By Gilles Paché

The war in Ukraine is a major geopolitical crisis whose first economic repercussions, particularly in terms of inflation, were quickly felt in Europe. Looking further ahead, the resulting disruption in supply systems could give rise to new models of industrial organization. Will the Ukrainian crisis lead to a ‘regionalization’ of global value chains?

The Covid-19 health crisis underlined the impact of an external shock on the supply systems of retailing and manufacturing companies, as we reported in a 2022 article1. For example, recurring stockouts and a sharp increase in delivery times have led to deteriorating customer service levels. Not surprisingly, the Ukrainian crisis is in turn highlighting dysfunctional supply of raw materials, components, and commodities, as Ebru Orhan’ analysis points out2. Europe is now obliged to find alternative sources to those historically coming from Russia (including the famous gas), but also from Ukraine. The presence of global value chains amplifies the problems, with shortages spreading much more quickly over entire continents like a tsunami.

In their article published in March 2022, David Simchi-Levi and Pierre Haren cite the case of neon gas, used massively in the manufacture of semiconductor chips3. Ukraine supplies about 50% of the world’s neon gas, which highlights the magnitude of future shortages in the event of a multi-year conflict. The effects of other shortages have also been felt since the spring of 2022. For example, Volkswagen and BMW have been forced to reduce their production levels due to a shortage of electrical harnesses, as Ukrainian suppliers have stopped making and therefore delivering them. This has resulted in queues of several months to get access to a new vehicle, a situation that was almost unthinkable even ten years ago. An ‘old world’ seems to be collapsing before our eyes, paving the way for what could be a new, post-crisis world, which is shrinking back to local geographical areas.

A predictable inflationary drift

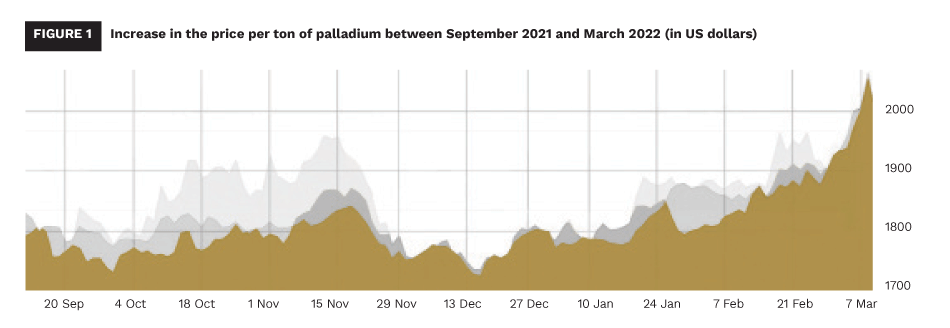

The impact of the war in Ukraine on supply systems is considerable, with major consequences on the procurement costs of raw materials, components, and commodities. In highly competitive industries, such as automotive and smartphone industry, the competitive advantage built up over decades is under threat. For example, while it is essential for the manufacturing of catalytic converters, the price of palladium rose as early as January 2022, when diplomatic tensions increased, and it literally exploded a few days after the start of the war in Ukraine. Figure 1 shows its evolution, compared to that of gold and platinum, to highlight the extraordinary convergence of trends.

There are dozens of other examples of soaring prices and, by mechanical effect, a return to a period of high inflation that is reaching dramatic peaks in a country like the United Kingdom. Observers have discovered that European aluminium production is highly dependent on alumina imports from Russia. As early as March 2022, the price of a ton of aluminium traded above 3,400 US dollars for the first time, up from 2,400 US dollars at the end of 2021, just two months earlier. Since manufacturers have little inventory on hand, a direct result of their just-in-time policy, the impact is almost immediate for many convenience goods, such as soft drink cans. The surge in the price of materials and components is further compounded by a drying up of supply while demand remains high in the wake of the Covid-19 crisis.

The main reason for this critical situation is Russia’s historical specialisation in the energy and metal sectors, which are largely located upstream of the value chains. Disruptions in supplies from Russia therefore spread down the value chains to European countries whose companies have specialised in assembly activities. Given that Russian inputs are involved in a very large number of value chains, the implications could be long-lasting in Europe. From this point of view, the recent finding of Deborah Winkler and her colleagues is not optimistic: value chains that rely heavily on inputs from Russia include a very wide range of goods from transport equipment to machine tools, micro-electronics, and food4.

Supply systems under strain

Faced with the external shock of Russia’s invasion of Ukraine and its effects on global value chains, the first reaction of European companies was to find alternative solutions that did not fundamentally challenge their supply systems. Building on their recent experience with the Covid-19 pandemic, most companies have continued to implement adaptive approaches, including developing new risk management practices more quickly and increasing their stocks of critical components and commodities. European states have also chosen the same path, filling up their strategic gas stocks to the maximum before the winter of 2022. But these emergency measures conceal profound changes to come, the effects of which are difficult to measure for the moment.

Tobias Korn and Henry Stemmler offer a thought-provoking analysis of what the ‘world after’ might look like5. Their reasoning focuses on the long-term consequences of the war in Ukraine on supply systems. They do this by looking at the impact that past civil wars have had on the organisation and functioning of global value chains, using the classification of civil wars proposed by the Uppsala Conflict Data Program. What do the two researchers find? Their analysis shows that importers react to supply disruptions from a country at war by increasing imports from other countries at peace. Substitution of suppliers is most obvious and fastest for agricultural products and minerals. For manufactured goods, changes in the supply system take time and are likely to be implemented during conflicts that last several years, in an irreversible way.

If we follow this argument, which is particularly well constructed statistically, it is likely that the reconfiguration of global value chains following the war in Ukraine, as is the case at the end of a civil war, will produce a profound reorganisation of supply systems, favouring new suppliers who might not have been selected without the presence of the war.

In short, the situation since the end of February 2022 is undoubtedly conducive to a radical transformation of value chains. We should not draw the conclusion that regionalised value chains will triumph in the future, as Christopher Tang’s article suggests6. The situation will probably be more nuanced, with the presence of global value chains based on totally different ranges of action from those that were dominant even ten years ago, and which are superimposed on each other.

Towards a multipolar world

One thing is clear: beyond the purely technological questions, it will undoubtedly be necessary to consider a more ‘geopolitical’ approach to the construction and operation of value chains. For several decades, researchers and practitioners have been emphasising the importance of new technologies as facilitators of globalised and unhindered exchanges. This is particularly true of blockchain, which has given rise to the publication of several hundred thousand academic papers. Numerous works are devoted to it, particularly to underline the capacity of the blockchain, a real miracle of modern times, to create the necessary trust to make the members of the supply chain collaborate, while guaranteeing the security, tracking/tracing and confidentiality of data.

Even if blockchain facilitates exchanges between companies located in the four corners of the planet, the war in Ukraine reminds us of the importance of geopolitical issues that significantly disrupt the functioning of value chains. Although technologies have enabled us to make a great leap forward in terms of performance, we had collectively forgotten that the desire to control resources, including by force, makes these technologies very fragile. It is thus possible that the war in Ukraine, the outcome of which no one can predict in the autumn of 2022, will lead to a significant contraction of trade relations only between countries sharing the same ‘humanist values.’ But who can say with certainty that a country sharing common values with us today will not become hostile tomorrow, following a radical change of political regime? In other words, we have entered a time of great instability, a world that will be ‘more contested’ by 2040, as the subtitle of the latest CIA report puts it.

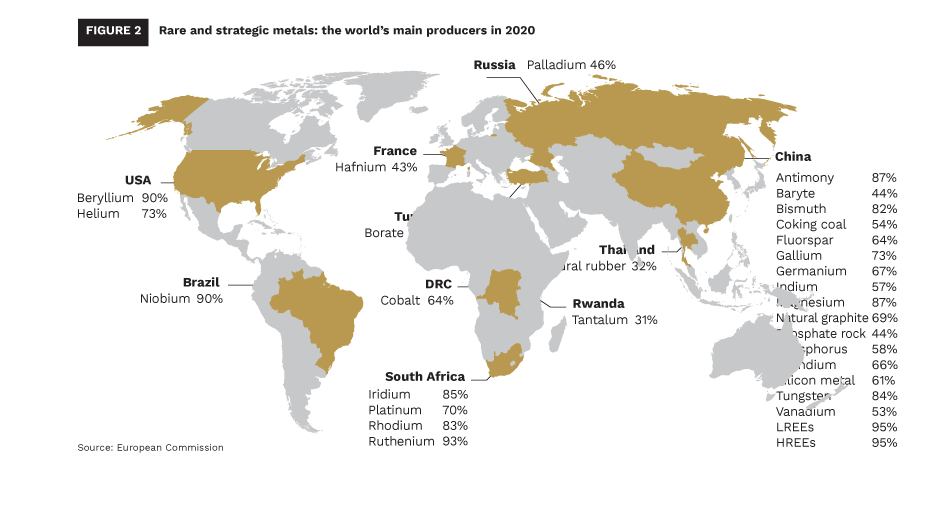

It is clear that the conflict between Ukraine and Russia is profoundly disrupting supply systems. But the situation could be much more dramatic if a major geopolitical crisis broke out between China, Taiwan and the United States. In addition to the fact that China has become the world’s workshop for convenience goods, Figure 2 shows that it also produces an impressive number of rare and strategic metals. The European Commission drew attention to this fact long before the Ukrainian crisis, but it takes on a special flavour in 2022. However, it cannot really be said that China shares common values with Europe, particularly in terms of human rights, and under these conditions, who could say that China will participate in a regionalised value chain that includes Europe?

It is clear that the conflict between Ukraine and Russia is profoundly disrupting supply systems. But the situation could be much more dramatic if a major geopolitical crisis broke out between China, Taiwan and the United States. In addition to the fact that China has become the world’s workshop for convenience goods, Figure 2 shows that it also produces an impressive number of rare and strategic metals. The European Commission drew attention to this fact long before the Ukrainian crisis, but it takes on a special flavour in 2022. However, it cannot really be said that China shares common values with Europe, particularly in terms of human rights, and under these conditions, who could say that China will participate in a regionalised value chain that includes Europe?

Great uncertainties ahead

Having just emerged from the Covid-19 pandemic, Western countries were faced with a new external shock of formidable intensity: the war between Ukraine and Russia. As with the pandemic, this shock affected the functioning of many global value chains, whether in the food, chemical, automotive or electronics industries. No one can say when the situation will allow for a return to calm, if ever. A recent Dun & Bradstreet report points out that Russia and Ukraine are major exporters of some of the world’s most important commodities: 374,000 companies worldwide use Russian suppliers, and 240,000 companies use Ukrainian suppliers7. It is easy to imagine the catastrophic consequences of war on thousands of global value chains.

Already, response strategies are being suggested to top managers to mitigate the impact of the conflict on global value chains. One of the most common recommendations is to develop alternative sources of supply, to secure upstream flows in order to continue to supply downstream BtoB and BtoC markets (household consumption which may recover rapidly after the crisis). This is the case of Boeing and Airbus for titanium, as underlined by Sarah Schiffling and Nikolaos Valantasis Kanellos8. In the long term, the creation of a portfolio of local suppliers is increasingly systematically encouraged, which is perfectly in line with the ‘regionalisation’ of global value chains. It must be recognised that this development would in fact be a revolution in the face of professional buyers who had become, in the 1990s, unconditional followers of global sourcing, in the image of Carlos Ghosn’s practices.

It is often said that the word ‘crisis’ refers to both a sudden event, a rupture, but also to a long evolution that highlights the structural weaknesses of an economic, political or social system. A crisis is ultimately characterised by a break in the stability of a system, in search of a new stability. History teaches us that the crises of industrial societies are linked to an imbalance between production and solvent demand, before becoming increasingly financial phenomena, when bank failures or stock market crashes precede the activity drop, as was the case during the 1929 great depression or the 2007-2008 recession. There is little doubt that the war in Ukraine is a major crisis that will force us to think about a new organisation of supply systems. If there is any ‘virtue’ to be found in this war, it is that it will force us to completely revise a business model whose limits have been in full view since 2020. It is very sad to note that the price to be paid is tens of thousands of deaths on Europe’s doorstep.

It is often said that the word ‘crisis’ refers to both a sudden event, a rupture, but also to a long evolution that highlights the structural weaknesses of an economic, political or social system. A crisis is ultimately characterised by a break in the stability of a system, in search of a new stability. History teaches us that the crises of industrial societies are linked to an imbalance between production and solvent demand, before becoming increasingly financial phenomena, when bank failures or stock market crashes precede the activity drop, as was the case during the 1929 great depression or the 2007-2008 recession. There is little doubt that the war in Ukraine is a major crisis that will force us to think about a new organisation of supply systems. If there is any ‘virtue’ to be found in this war, it is that it will force us to completely revise a business model whose limits have been in full view since 2020. It is very sad to note that the price to be paid is tens of thousands of deaths on Europe’s doorstep.

About the Author

Gilles Paché is Professor of Marketing and Supply Chain Management at Aix-Marseille University, and Director of Research at the CERGAM Lab, in Aix-en-Provence, France. He has more than 600 publications in the forms of journal papers, books, edited books, edited proceedings, edited special issues, book chapters, conference papers and reports, including the recent two books ‘La société malade de la Covid-19: regards logistiques croisés’ (2021), and ‘Variations sur la consommation et la distribution: individus, expériences, systèmes’ (2022).

Gilles Paché is Professor of Marketing and Supply Chain Management at Aix-Marseille University, and Director of Research at the CERGAM Lab, in Aix-en-Provence, France. He has more than 600 publications in the forms of journal papers, books, edited books, edited proceedings, edited special issues, book chapters, conference papers and reports, including the recent two books ‘La société malade de la Covid-19: regards logistiques croisés’ (2021), and ‘Variations sur la consommation et la distribution: individus, expériences, systèmes’ (2022).

References

- Paché, G. (2022). Living with shortages in the post-Covid world. Crisis Response Journal, Vol. 17, No. 1, pp. 64-66.

- Orhan, E. (2022). The effects of the Russia-Ukraine war on global trade. Journal of International Trade, Logistics & Law, Vol. 8, No. 1, pp. 141-146.

- Simchi-Levi, D., Haren, P. (2022). How the war in Ukraine is further disrupting global supply chains. Harvard Business Review [online], March 17. Available on: https://hbr.org/2022/03/how-the-war-in-ukraine-is-further-disrupting-global-supply-chains

- Winkler, D., Wuester, L., Knight, D. (2022). The effects of Russia’s global value chain participation. In Ruta, M. (Ed.), The impact of the war in Ukraine on global trade and investment. The World Bank, Washington DC, pp. 57-79.

- Korn, T., Stemmler, H. (2022). Russia’s war against Ukraine might persistently shift global supply chains. VoxEU CEPR [online], March 31. Available on: https://voxeu.org/article/russias-war-against-ukraine-might-persistently-shift-global-supply-chains

- Tang, C. (2022). It’s about time to build regional supply chains. Industry Week [online], March 30. Available on: https://www.industryweek.com/supply-chain/article/21237601/its-about-time-to-build-regional-supply-chains

- Dun & Bradstreet (2022). Russia-Ukraine crisis: implications for the global economy and businesses. Special Report, Jacksonville (FL).

- Schiffling, S., Valantasis Kanellos, N (2022). Five essential commodities that will be hit by war in Ukraine. The Conversation [online], February 24. Available on: https://theconversation.com/five-essential-commodities-that-will-be-hit-by-war-in-ukraine-177845