By Peter Weill & Stephanie L. Woerner

Top-performing firms reorganise several times to effectively use digital to capture value. In a series of CEO interviews, we identified four successful levers for maximising value from digital. Then, in a global survey, we found that the companies in the top quartile of effectiveness on these four levers were also top financial performers, growing 12 percentage points above their industry average, and leaders in innovation, with 45 per cent of their annual revenue coming from new products introduced in the last three years – a huge premium. In this paper, we describe the four levers and the reorganisation required, illustrating with examples including Standard Bank Group, the largest bank in Africa. To become a top performer takes persistence, as companies must perform organisational surgery – reorganising on average seven times to create the industry-leading value. It is like solving an organisational Rubik’s cube, with a big payoff.

How many major organisational changes has your company been through in the last five years, and did those changes create value? At MIT CISR, we studied over 700 companies to understand how companies unlock new digital value.1 We found that a company must perform organisational surgery, often reorganising many times to create the value. The top-performing companies in our research underwent, on average, 7.2 major organisational changes in the preceding five years, but the results were worth the disruption, as the companies grew well above their industry average.

Historically, organising a company to maximise value from digital started with the technology leader looking out of the IT organisation to understand what the business needed.

We found that the companies in the top quartile of effectiveness at using these four levers were also top financial performers, growing at almost 12 percentage points above their industry average, and leaders in innovation, with 45 per cent of their annual revenue coming from new products introduced in the last three years. From the interviews, we learned that taking a top-executive perspective rather than a tech leader perspective can enable the kind of persistence, organisational buy-in, and change needed to unlock industry-leading digital value enterprise-wide.

In this paper, we describe the four levers and illustrate them with examples from companies including Standard Bank Group and ANZ, and discuss how to move from the technology-led governance to the enterprise-wide governance that is now needed to succeed.

The Four Levers to Create New Digital Value

Historically, organising a company to maximise value from digital started with the technology leader looking out of the IT organisation to understand what the business needed. But in today’s world of technology everywhere, it’s time to take, first, a CEO perspective and, then, an enterprise-wide one to design the organisation to maximise value from digital. To understand how top-performing companies organise for digital, we began by interviewing eight CEOs of large organisations and then followed up with their colleagues, to learn what organisational levers were used to create new digital value. Four levers to unlocking value emerged. Each of these levers needed to be supported by CEO involvement to drive the necessary changes in company and employee behaviour. Then we surveyed executives from 721 companies to understand best practices and the impacts of employing the levers on company performance.

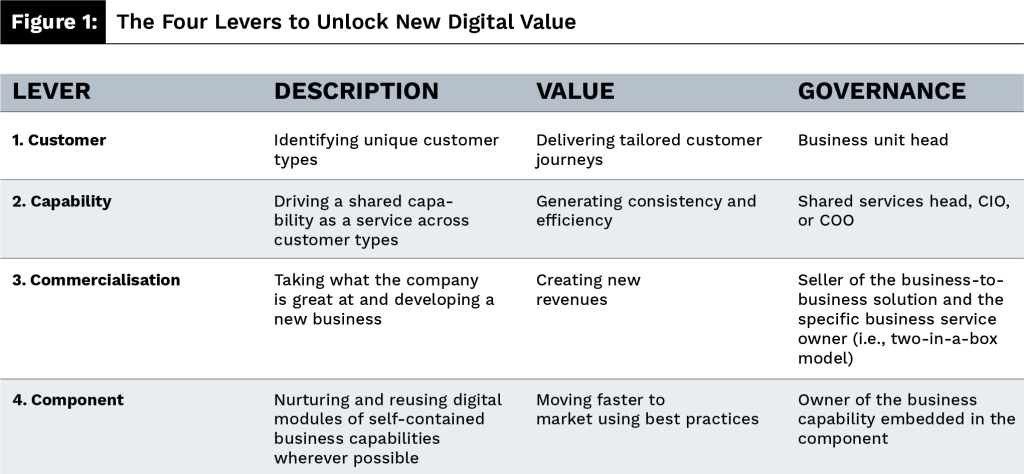

Companies focused on these four levers to unlock new digital value:

- Customer: Identifying and delighting the most important unique customer types.

- Capability: Providing and reusing a shared capability as a service across customer types.

- Commercialisation: Commercialising what the company is great at to generate new revenue.

- Component: Designing, embedding, and reusing digital modules of self-contained business capabilities.

Each lever produced a specific type of value to help drive top performance:

- Value from customer – focus: Customer loyalty and increased revenue per customer via tailored customer journeys and customer focus.

- Value from capability – scale: Consistency and efficiency across different customer types while capturing key data.

- Value from commercialisation – new revenues: New revenues from providing services to other companies based on what the company is great at.

- Value from component – speed via reuse: Faster time to market using best practices and decentralised governance with better compliance.

Let’s go into more detail on each of the levers.

Identifying Unique Customer Types

To unlock new digital value from customers, a company’s senior executive team must first identify their set of unique customer types to focus on, describing each type’s persona, customer journey, data model, channels for engagement, and more. In financial services, customer types typically include home buyers, small business enterprises, corporations, and high-wealth individuals and families. Developing an understanding of its most important customer types helps a company to really empathise and focus on meeting customer needs. The top-quartile performers on growth focused on an average of 8.9 unique customer types, typically describing for each type how they preferred to engage with the company, the typical products and solutions needed, the kinds of offers found attractive, and the associated data profile and systems that made the customer journey easy. In our interviews, CEOs reported that each customer type needed a senior executive who had both decision rights and accountability for success and, increasingly, customer journeys were supported by providing curated access to complementary and partner service providers.

Driving a Shared Capability as a Service

Leveraging business capabilities as a shared service helps a company to generate speed and efficiency. Here, senior executives must first identify what capabilities are common across customer types. Standardising, automating, branding, and reusing these capabilities allows the company to drive consistency, which both provides the customer with a common experience across products and increases efficiencies for the company. Shared capabilities can lead to better insights, because the data collected is more consistent and in one place. For example, a key shared capability in banking is a unified customer profile that details a customer’s current assets, products, and a forecast of their future needs, along with their identity, credit score, risk tolerance, and other factors.

The top-quartile growth companies provided an average of 6.3 separate business capabilities as a service across (almost) all their customer types. Because this lever can be hard to implement politically, as they were often centralised, top performers were selective about which services to share across customer types, thereby ensuring that the services were strategically important and there were a manageable number.

Commercialising What the Company Is Great At

The top-quartile growth companies selected internal capabilities they were great at – their crown jewels – and commercialised them as a service to produce a new revenue stream. This anything-as-a-service model, which we call XaaS, is becoming an important growth area for many companies as digital connections between companies become easier. Examples of XaaS that some banks have developed include anti-money-laundering (AML), payments, know your customer (KYC), and foreign exchange (FX). Often, such services are essentially selling compliance as a service, allowing the company to derive more value from its own efforts to address increasing compliance costs and create increasing scale.

Australian bank ANZ has recently focused on providing XaaS in areas including international payments and anti-money-laundering (AML). ANZ CEO Shayne Elliott described the bank’s AML efforts:

We saw one major player exit this business as a result of some AML issues, which meant their customers had sixty days to find another provider. Of those, there were seventeen major mandates and we won sixteen of them. That took our [AML] market share from the low 40s to 58 per cent.2

In our top-quartile companies on growth, an astounding 56 per cent of revenues were generated using the XaaS approach, unlocking a lot of previously untapped value.

Embedding, Nurturing, and Reusing Digital Modules

Embedded digital modules, sometimes called components, create new digital value for the company by driving consistency, compliance, and speed to market. Digital modules are “atomic” business capabilities, in that they are fully self-contained and right-sized. They are fine-tuned, automated, and reused in every possible application in the company, and nurtured by their owners to ensure they maintain best practice.

In financial services, typical examples of such modules are establishing the customer identity, onboarding a new customer, establishing or accessing a customer’s credit score, assessing risk, assessing compliance, and many other often-reused business capabilities. Often the motivation for these modules is to increase speed to market of different groups, while meeting compliance with regulations via consistency of approach and common reporting. Modules are built into the other three levers – customer types, shared capabilities, and XaaS – as well as other opportunities for reuse. The top-quartile companies on growth were 80 per cent effective at digital module reuse, improving their time to market and helping to generate an industry-leading percentage of revenues from new products introduced in the last three years.

Once a company has identified which business capability to modularise, it typically uses decentralised governance and APIs or some other kind of digital service to create the module and share it easily.

Top Performers on Growth and Innovation Used All Four Levers Effectively

Companies that were more effective at using the four levers individually grew faster than their peers. And the companies that were in the top quartile of effectiveness of all four levers combined grew even faster, at 11.7 percentage points above industry average.

Standard Bank Group, the largest financial services group in Africa,3 has used all four levers to unlock new digital value as part of the bank’s digital business transformation.

Unlocking New Value at Standard Bank Group

In its strategic transformation plan, Standard Bank Group describes serving the needs of clients in financial services and beyond by “banking the ecosystem” – i.e., providing financial services in all the ecosystems the bank is targeting. Behind this vision is Standard Bank’s inspiring purpose: “Africa is our home, we drive her growth.”4

The bank started by focusing on three client segments (Customer): consumer and high-net-worth clients, business and commercial clients, and wholesale clients. It identified client acquisition and engagement as the drivers for sustainable growth. The bank also initially targeted 10 ecosystems to operate in (Customer) – five that it would drive, such as agriculture and trade, and five that it would participate in, such as energy and education. It has since narrowed its focus to ecosystems where it is able to achieve the most competitiveness, including trade and home services. Standard Bank’s participation in an ecosystem typically involves offering B2B financial services the bank is great at (Commercialisation), such as FX and payments.

We found that in a digital / AI everywhere world, companies should rethink the traditional model of the technology organisation.

To enable shared capabilities as a service (Capability), the bank created a new group, called Client Solutions, that serviced the client segments with banking, insurance, and investment services. However, as the transformation progressed, the bank found that it was more efficient to provide these services within the client segments and reverted the segments to being more traditional business units.

Finally, a great deal of effort went into architecting modularity (Components). Standard Bank’s modularity relies on standardisation and simplification, as well as the technological capability to connect both internally and with partners, enabled by API readiness and integration and scalable and interoperable platforms. The bank calls developing modularity in this way “unpacking the honeycomb”, and tracks the number of digital solutions as a percentage of total solutions it has achieved. In 2021, 24 per cent of the bank’s banking solutions and 22 per cent of all solutions were digital solutions, and it was aiming for a target of 50 per cent across all solutions by 2025.

Standard Bank is making great progress toward its transformation goals, with the bank’s 2022 results demonstrating record revenue and earnings.5 The positive impacts continue in the first half of 2023, when the bank’s cost-income ratio (a common measure of efficiency) improved from varying between 55 and 58 per cent over the previous 10 years to 50.5 per cent.6

The Importance of Lever Governance in Unlocking Value

To unlock its value, each lever needs to be governed and nurtured differently (see figure 1). The Customer lever is typically owned and governed by business unit heads with responsibility for engaging each customer type. The governance of the Capability lever, because it spans different customer types, is typically owned centrally by a shared services group, COO, or CIO who operates those services for the rest of the company, perhaps on a chargeback basis. We have also seen leader-follower models, where one business unit takes the lead on a particular service and then provides it to the other business units. The ownership of the Commercialisation lever frequently belongs to a combination of people who sell business-to-business solutions and the specific business service owner (e.g., payments), often using a two-in-a-box model.7 Finally, components are typically owned and governed by the business owner of the business capability embedded in the component, such as risk management (owned by the head of risk), know your customer (the head of compliance), credit scoring (the CFO), or payments (the head of the payment service), often in partnership with a technology leader.

The Key to Realising Value from the Four Levers

We found that in a digital / AI everywhere world, companies should rethink the traditional model of the technology organisation. Instead of taking a technology-led perspective, we recommend taking the CEO, enterprise-wide perspective on designing the technology capability to unlock maximum value from digital. To be a top-quartile growth company in the digital era requires focusing on four levers to create digital value. But companies must iterate several times to get the levers to work together to unlock that value. And they have to implement an ownership and governance model that encourages nurturing and reuse of the four levers. They also need very good real-time metrics that measure the effectiveness of the levers, their impact on performance, and the capabilities needed to deliver them, shared widely via a dashboard. Finally, they need the support and vision of the CEO and top management team, along with the board, to help exploit the levers throughout the company. It is like solving an organisational Rubik’s cube with a big payoff.

This paper draws on Weill, Peter and Stephanie L. Woerner. “Unlocking New Digital Value.” MIT Sloan Center for Information Systems Research, Research Briefing, XXIII-7, July 2023.

About the Authors

Peter Weill, PhD, is an MIT Senior Research Scientist and Chairman of the Center for Information Systems Research (CISR) at the MIT Sloan School of Management, which studies and works with companies on how to transform for success in the digital era. MIT CISR has approximately 75 company members globally who use, debate, support and participate in the research. Peter’s work centres on the role, value, and governance of digitisation in enterprises and their ecosystems and has coauthored 10 books. Ziff Davis recognised Peter as #24 of “The Top 100 Most Influential People in IT” and the highest-ranked academic.

Peter Weill, PhD, is an MIT Senior Research Scientist and Chairman of the Center for Information Systems Research (CISR) at the MIT Sloan School of Management, which studies and works with companies on how to transform for success in the digital era. MIT CISR has approximately 75 company members globally who use, debate, support and participate in the research. Peter’s work centres on the role, value, and governance of digitisation in enterprises and their ecosystems and has coauthored 10 books. Ziff Davis recognised Peter as #24 of “The Top 100 Most Influential People in IT” and the highest-ranked academic.

Stephanie L. Woerner, PhD, is a Principal Research Scientist at the MIT Sloan School of Management and Director of MIT CISR. She is a renowned researcher and speaker, and coauthor of Future Ready: The Four Pathways to Capturing Digital Value and What’s Your Digital Business Model? Six Questions to Help You Build the Next-Generation Enterprise, both published by Harvard Business Review Press. Stephanie studies how companies use technology and data to create more effective business models as well as how they manage the associated organisational change and governance and strategy implications. Stephanie’s research has appeared in MIT Sloan Management Review, Harvard Business Review, CNBC, Forbes, Chief Executive, and CIO.

Stephanie L. Woerner, PhD, is a Principal Research Scientist at the MIT Sloan School of Management and Director of MIT CISR. She is a renowned researcher and speaker, and coauthor of Future Ready: The Four Pathways to Capturing Digital Value and What’s Your Digital Business Model? Six Questions to Help You Build the Next-Generation Enterprise, both published by Harvard Business Review Press. Stephanie studies how companies use technology and data to create more effective business models as well as how they manage the associated organisational change and governance and strategy implications. Stephanie’s research has appeared in MIT Sloan Management Review, Harvard Business Review, CNBC, Forbes, Chief Executive, and CIO.

References

-

This research is based on the MIT CISR 2022 Future Ready Survey (N=721), plus interviews with eight CEOs conducted in 2021–2 and case vignettes of five large companies in manufacturing, medical technology, financial services, and real estate.

-

Shayne Elliott, “Elliott: Accelerating Our Strategy”, ANZ bluenotes, 27 May 2021, https://bluenotes.anz.com/posts/2021/05/anz-ceo-shayne-elliott-banking-future.

-

Standard Bank Group was the largest financial services group in Africa, based on Tier 1 capital, in 2023; see T. Minney, “Africa’s Top 100 Banks in 2023”, African Business, 4 October 2023, https://african.business/2023/10/finance-services/africas-top-100-banks-in-2023

-

“Purpose and Values”, Standard Bank Group, https://www.standardbank.com/sbg/standard-bank-group/about-us/who-we-are/purpose-and-values.

-

See “Overview of Financial Results”, Investor Relations, Standard Bank Group, https://reporting.standardbank.com/overview-financial-results-2022/ .

-

https://reporting.standardbank.com/about-us/key-performance-indicators/

-

Two-in-a-box is a management model in which two (or more) people are given equal leadership authority and responsibility for a task or set of tasks, often in complementary roles. Read about a two-in-a-box model in use at DBS in S.K. Sia, P. Weill, and M. Xu, “DBS: From the ‘World’s Best Bank’ to Building the Future-Ready Enterprise”, MIT CISR Working Paper No. 436, 19 March 2019, https://cisr.mit.edu/publication/MIT_CISRwp436_DBS-FutureReadyEnterprise_SiaWeillXu.