The recent economic crisis has severely reduced the short-term willingness of firms to invest in innovation. But this reduction has not occurred uniformly. A few firms are swimming against the stream by increasing investment during the crisis. This has led to a greater concentration of innovative activities among firms already highly innovative before the crisis. Yet, there remains hope for dynamic entrepreneurs, as we see a small group of fast growing, new firms that also increase innovation investment during the crisis.

Gales of creative destruction

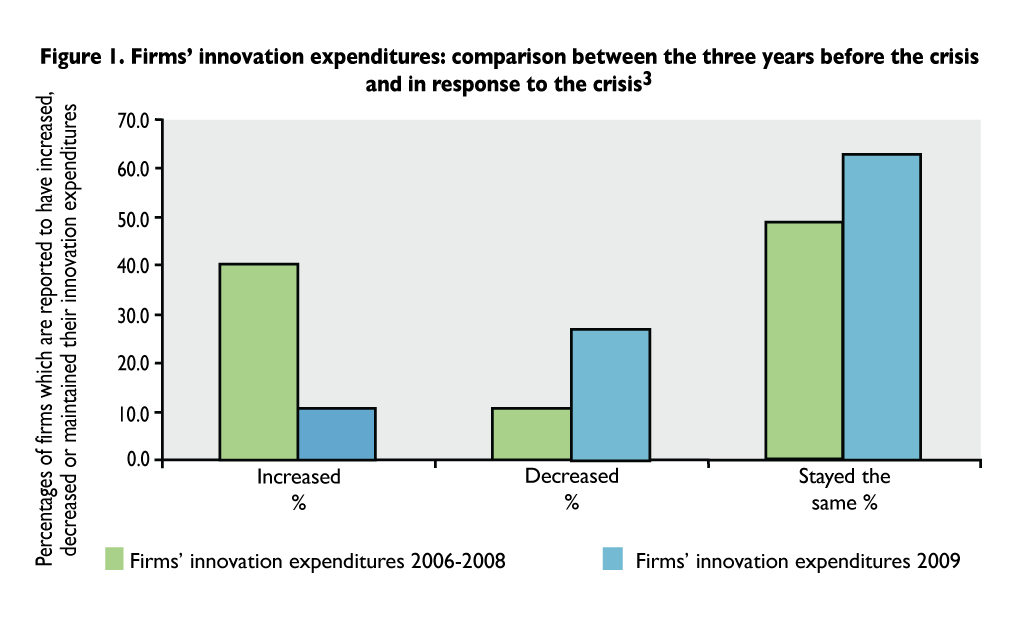

The economic crisis has meant that firms operate in environments characterized by greater uncertainties about the demand for (new) goods or services and their willingness to invest in innovation decreased1. The economic downturn is having a profound impact on firms’ innovation behaviour across Europe. The percentage of firms that increase innovation-related expenditures has fallen dramatically from 40.2% to 10.6% as a direct result of the crisis (see Figure 1). In turn the percentage of firms that decrease their spending on innovation surges from 10.8% to 26.7%. But also remarkable is the presence of a large number of firms that keep their innovation spending unchanged (which rose to 60% from around 50% before the crisis)2.

The impact of the economic downturn on firms’ innovation spending is also visible if we look at data across European economies. In Figure 2 below we plot the difference between the share of firms increasing and those decreasing their innovation spending relative to two periods: 2006-2008 and 2009. Results for the two periods are strikingly different. If we look along the x-axis (innovation expenditures in 2006-2008), all countries show a positive balance, that is, the percentage of firms increasing their innovation spending is higher then firms decreasing for all the considered countries. But if we turn to 2009 and read along the y-axis, we see that only four countries remain in a position where the share of firms increasing innovation activity outweighs that of firms decreasing. These four countries are located above the dot line, which corresponds to a balance equal to zero in 2009.

Swimming against the stream

While the average firm reduced overall expenditures on innovation as a result of the economic downturn, a few firms are swimming against the stream by increasing their investment in activities such as in-house R&D, purchases of R&D services, technology licensing, design and marketing of, and training aimed at the development of new goods and services.

Who are these firms that decided to respond to the crisis by innovating more rather than less? There are two possible scenarios:

(a) These firms are the most dynamic; those that cannot survive without changing their products and services. The competitive advantage of these firms resides in the generation and upgrading of new knowledge, and they innovate continuously, irrespectively of the business cycle.

(b) Or, alternatively, these firms are new innovators that were not necessarily involved in innovation before the crisis. These firms might be smaller in size or entirely new firms that take advantage of the crisis to contest the market shares of incumbent firms or to launch fresh markets.

Our work showed evidence pointing towards a combination of both scenario (a) and (b) that explains innovation during the recent crisis. We addressed this question empirically with the help of two large-scale business surveys that contain replies from manufacturing and private services enterprises. One survey is the Innobarometer survey conducted by the European Commission. The second survey is the UK version of the Community Innovation Survey collected by the Office for National Statistics on behalf of the Department for Business, Innovation and Skills. The latter is perhaps the most widely analysed and known among the official innovation data.

For one survey firms are located across the whole of Europe. The second dataset is based on responses from UK firms. In both surveys, the firms replied to a breadth of questions into their innovation behaviours before the crisis and during the crisis. This included investments in the following innovation related activities: in-house R&D, bought-in R&D, bought-in other knowledge for example licensing-in of patents. This current article heavily draws on, and borrows from, two of our papers and provides a taste for some of the key findings4.

The two scenarios: past innovators and new players

An external shock in the form of an economic crisis, and the contraction in demand that it brings, is affecting firms’ innovation-related investments. This happened with the 2008 financial crisis, which brought with it a drop in innovation investment in Europe and elsewhere. Since then firms found that they are operating under greater uncertainties about the development of their markets and the relevant technologies compared to the years preceding the recession. Theory links periods of economic downturns to shifting patterns of industries or sectors that exhibit the largest innovation and growth rates, or the largest opportunities for innovation and growth. A decline in the technological and profit opportunities in established industries affects incumbent firms5. One argument is that the crisis might see new players contributing towards innovation and doing so in new areas: sectors, markets or technologies.

However, there is also evidence that suggests economic turmoil does not undermine or erode the role of the past innovator. Cumulativeness in innovation dominates times of relative calm in external environments, and it matters during economic turmoil. Firms’ internal resources, financial, capital equipment and technological know-how all contribute towards continuous innovation activity – persistence in innovation investment, independent of changes in aggregate demand. This is supported by the fact that the number of large and incumbent firms remained fairly stable for several decades, irrespectively of economic cycles and recessions6. Firms that innovated successfully and repeatedly in the past are those most likely to continue to innovate in the present and in the future.

The persistence in innovation among ‘great’ innovators

The existing literature on persistence has identified the characteristics of innovating firms, but has not given specific attention to economic cycles. The findings of this literature relevant here are that: persistence in innovation tends to be low (while persistence in non-innovation is high); and persistence is strongest among ‘great innovators’ or firms that reach a specific threshold of innovation activities, identified, for example, by a large number of patents registered every year. We tried to identify a category of highly innovating firms – ‘great innovators’ with a minimum threshold of innovation – and looked at changes in their innovation investment before and during the crisis.

We find strong support that ‘great’ innovators are more likely to swim against the stream by increasing innovation activities during the crisis. Those firms that were most successful in innovation in the previous period (measured in 2004) are those that continue to invest in 2008 and, indeed, increase on their previous levels of investment. This supports our scenario (a) above.

Fast growing, new firms increase innovation activities during the crisis

We combined looking at great innovators with an analysis of fast growing, new firms. Newly established firms are on average small, with fewer than ten employees, and they operate at suboptimal levels of output, giving them a competitive disadvantage in most markets. If such new firms are successful they are very likely to rapidly expand and grow. We identified a group of comparatively young firms – established after 2000 – and coupled this information with their sales growth before the crisis. While the group of young or newly established firms is not as such responsible for increased innovation investment (before or) during the crisis, we find evidence that fast growing, new entrants increased innovation activities during the crisis, pointing towards scenario (b) above. Moreover, firm size less well predicts innovation investment during the crisis compared with before the crisis.

Of course, it is possible, and likely, that the majority of firms, specifically those with greater internal resources, continue or indeed increase innovation investment with respect to specific projects, but pause or abandon other projects. Economic crises may spur change in investment strategies as a managerial response to the changes in the macro-environment. During a crisis many firms might focus more strongly on survival, and less on seeking out new opportunities.

A probable strategy is a combination of retrenchment and investment that involves seeking out new products or markets in certain areas, while engaging in cost-cutting measures and activities aimed at increasing efficiency in other areas. Additionally, there is likely to be a qualitative shift in the aims of innovation activities towards new processes or methods that focus lead-to-cost savings in the production of goods or the delivery of services.

This trade-off between exploitation (changes to bring about cost-saving measures and increase in efficiency) and exploration (new product or market development) was put forward by March who suggests that in order to survive firms need to maintain an appropriate balance between the two7. Our data indicates that explorative strategies – positive both before and during the crisis – have a larger impact during the crisis. The reverse is the case for exploitation strategies that appear to matter more before the crisis than during the crisis.

Size and sales performance strategies predict increased innovation investment before the crisis. However, when we turn to what happened during the crisis, we see interesting differences. Size and performance strategies play a less important role. By contrast, the presence of in-house R&D activity becomes a major predictor of increase in innovation expenditure during the crisis.

This evidence suggests that during the current crisis the sources of persistence in innovation are fundamentally two. In the first place, the existence of an R&D department suggests the firm has made a medium or long-term commitment to innovation. Secondly, we show the important contribution of a strategy, and in particular of a strategy aimed at exploring new markets and new product developments.

Conclusions

The aim of our research is to investigate how the current economic downturn affected different innovating firms. During major recessions, the economic landscape is characterized by huge uncertainties about the direction of technological change, demand conditions, and new market opportunities. The first significant result at the aggregate level is that the crisis has substantially reduced innovation expenditure of the firm. No doubt that the crisis has brought, at least in its initial stage, “destruction” in the amount of resources devoted to innovation. The second major aggregate result is that innovation expenditure started to be more concentrated: fewer firms were responsible for an increased share of innovation expenditure.

Our evidence strongly supports the case for creative accumulation; those firms identified as the great innovators are responsible for a larger share of innovation expenditure in 2008 compared to 2006. It should also be noted that the great innovators do not stand as increasing innovation before the crisis, in 2006. Put differently, the cumulative, or persistent, nature of innovation activity tends to be more prominent in times of crisis compared to during ordinary times.

But, does this mean that the crisis is exacerbating the concentration of innovation in a few firms, thus leaving little hope for dynamic Schumpeterian entrepreneurs? In fact, alongside the great innovators there is another category of firms that are gaining momentum during the crisis by increasing innovation expenditure. They are the fast growing new firms. As with the great innovators, this group of firms does not show an above average behaviour in 2006 but it starts to increase expenditure during the crisis.

On the one hand, policies should support the good innovators, and reward the winners under the assumption that those who won in the past are those better equipped to also win in the future. On the other hand, policies should also encourage the creation of new innovative firms. It is certainly not easy for policy makers to recognize which of the new firms are more likely to be successful, and the fact that they are relatively young makes this task even harder. Our data suggests that size alone would not be enough to indicate if a firm will be successful. Other structural characteristics, such as the presence of an R&D department and its past economic performance, seem to play a more important role.

The article draws materials from Innovation and Economic Crisis, by Daniele Archibugi and Andrea Filippetti, 2011, Routledge.

About the Authors

Daniele Archibugi is a Research Director at the Italian National Research Council in Rome and Professor of Innovation, Governance and Public Policy at the University of London, Birkbeck. He has worked and taught at the Universities of Sussex, Naples, Cambridge and Rome, was a Leverhulme Visiting Professor at the London School of Economics and Political Science, and a Lauro de Bosis Visiting Professor at Harvard University.

Andrea Filippetti is a Researcher at the National Research Council of Italy. He gained his PhD in Economic Science from the University “La Sapienza” of Rome. He was a DIME Visiting Fellow at Birkbeck, University of London. In the autumn of 2011 he was a Fulbright-Schuman Post Doc at Harvard University. He is interested in innovation, EU innovation policy, regional development and institutions, the globalization of intellectual property rights, technological change and productivity.

Marion Frenz is Senior Lecturer at Birkbeck, University of London. Her research focuses on the measurement and determinants of firms’ innovation performance. Supported by an ESRC knowledge transfer grant, she was seconded to the UK Department for Innovation, Universities and Skills – Science and Innovation Analysis Unit (SIA) – during 2007.

References

1. Figures are based on our own analysis of Innobarometer data.

2. Because this statistic omits micro firms, those with ten or fewer employees, we might well underestimate the true extent of the decline in innovation investments in these statistics or statistics reported elsewhere. In a sample of around 2,000 UK firms average innovation related investment fell by 8 % in 2008 compared with 2006 .This figure is based on our own calculations of UK Innovation Survey data.

3. Archibugi, D. and Filippetti, A., 2011. Innovation and Economic Crisis. Lessons and Prospects from the Economic Downturn, Routledge

4. Archibugi, D., Filippetti, A., and Frenz, M., 2011. Who is swimming against the stream: is accumulation more creative than destruction? in Archibugi, D. and Filippetti, A. Innovation and Economic Crisis. Lessons and Prospects from the Economic Downturn, Routledge, 113-135.

Archibugi, D., Filippetti, A. and Frenz, M., 2012. Economic crisis and innovation: is destruction prevailing over accumulation? Research Policy, in press.

5. Perez, C., 2009. The double bubble at the turn of the century: technological roots and structural Implications. Cambridge Journal of Economics 33 (4), 779-805.

6. Chandler, A.D., 1977. The Visible Hand: The Managerial Revolution in American Business. Belknap Press, Cambridge MA.

7. March, J., 1991. Exploration and exploitation in organizational learning. Organization Science 2 (1), 71-87.