Research indicates that sustainability footprints can transform stakeholder perceptions of waste from being a cost center to a profit center, reduce carbon emissions by diverting waste from landfills, and stimulate innovation through the search for potential energy savings. In this excerpt, Lowellyne James discusses strategic options for SMEs to embed sustainability and highlights the role of quality management in sustainable development.

Reflecting on the major stories of the past few years floods in Australia and Brazil, Typhoon Haiyan, BP Deepwater Horizon incident, poor working conditions of garment factory workers in Bangladesh, food riots that led to the overthrow of a dictatorship in Tunisia – common themes emerge such as the environment, climate change, ethics, and human rights, which all fall under the vast umbrella of sustainability. Increasingly, governments are implementing policies and enacting legislation designed to reduce unabated carbon emissions through market mechanisms such as cap and trade schemes.1

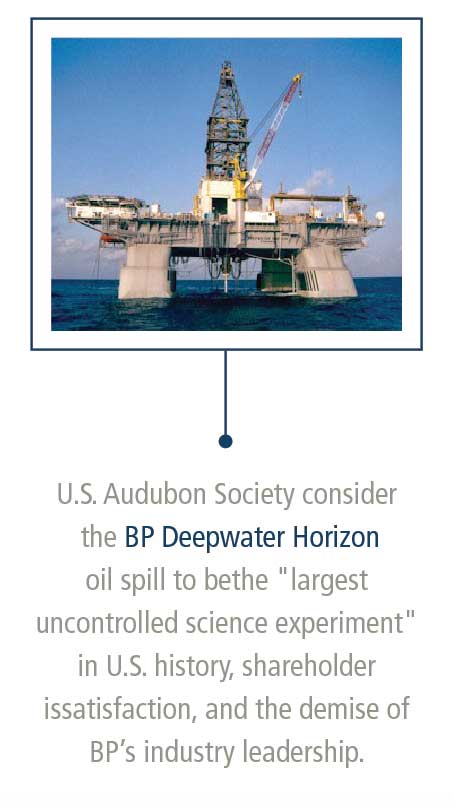

The BP Deepwater Horizon incident crystallizes the centrality of sustainability to business strategic success. Costs to BP arising from the absence of a quality culture that incorporates “minimal loss” to the society has been a $91 billion reduction of market value between April and June 2010, over 350 lawsuits from the general public, damage to its brand image, loss of support from environmental groups with the U.S. Audubon Society who consider the oil spill to be the “largest uncontrolled science experiment” in U.S. history, shareholder dissatisfaction, and the demise of BP’s industry leadership.2

The BP Deepwater Horizon incident crystallizes the centrality of sustainability to business strategic success. Costs to BP arising from the absence of a quality culture that incorporates “minimal loss” to the society has been a $91 billion reduction of market value between April and June 2010, over 350 lawsuits from the general public, damage to its brand image, loss of support from environmental groups with the U.S. Audubon Society who consider the oil spill to be the “largest uncontrolled science experiment” in U.S. history, shareholder dissatisfaction, and the demise of BP’s industry leadership.2

This absence of a quality culture gave rise to the following quality failures leading to the explosion aboard Deepwater Horizon:3

1. Incorrect parts: Centralizers, key equipment used in drilling operations, were received from supplier not to specification.

2. Breach of existing well design: The centralizers used in operations totaled to 6 instead of 21, a casualty of the misdirected focus on reducing the cost and not reducing the cost of quality.

3. No product verification: Incoming inspection tests were not conducted on the cement foam upon receipt from the supplier Halliburton.

4. Poor supplier management: The cement supplied by Halliburton failed in-house tests. The need to develop mutually beneficial supplier relationships is a corner stone of total quality management and quality management standards such as ISO 9001. BP’s relationship with its supply chain Transocean and Halliburton, as events have revealed, can be described as combative at best.

5. Poor process management: “Negative Pressure Test” was not dictated on the oil platform’s work plan. There was no procedure for conducting the “Negative Pressure Test.”

6. No management of change procedure: “Negative Pressure Test” was added to the work plan at the “eleventh hour”. This confusion led to the acceptance of one positive test result despite three failed negative pressure tests, a decision that sealed the fate of the crew of Deepwater Horizon.

These six quality failures resulted in the catastrophic loss of life and environmental disaster – the safety consequence –

a cost that is unquantifiable.

Safety is not the issue but a consequence of the absence of an understanding of quality and its impact on the triple bottom-line, that is, economic, social, and environmental. It is time for business and regulators to adopt an industry-wide approach that embraces continuous improvement that goes “beyond quality”.

Humanity’s insatiable appetite for knowledge and space exploration has also impacted negatively on the environment of earth’s orbital atmosphere. Most of us with our feet firmly planted on the ground may find it incredible that to date it is estimated that there are more than 21,000 man-made objects measuring more than 4 inches in earth’s orbit with millions of other objects measuring a centimeter or less. These man-made objects, benignly described as space debris, can range from spent booster stages, nuts, batteries, and nuclear waste to derelict satellites, all moving faster than 20 times the speed of sound, reaching speeds of up to 18,000 miles per hour just to remain in orbit. The management or lack of management of waste extends to the more distasteful issue of human waste matter, which in some instances is launched into the vastness of space.4

Environmental concerns placed aside the existence of space debris is a hazard that increases the risks inherent with space travel. Large companies such as Virgin Galactic, who are in the forefront in the race to commercialize space flight and colonize space, the existence of these hazards are being either ignored or muted in favor of economic or financial expedience.5 The risks of these hazards, however, are so acute that the US Space Surveillance Network, an arm of the US Department of Defense, daily tracks all space debris larger than 10 cm.

The National Aeronautical Space Agency (NASA) has taken the lead in embracing a more sustainable approach to space flight in earth’s orbit by developing mitigation standards aimed at reducing orbital debris. Similar plans have been developed by other countries such as Japan and institutions such as the European Space Agency.6 Although commendable, these efforts fall short of a cleanup of the earth’s orbital space, whose costs may prove prohibitive with the hope of incentives such as government subsidies to spur entrepreneurial activity in this sector, which may seem but a pipe dream in an age of government cutbacks and financial austerity. Despite the enormous challenge of removing space debris, two Japanese firms are engaged in a joint venture to develop space debris removal systems.7

Modern human activity on our planet, both terrestrial and atmospheric, is inherently carbon intensive.8 Armed with an understanding that the sustainability issues facing our planet are not only earth bound and that waste has gone orbital, I attended the Edinburgh Napier Business School for a meeting with the sustainability program course leader. During our conversation, I noticed four origami swans on his desk. Upon enquiring further, my colleague intimated that the items were found at the end of one of his lectures on the seat vacated by an anonymous student, jokingly suggesting it is symbolic of the quality of the lecture during which one of the students found origami more interesting!

Swans in mythology have helped Greek gods move across the sky and are considered by many ancient and indigenous people to symbolize transformation, balance, and elegance depending on their color. For example, black swans symbolize mystery or uncertainty.

My own research into the phenomenon of sustainability footprints (i.e., the use of carbon footprint, water footprint, ecological footprint, and the emerging concept of social footprint to evaluate present nonfinancial consequences and future risk implications of strategic decisions) indicates that sustainability footprint methodology is at the nexus of three management concepts (See Fig. 1.1), which are as follows:

Risk – sustainability footprint risk must incorporate environmental, social impact and its effect on cost structure and revenue streams.9, 10

Natural Resource-Based View – sustainability footprint measurement contributes to strategy through pollution prevention, product stewardship, and sustainable development.11-15

Shared Value – as indicators, sustainability footprint assists firms in the mitigation of environmental impacts arising from value chain activities.16, 17

These theories reveal four key areas within which sustainability footprints can contribute to the success of the firm in terms of cost impact, innovation impact, environmental impact, and stakeholder impact – the four swans of sustainability. The research study also categorized perceptions of the impact of sustainability footprints among small and medium-sized enterprise (SME) managers and personnel along a qualitative scale consisting of sustainability positive, sustainability passive, and sustainability negative.

These theories reveal four key areas within which sustainability footprints can contribute to the success of the firm in terms of cost impact, innovation impact, environmental impact, and stakeholder impact – the four swans of sustainability. The research study also categorized perceptions of the impact of sustainability footprints among small and medium-sized enterprise (SME) managers and personnel along a qualitative scale consisting of sustainability positive, sustainability passive, and sustainability negative.

Results of this research indicate that sustainability footprints can transform stakeholder perceptions of waste from being a cost center to a profit center, reduce carbon emissions by diverting waste from landfills, and stimulate innovation through the search for potential energy savings.

Firms that do not measure their sustainability footprints, for example, carbon, social, and water footprint, expose themselves to uncertainty and risk especially within the context of climate change as they fail to adopt behaviors or make decisions that are expressly sustainable.

This book utilizes the results of this study to provide strategic options for SMEs to embed sustainability and highlights the role of quality management in sustainable development.

Firstly, it is essential to briefly define the role of quality in sustainable development. As a quality practitioner, I reviewed the responses from practitioner bodies to the U.K. government’s consultation on a long-term focus for corporate Britain with some disappointment. I felt it did not define the centrality of the role of quality management and quality practitioners, managers, and entrepreneurs in assisting UK plc in maintaining a long-term focus.

Critically, in my opinion, the response from practitioner bodies was not as incisive regarding the following three issues:18

1.1 The Concept of Customer Satisfaction

A search on the Chartered Quality Institute (CQI) website for the word “customer” reveals a concept linked to the traditional process model interpretation of the definition as “a generic term for the person who buys goods or services from a supplier.”19

The Inability to Respond to the Dilemma Inherent in the Principal

The traditional process model of input–process–output intuitively recognizes waste as a result of economic activity but interprets waste as an unavoidable externality.

The quality profession has led the way in waste reduction by developing techniques and tools such as lean manufacturing and Six Sigma. However, these innovations were never designed to account for the effects of externalities such as carbon emissions resulting from global industrialization and fossil fuel consumption. From this perspective, the concept of the customer should be redefined to include all stakeholders affected by the activity of the organization. Extending the concept clearly redefines quality beyond the boundaries of mere product and service conformity to include its role in sustainable development.

1.2 The Decoupling of Quality from Sustainable Development

The Brundtland Commission’s seminal definition of sustainable development as “development that meets the needs of the present without compromising the ability of future generations to meet their own needs” has influenced all approaches to sustainability over the past two decades.20 Inherent in this definition is the concept of satisfaction of the “needs” of humanity, both present and future.

The quality profession is perfectly placed to assist businesses in reinterpreting their approach to sustainable development and investment by focusing efforts on the development of a sustainable culture based on the use of quality principles and techniques. The messaging of the importance and applicability of basic techniques, such as the plan–do–check–act cycle in implementing sustainable solutions to business functions, is steadily being usurped by a recent emphasis on the use of triple bottom-line reporting by organizations.

This has led, in some instances, to a distinct focus on economic, environmental, and social indicators to the detriment of quality and safety indicators. The result of this focus by corporations has contributed to product failures at Toyota21 and unfortunate but avoidable disasters such as the BP oil spill in the Gulf of Mexico.

1.3 The Inability to Respond to the Dilemma Inherent in the Principal-Agent Relationship

The recent financial crisis identified with terrific clarity the inherent failings of the principal-agent relationship. This is clearly demonstrated by the bankruptcy of Lehman Brothers in autumn 2008, when a lack of definition of the term “customer”, or a focus on customer satisfaction and the needs of the customer from the perspective of sustainable development, was at fault.22 The entire focus of the company was on short-term profits to the detriment of the principals; that is, shareholders, investors, and society. Lehman’s customer or principal in this context was global society, due to its size and reach. The board failed to understand their duty to society, and this translated into unsustainable practices, such as bonuses linked to purely financial indicators and investment decisions that resulted in the death of this 158-year-old institution.

It is imperative that the quality profession broadens its unique selling proposition beyond the traditional roles of quality assurance and ISO 9000 and extend its remit. The Japanese Union of Scientists and Engineers, American Society for Quality, and CQI should take the lead in disseminating knowledge on management systems in general including business continuity, risk management, and social responsibility, as these are evolving as major parts of the quality professional’s role and are expressed in ISO 26000, the new social responsibility standard.

This expansion is necessary if quality management is to continue to attract the individuals who can contribute to the development of the profession. I subscribe to the view that not only UK plc but also global economy can regain its competitiveness, but this can only happen if quality is placed right at the heart of sustainable development by focusing not on the management of quality but on the quality of management.

Secondly, regarding the strategic options for SMEs to embed sustainability, tools such as carbon footprint reporting are voluntary initiatives of which implementation costs are considered prohibitive except for those firms with near-monopolistic profits.23 Research studies also infer that sustainability footprints, for example, carbon footprint, by nature record historical impact and do not incorporate the views of future generations.24 The lack of utility of sustainability indices such as the Global Reporting Index as an indicator of an organization’s state of sustainability or absence sustainability and the difficulty in quantifying the benefits of sustainability footprints have seen its limited adoption by SMEs.25, 26 Significantly, research into sustainability footprint tools has focused on larger organizations with limited research into sustainability footprint reporting in SMEs.27, 28 Contemporary research reveals that the success of best practice initiatives, for example, carbon footprint measurement, seems to benefit from the organization having prior “built-in” capability.29 SMEs are also faced with a conundrum of short- versus long-term aims within the constraints of limited resources when adopting best practice initiatives, the value of which must be judged by the achievement, deployment, and overall sustainability of the capability generated by the initiative with implementation decisions being affected by the ability of management to apply sustainability models that have been “over engineered” precluding their suitability to the operational SME context.29, 30 This has contributed to an emphasis on “quick wins” when the long-term success of best practice initiatives requires ongoing support.29 Performance measurement tools such as carbon footprint reporting are voluntary activities as small businesses are not required to participate in carbon trading schemes such as the European Union Emissions Trading Scheme (EUETS) or unduly influenced by pressure from institutional investors.30 In the absence of direct grants or legal pressures to pursue sustainability initiatives, SMEs can be encouraged by the increased spending on energy, environmental, and sustainability initiatives by large customers despite recent global economic challenges and as such may be influenced to adopt sustainable business practices.31, 32

This book explores the key challenges facing businesses striving to embed sustainability, that is, philosophical, cultural, and social. The Sustainable Strategic Growth Model is provided as an option to overcome the key challenges regarding the incorporation of sustainability within strategy with four case studies outlining practical approaches in deploying strategic intent within the resource constraints of the SME operational context.

Through the implementation of the Sustainable Strategic Growth Model, organizations evolve from small businesses to Sustainably Managed Enterprises, the new SMEs.

In the race to exploit earth’s resources, commercialize space, and colonize future planets, we must aim to incorporate sustainability principles in our technological innovations. The choices are clear; our species Homo sapiens, which when translated from the original Latin means “wise man” must achieve sustainable development.

About the Author

Lowellyne James is the CEO of Sustainability & CSR Insights www.sustainabilitycsr.com and Course Leader of the MSc in Quality Management at the Aberdeen Business School. In his spare time he actively communicates his thoughts on Sustainability and Corporate Social Responsibility (CSR) on his website www.lowellynejames.com as well as his blog www.lowellynejames.blogspot.com. His new book Sustainability Footprints in SMEs – Strategy and Case Studies for Entrepreneurs and Small Business has been published by John Wiley & Sons.

Lowellyne James is the CEO of Sustainability & CSR Insights www.sustainabilitycsr.com and Course Leader of the MSc in Quality Management at the Aberdeen Business School. In his spare time he actively communicates his thoughts on Sustainability and Corporate Social Responsibility (CSR) on his website www.lowellynejames.com as well as his blog www.lowellynejames.blogspot.com. His new book Sustainability Footprints in SMEs – Strategy and Case Studies for Entrepreneurs and Small Business has been published by John Wiley & Sons.

References

1. Unknown. British Safety Council World heading for irreversible climate change, IEA warns. Feature Article; Dec 15, 2011.

2. Audubon. Audubon scientists find gulf birds & oil too close for comfort; 2010. Available at http://gulfoilspill.audubon.org/oil-and-birds-too-close-comfort. Accessed on Dec 2, 2013.

3. James L. BP’s deepwater horizon: a quality issue or a safety issue? Available at http://lowellynejames.blogspot.co.uk/ Accessed on Dec 5, 2013.

4. Moon and Back. JAXA and fishing net maker team up to catch space junk; 2011. Available at http://moonandback.com/2011/02/07/jaxa-and-fishing-net-maker-teamup-to-catch-space-junk/. Accessed on Dec 2, 2013.

5. Unknown. Safety. The North Star. Available at http://www.virgingalactic.com/overview/safety/. Accessed on Dec 2, 2013.

6. Unknown. Orbital Debris Mitigation. Available at http://orbitaldebris.jsc.nasa.gov/mitigate/mitigation.html. Accessed on Dec 2, 2013.

7. Nitto Seimo. Space debris removable. Available at http://english.nittoseimo.co.jp/13/9/. Accessed on Dec 2, 2013.

8. Unknown. World heading for irreversible climate change, IEA warns—British Safety Council. Feature Article, December 15, 2011.

9. Krysiak F. Risk management as a tool for sustainability. J Bus Ethics 2009;85:483–492.

10. Lash J, Wellington F. Competitive advantage on a warming planet. Harvard Bus Rev 2007;85(3):94–102.

11. Winter S. Knowledge and competence as strategic assets. In Teece D, editor. The Competitive Challenge. Cambridge: Ballinger; 1987. p. 159–184.

12. Hart S. A natural resource based view of the firm. Acad Manage Rev 1995;20(4): 986–1014.

13. Teece D, editor. Profiting from technological innovation: implications for integration, collaboration, licensing, and public policy. In The Competitive Challenge Cambridge: Ballinger; 1987. p. 185–220.

14. Porter M. Competitive Strategy. New York: Free Press; 1980.

15. Porter M. Competitive Advantage. New York: Free Press; 1985.

16. Porter M. The big idea: creating shared value. Harvard Bus Rev; January 2011; 89(1/2):62–77.

17. Porter M, Kramer M. Strategy & society: the link between competitive advantage and corporate social responsibility. Harvard Bus Rev December 2006;84(12):78–93.

18. James L. The CQI must expand its role. Available at http://www.thecqi.org/Knowledge-Hub/Qualityworld/Qualityworld-archive/Columns/Soapbox-March-2011/. Accessed on Dec 5, 2013.

19. Unknown. Customers. Available at http://www.thecqi.org/Knowledge-Hub/Knowledgeportal/Customers-and-stake-holders/Customers-/. Accessed on Dec 5, 2013.

20. Brundtland Commission. Our Common Future. Oxford: United Nations World Commission on Environment and Development; 1987.

21. Timeline Toyota’s recall woes. Available at http://www.theguardian.com/business/2010/jan/29/timeline-toyota-recall-accelerator-pedal. Accessed on Dec5, 2013.

22. Elliot L, Treanor J. Lehman Brothers collapse, five years on: ’We had almost no control’. Available at http://www.theguardian.com/business/2013/sep/13/lehman-brothers-collapsefive-years-later-shiver-spine. Accessed Dec 5, 2013.

23. Hicks M. BP: social responsibility and the easy life of the monopolist. Am J Bus 2010;25(2):9–10.

24. Holland L. Can the principle of the ecological footprint be applied to measure the environmental sustainability of business. Corp Social Responsib Environ Manage 2003; 10:224–232.

25. Demos T. Beyond the bottom line: our second annual ranking of global 500 companies. Fortune 2006; October 23.

26. Gray R, Bebbington J. Corporate Sustainability, Accountability and the Pursuit of the Impossible Dream. Available at CSEAR Website: http://www.st-andrews.ac.uk/~csearweb/researchresources/dps-sustain-handcorp.html. Accessed on Mar 20, 2012.

27. Price Waterhouse Coopers. Financial Times Stock Exchange Carbon Disclosure Project Strategy Index series 2010. http://www.ftse.com/Indices/FTSE_CDP_Carbon_Strategy_Index_Series/index.jsp. Accessed on Mar 20, 2012.

28. CDP 2010. Global 500 report. Available at https://www.cdproject.net/CDPResults/CDP-2010-G500.pdf. Accessed on January 1, 2014.

29. Done A, Voss C, Rytter NG. Best practice interventions: short-term impact and long-term outcomes. J Opera Manage 2011;29(5):500-513.

30. Hendrichs H, Busch T. Carbon management as a strategic challenge for SMEs. Greenhouse Gas Measure Manage 2012;2(1):61-72.

31. Unknown. Sustainable investment by large firms set to grow – British Safety Council Feature Article, March 8, 2012.

32. Unknown. Climate change report highlights need for business resilience – British Safety Council Feature Article March 22, 2012.