates the count from all categories.

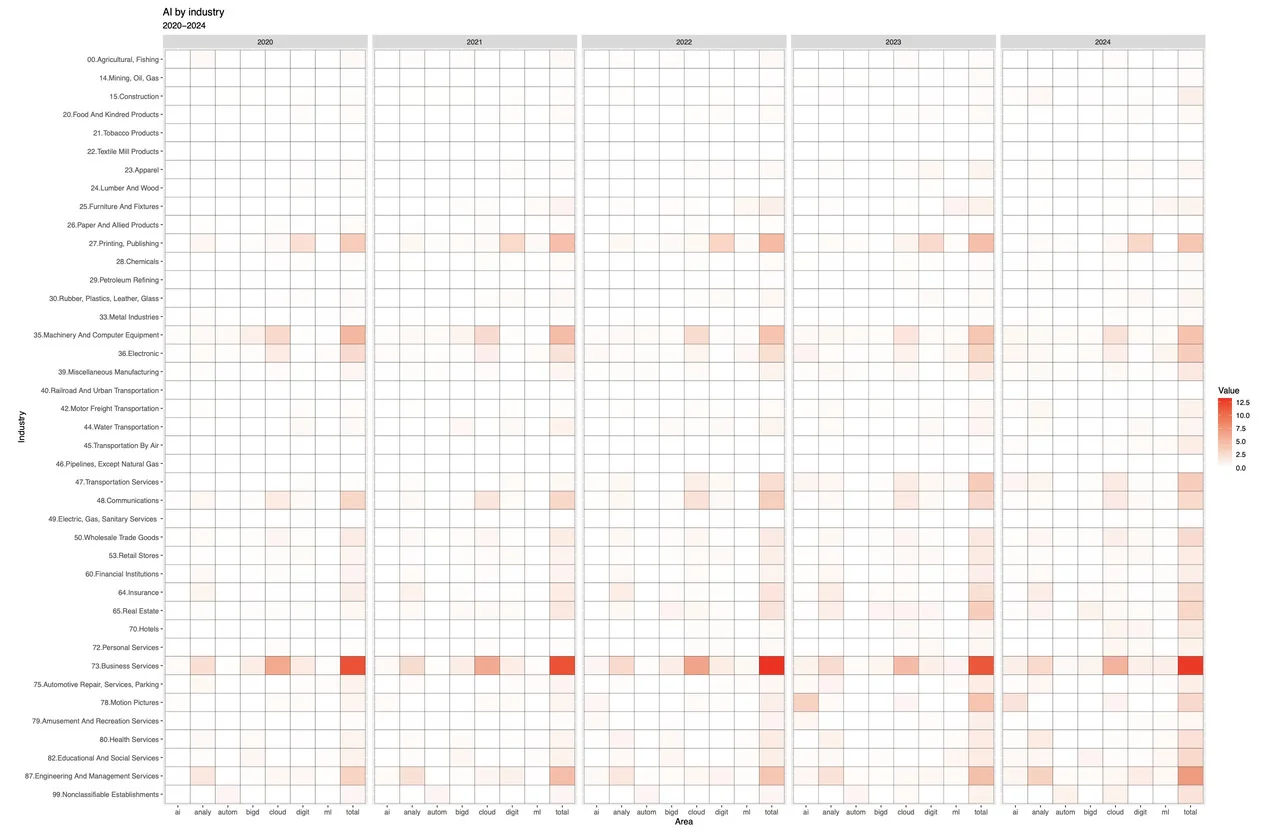

Keyword mentions are counted in each firm’s 10-K text using regular expressions and aggregated by industry-year-category, resulting in a three-dimensional matrix. Figure 1 next page shows the intensity of keyword usage across time, industry, and AI dimension. Industries are arranged vertically, and AI categories are horizontally, with separate panels for each year from 2020 to 2024. Color intensity indicates the log-transformed frequency of keyword mentions, normalized by the number of firms in each industry-year cell. The higher the color intensity, the higher the adoption of the technology in that industry year.

The results shown in Figure 1 reveal clear and increasing engagement with AI-related terminology over time, though unevenly distributed across sectors. Between 2020 and 2024, there was a general increase in mentions across all keyword categories, indicating growing awareness or adoption of digital technologies. The total keyword count shows a marked increase in intensity in the Business Services and Engineering and Management Services sectors, consistent with these sectors’ role in IT, consulting, and optimization. The machinery, computer equipment, and electronics sectors also show an increasing use of AI language, particularly in the context of automation, AI, and cloud technologies. Financial institutions show occasional spikes, particularly in analytics and big data, reflecting their investment in data-driven risk modeling and algorithmic trading. In contrast, traditional industries such as agriculture, mining, and lumber show minimal activity, possibly reflecting slower digitization trajectories or less public discussion of AI in filings.

The limited presence of AI-related activity in the air and railroad transportation sectors is a noteworthy finding. These industries operate under stringent regulatory oversight, where safety, reliability, and compliance are of paramount importance. The integration of artificial intelligence technologies in such contexts often encounters regulatory resistance and protracted certification processes, which can hinder adoption timelines and diminish the likelihood of prominent disclosure in official filings such as 10-K reports. Historically, firms within these sectors have been laggards in the adoption of digital technologies, including AI, which has contributed to persistent challenges in customer experience, operational efficiency, and profitability.

As firms adapt to e-books, online journalism, and on-demand printing, they increasingly adopt technologies such as cloud computing, automated workflows, and digital content management systems.

Our results also underscore the ongoing digital transformation of the printing and publishing industry, shifting from traditional print to digital platforms. As firms adapt to e-books, online journalism, and on-demand printing, they increasingly adopt technologies such as cloud computing, automated workflows, and digital content management systems—all of which are commonly linked with AI-related terminology in 10-K filings.

Another notable pattern is the consistent adoption of AI-related language within the telecommunications sector, particularly in analytics and cloud computing. This reflects the sector’s ongoing investment in digital infrastructure, customer behavior modeling, and network optimization—areas where AI tools have become essential to managing high data volumes and enabling services such as 5G rollout, predictive maintenance, and real-time service personalization.

Different keyword categories exhibit distinct temporal and sectoral patterns. Analytics is the most broadly adopted term, with usage growing steadily across most industries. Automation and AI terms appear less frequently but show sharp uptake in select years and sectors. Big data and cloud are often mentioned together, reflecting their complementary use in scalable data architectures. Digitization appears more often in sectors undergoing internal transformation, such as retail and communications.

Management Implications

It is noteworthy that while keyword counts proxy for awareness or strategic focus, they may not directly measure actual investment or implementation. Mentions in filings could reflect forward-looking plans, reactions to competitive pressure, or boilerplate language. However, prior research has shown that textual disclosures can be predictive of future firm behavior and market reactions (Li, 2008; Chen and Srinivasan, 2020), suggesting that these proxies offer meaningful insights into industry-level AI engagement.

This article presents a method for tracking AI adoption across industries using textual analysis of regulatory filings. By systematically counting AI-related terms in 10-K documents for nearly 8,000 US firms, we visualize trends in adoption over time and across industries. Our findings indicate that AI adoption is expanding rapidly across industries, led by a few dynamic service sectors that are at the forefront of this transformation. Analytics and cloud computing remain the most widely adopted category, while more technical terms like “machine learning” and “deep learning” are still relatively rare in non-tech sectors. The approach offers a framework for further empirical work on digital transformation and sectoral readiness.

Based on the findings, contemporary managers will benefit from the following strategic approaches:

- Prepare for greater AI engagement. During the course of the study, AI engagement has increased. This trend will likely continue. Managers will be well served by planning their AI agenda in advance and pursuing strategic workforce training.

- Plan for diverse utilization of technological tools. The findings suggest that companies have used a diversity of AI and other technological tools. Managers need to understand that technological progress does not necessarily follow just one path but rather multiple paths at different speeds. Set goals as well as resource allocation need to align with this reality.

- Design the right digital transformation framework. It is evident from the research that digital technologies are reshaping the playing field of industries. The breadth and scope of transformation varies from industry to industry. Managers need to carefully assess their organization alongside the industry they are in and plan for the optimal and most impactful digital transformation.

The adoption of AI across US industries is presently underway. As such, organizational transformations are unfolding as new technologies gain popularity, prominence and usage. Contemporary managers need to strengthen their strategic planning skills to manage emerging threats as well as exciting opportunities ahead.