")

By Dan Prud’homme, Max von Zedtwitz, and Fernanda Arreola

The rise of Neo-populism presents risks to multi-national corporations in Western markets. The authors outline practical strategies corporations can take to combat such risks.

Populism is no longer a business risk confined to emerging markets. In fact, measured by the share of votes for anti-establishment parties, populism in developed economies is at its highest levels since the 1930s.1 Given the multiplicity of factors driving this “neo-populism” and the type of institutions shaping its evolution, multinational corporations (MNCs) need to respond to it differently than they have to classical populism. Neo-populism is directly or indirectly costing MNCs profit margins, customer loyalty, strategic footholds, and talented employees. It is manifested in Brexit, Italy’s recent elections, the Trump administration’s trade war, and populist party control of parliamentary seats in many European countries.2 It is leading to stringent security reviews of foreign acquisitions in the US and Europe and to fears of tightening immigrant policies. However, little practical advice is available regarding how to navigate these hazards.3 In this article, we discuss several ways that MNCs can weather neo-populism: (1) resetting risk scenario-planning differently than in classic populist regimes, (2) ramping-up creative stakeholder-engagement, (3) timing high-profile M&A better, and (4) localising smarter.

Populism, in the broadest sense, is a movement supporting ordinary people rather than those perceived as “elites” to hold powerful positions within governments.4 There are variants of how populism is more specifically conceptualised in some countries, for example France, compared to others.5 However, for our purposes, we define “neo-populism” as a set anti-establishment, authoritarianism, nativism, and anti-cosmopolitan values that underpin the political views of a growing number of people in the West today.6 Neo-populist sentiment takes the form of public opposition to liberal international trade and investment regimes,7 resistance to mass immigration and cultural liberalisation, and continuous protest against actions that are perceived as a surrender of national sovereignty to international bodies.8 These risks are cited among the top ten faced by MNCs operating in the US and Europe today.9

Neo-populism can also be seen as a consequence of the significant economic changes driven by businesses over the past few decades. The globalisation of value chains and rise in automation10 – while generally good for firms’ efficiency and productivity – have contributed to increasingly stark income inequality in favor of the higher classes of society.11 It has also resulted in unemployment in industries characterised by repetitive tasks and/or low-skilled labour.12 In the US, for example, the share of national income of the bottom 90% of the population held steady at around 66% from 1950 to 1980 but fell to just over 50% at the start of the financial crisis in 2007.13 This situation has created an identity crisis among many citizens.14 Further, information silos enabled by social media have catalysed and reinforced this upheaval.15 The multiplicity of these factors driving neo-populism in the West today distinguish it from classic populist movements. Trade, foreign investment, and immigration are most often blamed for these woes as they are perceived to create unfairness and because foreigners are attractive scapegoats.16

Another notable difference in neo-populism in developed countries today compared to traditional populism in developing countries is the way in which the ideology is to some extent restrained by relatively robust institutions (e.g., the rule of law, the formal free press, the chance to elect new leaders, and the independence of the academic community). These institutions are not always present in developing countries. At the same time, the grounding-effects that such institutions may have are somewhat offset by the aforementioned effects of information silos and social media, and, in some places, a rising polarisation in the formal free press. This new economic and political environment requires different responses from incumbent MNCs (IMNCs) and MNCs from emerging markets (EMNCs) relative to the strategies they have employed in classical neo-populist regimes.

[ms-protect-content id=”9932″]

An actionable perspective for neo-populism

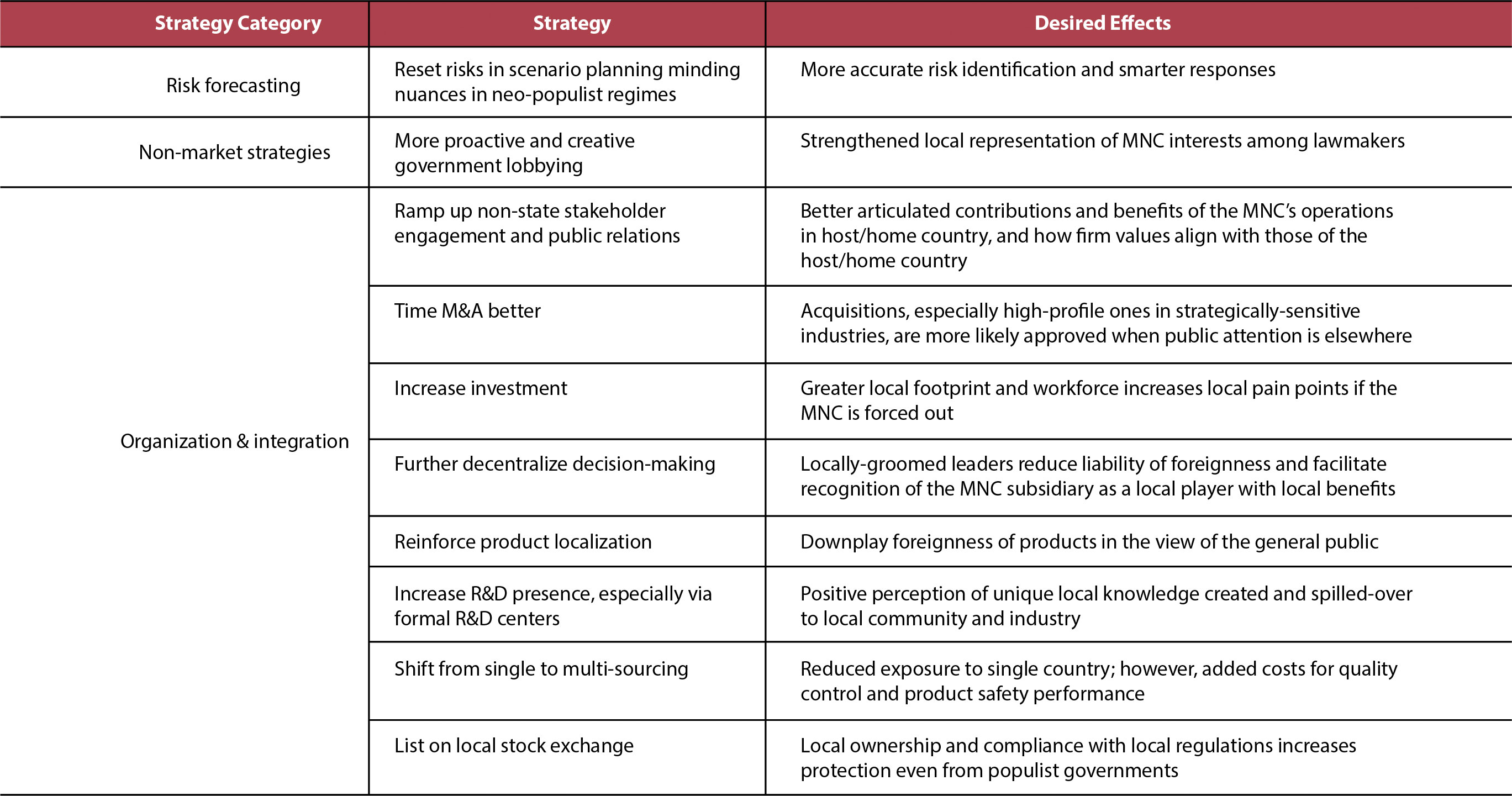

The new market and non-market17 conditions that current neo-populist economies impose on corporations require a diverse set of responses by MNCs. In this climate, firms face strategic choices to mitigate the negative effects of neo-populism and/or to benefit from positive effects of local-orientation. Based on the expertise and insights of several executives along with additional data and examples from MNCs established in these regions, we provide insights about how to respond to neo-populism. Table 1 summarises these responses which we then expound upon.

Table 1. Strategic responses to rising neo-populism

1. Risk forecasting: reset scenario planning minding nuances in neo-populist regimes

As mentioned, the multiplicity of factors driving neo-populism in the West distinguishes it from classic populist movements. Meanwhile, the long-term manifestations of neo-populism in policy, law, and other forms of institutional change is to some extent restrained by Western institutions in a way that is not always the case for populist movements in developing economies. Further, IMNCs often concentrate most of their operations in neo-populist markets whereas EMNCs are often new to these markets. These dynamics often require top management of MNCs to think about rising neo-populism somewhat differently depending if they are operating in their home market or a foreign host market. For instance, IMNCs operating in their home markets should think about ways to exploit neo-populism in their own interest and be wary of fighting it visibly. In contrast, EMNCs and IMNCs operating in a foreign host market should think of ways to mitigate its results. These dynamics are reflected in the recommendations throughout the remainder of this article.

The first important recommendation is to ensure a continuous assessment and revision of the frameworks used for identifying and measuring risk. These updates should be placed on the monthly, or even (if acute) the daily, executive agenda. They will require renewed scenario analyses of the likelihood that populist-related shocks to policy and law will take place and an evaluation of the magnitude of commercial hazards they pose.

Some MNCs are already following this logic and revising their risk forecasting frameworks. For example, Citigroup has recently released a new method for evaluating European equities taking into account neo-populist political risk.18 Risks from neo-populism span exchange rate volatility, various supply chain disruptions, changes in immigration policy (especially relevant for employing foreign talent), tax issues, and other areas, all of which need to be carefully delineated. For example, Panasonic, a Japanese electronics firm, has cited Brexit as the main reason for moving its European headquarters from the UK to the Netherlands. Firms operating amidst surging neo-populism that sell directly in high-risk industries or have suppliers in such industries need to be especially careful.

2. Non-market strategies: ramping up creative stakeholder-engagement

Ramped up non-market and marketing strategies can help MNCs navigate the dangers of neo-populism by explicitly considering political risks next to more economic-centric risks. Such non-market strategies may require MNCs to smarten up in the policy formulation process in key countries, an area that many firms are not well prepared for but in which they should especially vigilant and attentive. An obvious example of a smart approach in this regard is the mobilisation of many MNCs under the National Association of Manufacturers in the summer of 2018 to quietly lower US tariffs on hundreds of components produced in China that are used in US operations.19 Working quietly and directly with government officials in neo-populist states can help circumvent public criticism of pro-trade policies. This approach may also help MNCs to secure important allowances or even incentives to recruit and retain foreign talent – which is becoming increasingly challenging amidst proposed changes to US immigration policy, Brexit, and stricter immigration policies in some EU countries.

MNCs can also mitigate risks from neo-populism by contributing to certain important items on the political agenda of the host county’s government, such as job creation. Ford, an American auto manufacturer, has grappled with how to best do this amidst US neo-populism. In early 2017, Ford promised to scrap a plan to build a $1.6 billion car factory in Mexico and instead add 700 jobs in Michigan. Later that year it decided to go-ahead and assemble new battery-powered cars in Mexico rather than Michigan, but pledged to invest even more significantly in the Michigan plant, now focusing on self-driving cars. The importance of similar investment decisions is not only in their deployment but a pre-conceived marketing agenda that positions the discourse of corresponding choices within the media and amongst key politicians. Mass communication is key to effectively respond to neo-populism.20

A third non-market strategy considers the compatibility between firm discourse with the one held by key government officials. An example is the rivalry in the washing machines industry between US firm Whirlpool and competitors LG Electronics and Samsung Electronics, both from South Korea. Whirlpool, who employs thousands of union workers in the US, recently argued that these South Korean firms have undercut its US business by exporting washers at unfairly low prices. By building on the semantics of the Trump administration’s fight against foreign production of US consumed goods, Whirlpool engaged in an aggressive non-market strategy intent on garnering favor with US politicians to levy trade barriers against its South Korean rivals. Even when the strategic response to this movement was that both South Korean companies invested in new plants generating jobs in the US (LG is spending $250 million to build a 600-worker factory in Tennessee, while Samsung is investing $380 million to renovate a factory in South Carolina that will employ 950 people),21 this did not prevent the Trump administration from imposing a tariff of up to 50% on large residential washing machines penalising Samsung and LG. As positive reinforcement for the government’s decision, Whirlpool announced it was adding several hundred jobs in the US.

Of course, the liability of foreignness does not predestine all foreign MNCs to suffer from neo-populism. Nor does the so-called “liability of country of origin”, which is primarily an issue for EMNCs, such as those from China.22 One of the executives we interviewed from an auto MNC with operations in the US told us about their desire to adapt their non-market strategy. For instance, the firm is now engaging, for the first time, select factory workers at its plants in the US to reach out to state and federal lawmakers. The firm provides the workers with training about how trade and investment issues affect its US operations and then flies the workers to state capitols and Washington D.C. to lobby key politicians. The main message the workers pass to politicians emphasises the firm’s contribution to the US economy and society. Despite technically being a foreign firm, the workers highlight the firm’s contribution to the US in terms of jobs, production, and other economic value, as well as corporate social responsibility activities. While such messaging is not entirely new, the method of such outreach is more strategic and builds a new approach that is rooted not only in the host country but also its own citizens.

Both IMNCs and EMNCs can also benefit from heavily lobbying their home governments to negotiate with foreign host nations. This recently worked for ZTE, a Chinese MNC in the telecom equipment industry, who was able to facilitate a high-profile agreement between the US and Chinese government to limit sanctions imposed on the firm. Of course, not all firms will benefit from such explicit agreements. However, if and when a firm employs enough people in its home country in an industry of strategic importance, and if its home government is engaged with a smart non-market strategy, the home state has a strong incentive to proactively support the firm abroad.

In addition to a government-focused non-market strategy, our interviews suggest that both IMNCs and EMNCs can benefit from ramping up non-state stakeholder engagement and public relations. This can include stepping-up social and traditional media advertising campaigns to highlight how the firm’s values align with those of the host/home nation and otherwise contributes to the sustainability of that nation. The indirect societal benefits that firms offer are easily overlooked, so specialised skills are required to articulate them.

MNCs are well advised to engage the neo-populist public and governments even if, or sometimes especially if, they are often suffering from the effects of their neo-populist ideologies and policies. Firms, such as GM, Caterpillar, and Harley Davidson have reported that they are losing money due to neo-populist policies, especially new US tariffs on foreign steel and aluminum. Tech firms, such as Apple, are also being hurt by the US’ trade wars.23 A clearly failed response to this new environment is Harley Davidson’s poorly articulated public plan in 2018 to move production overseas in response to rising tariffs in the US. This mistake has resulted in Harley’s patriotic US consumer base rethinking their loyalty to what they thought was an “all American” company.24

3. Integration & organisation: time high-profile M&A better and/or localise smarter

Recent revisions to national security reviews in neo-populist states can complicate, if not fully scupper, attempts by foreign MNCS to merge with or acquire local firms. For instance, in the last three years, the inbound investment laws of the US, UK, France, Germany, Italy, and Lithuania, have all been made notably more restrictive.25

It appears that the risk of failing security reviews currently disproportionately affects Chinese EMNCs. Such firms are often seen as opaque extensions of the Chinese Communist Party’s allegedly strategic “mercantilism”. Many Chinese EMNCs are also seen as serious competitors, often supported by the state and with growing innovation and strategic capabilities.26 In 2016, almost $75 billion in Chinese overseas deals were cancelled, in part due to inward investment restrictions by neo-populist states.27 Most recently, in July 2018, the German authorities intervened to block a Chinese investor’s attempt to acquire Leifeld Metal Spinning, a German machine tool firm. This follows German state intervention earlier in 2018 to block the acquisition of Cotesa, a German aerospace company, by state-run China Iron & Steel Research Institute Group.

Our discussions with Chinese EMNCs indicated that the most straightforward response to these regulatory shifts was to delay acquisitions of US and European firms in sensitive industries in the short-term. Such acquisitions are more likely to be approved when public attention is elsewhere. Sensitive industries have traditionally included ones where dual-use (civilian and military) technologies are prevalent, but now also include new energy, banking, information technology, and a range of other high-technology industries, some of which the Chinese state has explicitly targeted as part of its “Made in China 2025” plan for economic and technological leapfrogging.

At the same time, not all Western countries are equally restrictive of Chinese investment. In fact, several central and eastern European countries, for example, Hungary, Bulgaria, the Czech Republic, Croatia, have recently attracted significant investments from Chinese EMNCs.28 Greece, and Italy are also embracing certain Chinese investments. These investments are, ironically, also part of rising neo-populism, fueled by a sense of disenfranchisement with the EU and the search for powerful yet distant partners in their quest to retain their independence. This phenomenon provides continued opportunities for Chinese and other EMNCs looking to make inroads into Western markets.

A related issue for firms and individual investors is the need to be careful about how they are funded. Chinese SOEs are not the only targets of neo-populist government suspicion. Recent research for the US Department of Defense has raised concern that much of the venture capital (VC) originating from China is orchestrated by the Chinese state to strategically sap the US of its crown jewel technologies.29 Similar concerns have recently been raised about Russian VC.30 In order to avoid regulatory hurdles that may accompany these suspicions, firms should seek to diversify away from such funding, at least in the near-term. This is understandably very difficult for domestic startups, the typical customers of VC investment, as they have limited options for internal funding and market entry timing is a major strategic concern.

In the case of MNCs, our interviewees suggested that, in addition to more cautiously approaching M&A and financing, MNCs need to re-evaluate their localisation strategies. The most intuitive strategy is to work on a “local” production strategy for all international products. By reducing any reminiscent foreignness of the MNC’s products, especially in consumer goods industries, it is more difficult for the general public – the source and target of neo-populist governments – to develop negative perceptions about the foreign firm and its products. The Japanese inventors of Pac-Man deliberately rebranded their product to sound more American in order to avoid US populist backlash in the early 1980s. Today, amidst neo-populism, Lenovo, a Chinese technology firm, has increasing pursued “agnostic branding”: positioning itself as a global technology firm rather than a Chinese one.

A more significant strategy is to localise leadership. This decentralisation of decision-making into populist countries ensures that there are high-level executives from such countries heading key corporate units. Such decentralisation should not be limited to merely local management but could also include top-level appointments to the global board of directors, as illustrated by the many Westerners sitting on the board at Lenovo. Local faces reduce the perceived foreignness of the MNC while increasing local influence and representation among key stakeholder groups. Of course, global management must still ensure that the local country management remains strategically aligned with the rest of the MNC.

Our interviewees suggested that to make an even stronger statement companies should consider the local establishment of strategic operations, such as R&D centres. R&D investments are the most desired form of FDI as they are pure cost-centres, i.e., foreign money pays for local salaries and taxes, creates local knowledge and spill-overs for the local ecosystem, and trains local talent. Local R&D centres also help quickly establish a “good local citizen” image – which is much needed when foreign MNCs, especially those from China, are increasingly viewed as raiders of Western technology with the only intent of helping themselves and the Chinese state. Setting up formal R&D centres can also enable bypassing of nationalist regulations, facilitate the localisation, and groom local talent for global leadership positions.

Shifts in sourcing arrangements might also be considered alongside new localisation initiatives, but should be approached with caution. On one hand, multi-sourcing is recommended for the non-strategic supply chain.31 On the other hand, multi-sourcing runs counter to the trends of supply chain integration, as well as streamlined product quality and safety performance improvement.

Last but not least, MNCs might consider local stock-market listings as a final tool to combat rising neo-populism. Listings raise local shareholder ownership and therefore protect the firm’s global leverage.32 This option is equally valid for IMNCs as it is for fast-developing startups and EMNCs.

Conclusion

We have outlined several practical strategies that MNCs can take to combat the risks posed by rising neo-populism in Western markets. These strategies include (1) resetting risk scenario-planning differently than in classic populist regimes, (2) ramping-up creative stakeholder-engagement, (3) timing high-profile M&A better, and (4) localising smarter. Of course, the strategies should not be considered in isolation: they should be aligned with the firm’s core values, profit orientation, culture, and organisation. If designed and implemented right, the strategies can make neo-populism far less of a business hazard than it may seem at present.

[/ms-protect-content]

Dan Prud’homme is an associate professor at EMLV Business School (École de Management Léonard de Vinci) (Paris, France). He is also a non-resident senior researcher at the GLORAD Center for Global R&D and Innovation at Tongji University (Shanghai, China).

Max von Zedtwitz is Professor at Kaunas University of Technology and Southern Denmark University, and Director of the GLORAD Center for Global R&D and Innovation. Previously, he was Professor at Tsinghua, Tongji, and Peking Universities in China, as well as Vice President Global Innovation for PRTM Management Consultants based in Shanghai.

Fernanda Arreola professor of Strategy, Innovation & Entrepreneurship at ESSCA. Her research interests focus on service innovation, governance, and social entrepreneurship. Fernanda has held numerous managerial posts and possesses a range of international academic and professional experiences.

References

1.https://www.foreignaffairs.com/articles/europe/201 6-10-17/europe-s-populist-surge

2.https://www.standard.co.uk/lifestyle/london-life/from-altright-to-neo populism-can-you-decode-the-new-political-lexicon-a3407491.html

3.Di Tella, R., Kenney, B., 2018. Trump’s populism: What business leaders need to understand. Harvard Business School Podcast. https://hbswk.hbs.edu/item/trump-s-populism-what-business-leaders-need-to-understand ?cid=wk-rss; Aragandona, A., 2017. Why populism is rising and how to combat it. Forbes. https://www.forbes.com/sites/iese/2017/01/24/why-populism-is-rising-and-how -to-combat-it/#23f960c21d44

4.Canovan, M., 1981. Populism. New York: Harcourt Brace Jovanovuch; McNamee, M., Kokkinogeni, A., 2018. How multinationals should be planning for Brexit. Harvard Business Review. https://hbr.org/2018/05/how-multinationals-should-be-planning-for-brexit

5.Nickisch, C., 2017. How France’s brand of populism differs from what drove Brexit and Trump. Harvard Business Review. https://hbr.org/2017/04/how-frances-brand-of-populism-differs-from-what-drove-brexit-and-trump

6.Mudde, C. 2007. Populist Radical Right Parties in Europe. NY: Cam bridge University Press; Inglehard, R., Norris, P., 2016. Trump, Brexit, and the rise of populism: Economic have-nots and cultural backlash. Harvard University Working Paper Series. https://research.hks.harvard.edu/publications/getFile.aspx?Id=1401

7. Rodrik, D., 2018. Populism and the economics of globalization. NBER Working Paper No., 23559. http://www.nber.org/papers/w23559.ack

8.Galston, W., 2018. The rise of European populism and the collapse of the center-left. Brooking Institution. https://www.brookings.edu/blog/order-from-chaos/20 18/03/08/the-rise-of-european-populism-and-the-col lapse-of-the-center-left/

9.BlackRock Investment Institute, 2018. BlackRock geopolitical risk dashboard. https://www.blackrockblog.com/blackrock-geopolitical-risk-dashboard/

10. Alessandro, F., Volker, K., Rasmussen, D., Sandel, M., 2018. Populism, liberalism, and democracy. Philosophy & Social Criticism 44; Bonikowski, B., 2016. Three lessons of contemporary populism in Europe and the United States. The Brown Journal of World Affairs 23, 9-24

11. Ebenstein, A., Harrison, A., McMillan, M., and Phillips, S. 2014. Estimating the impact of trade and offshoring on American workers using the current population surveys. The Review of Economics and Statistics, 96, 581–595; Rodrik, D., 2018. Populism and the economics of globalization. NBER Working Paper No., 23559. http://www.nber.org/papers/w23559.ack. See: Hicks, M. J., Devaraj, S. 2017. Myth and reality of manufacturing in America. Ball State University Center for Business and Economic Research; Autor, D., Dorn, D., & Hanson, G. 2013. The China syndrome: Local labor market effects of import competition in the United States. American Economic Review 103(6): 2121–2168; Acemoglu, D., Autor, D., Dorn, D., Hanson, G., Price, B., 2016. Import competition and the great US employment sage of the 2000s. Journal of Labor Economics 34, 141-198.

12. Ibid

13. Elliott, L., 2017. Populism is the result of global economic failure. The Guardian. https://www.theguar dian.com/business/2017/mar/26/populism-is-the-res ult-of-global-economic-failure

14. Norris, P., 2016. It’s not just Trump. Authoritarian populism is rising across the West. Here’s why. The Washington Post. https://www.washingtonpost.com/news/monkey-cage/wp/2016/03/11/its-not-just-trump-authoritarian-populism-is-rising-across-the-west-heres-why/?noredirect=on&utm_term=.d3dd782b2487 Galston, W., 2018. The rise of European populism and the collapse of the center-left. Brooking Institution. https://www.brookings.edu/blog/order-from-chaos/2018/03/08/the-rise-of-european-populism-and-the-collapse-of-the-center-left/

15. Higgins, M., 2017. Mediated populism, culture, and media form. Palgrave Communications 3. https://www.nature.com/articles/s41599-017-0005-4; Hameleers, M., Schmuck, D., 2017. It’s us against them: a comparative experiment on the effects of populist messages communicated via social media. Information, Communication & Society 9, 1425-1444.

16. Rodrik, D., 2018

17.http://lexicon.ft.com/Term?term=non_market-strategy.

18. Citigroup, 2017. European Portfolio Strategist: The MEGA trade and Europe’s political risk premium.

19. Sullivan, A., 2018. US Senate quietly votes to cut tariffs on hundreds of Chinese goods. Reuters: https://www.reuters.com/article/us-usa-congress-trade/u-s-sen ate-quietly-votes-to-cut-tariffs-on-hundreds-of-chinese-goods-idUSKBN1KG35R

20. Bach, D., Allen, D., 2010. What every CEO needs to know about nonmarket strategy. MIT Sloan Management Review. https://sloanreview.mit.edu/article/what-every-ceo-needs-to-know-about-nonmarket-strategy/

21. Martin, T., 2017. Samsung to invest $380 million in South Carolina factory for home appliances. Wall Street Journal. https://www.wsj.com/articles/samsung-to-in vest-380-million-in-south-carolina-factory-for-home-ap pliances-1498660270

22.Muralidharan E., Wei, W. Liu, X., 2017. Integrationby Emerging-Economy Multinationals- Perspectives from Chinese M&As. Thunderbird International Business Review 59.

23.https://www.amcham-shanghai.org/sites/default/files/2018-09/2018%20U.S.-China%20tariff%20report.pdf

24.Swan, A., 2018. Can Harley-Davidson survive tariffs and a consumer revolt? Forbes. https://www.forbes.com/sites/andyswan/2018/07/24/harley-davidson -revolt/#4ba2f5574d7c

25.UN, 2018. World Investment Report: Investment and New Industrial Policies, p. 84. http://unctad.org/en/PublicationsLibrary/wir2018_en.pd f; UN, 2016. World Investment Report, p. 96. http://unctad.org/en/Pub licationChapters/wir2016ch3_en.pdf#page=6

26.Prud’homme, D., von Zedtwitz, M., 2018. The changing face of innovation in China. MIT Sloan Management Review. https://sloanreview.mit.edu/article/the-changing-face-of-innovation-in-china/

27. Jones, C., Espinoza, J., Hancock, T., 2017. Overseas Chinese acquisitions worth $75bn cancelled last year. Financial Times. https://www.ft.com/content/b0ff426c -eabe-11e6-930f-061b01e23655.

28. Allen-Ebrahimian, B., Tamkin, E., 2018. Prague opened the door to Chinese influence. Now it may need to change course. Foreign Policy. https://foreignpolicy.com/2018/03/16/prague-to-czech-chinese-influence-ce fc-energy-communist-party/

29.Brown, M., Singh, P., 2018. China’s technology transfer strategy: How Chinese investments in emerging technology enable a strategic competitor to access the crown jewels of US innovation. Report for the US Department of Defense. https://admin.govexec.com/media/diux_chinatechno logytransferstudy_jan_2018_(1).pdf

30. Dorfman, Z., 2018. How Silicon Valley became a den of spies. Politico. https://www.politico.com/magazine/story/2018/07/27/silicon-valley-spies-china-russia-219071

31. Sheffi, Y., 2016. Second Thoughts on Second Sourcing. https://sloanreview.mit.edu/article/second-thoughts -on-second-sourcing/

32. The Economist, Jan 21, 2017. Business can and will adapt to the age of populism. https://www.economist.com/business/2017/01/21/businesses-can-and-will-a dapt-to-the-age-of-populism