")

By Howard Yu and Jialu Shan

The average lifespan of companies is becoming shorter. For them to survive the competition it is important to learn to jump across knowledge disciplines and create new knowledge about how a product is made or a service is delivered. Using the Leap Readiness Index, the authors measure the readiness of financial institutes to leap to a new frontier of know-how to prepare for the future.

It’s common knowledge among executives that while humans now live longer, companies die faster. In 1958, the average lifespan of companies listed in Standard & Poor’s 500 Index was 61 years. Now it’s less than 18 years, according to a study conducted by McKinsey. Others have suggested that nearly 50% of the companies currently in the S&P 500 Index will be replaced over the next 10 years. These companies will be bought out or merged or go bankrupted, like Enron and Lehman Brothers and Polaroid and Kodak. And those who escape may still struggle to restore their former fortune, such as General Electric, Panasonic, Sony, ABB, Citigroup, UBS, and the like.

Every CEO is presumed to understand that, and also every executive, whose c-suite office either is or isn’t situated at a current S&P 500 company. It’s therefore no surprise to these executives that in 2019, the impetus is to leverage connectivity and artificial intelligence as part of their corporate strategy. No carmaker, for instance, will speak to investors without mentioning “future mobility.” BMW is a “supplier of individual premium mobility with innovative mobility services.” General Motors aims to “deliver on its vision of an all-electric, emissions-free future.” And Daimler, the maker of Mercedes, sees the future as “connected, autonomous, and smart.” In fact, automakers are on the cusp of making a major leap in their know-how from mechanical engineering with combustion engine experts to that with electric and programming experts—the same kind who build computers, mobile games, and handheld devices. In contrast to personally owned, gasoline-powered, human-driven vehicles that dominated the last century, carmakers realise that they have to transition to mobility services based on self-driving electric vehicles that will be paid for by the trip, by the mile, through a monthly subscription, or through a combination of all three.

[ms-protect-content id=”9932″]

One defining character of pioneering companies that stay ahead of their competitors is that they leap: they jump across knowledge disciplines to leverage and create new knowledge about how a product is made or a service is delivered. The best companies leap repeatedly. Absent such efforts, latecomers will catch up.

In a similar vein, in consumer banking, it’s a shift from operating a traditional retail branch with knowledgeable staff who provide investment advice to running data analytics and interacting with consumers the same way an e-commerce retailer does. Leap is everywhere, although the pace of change may differ between industries.

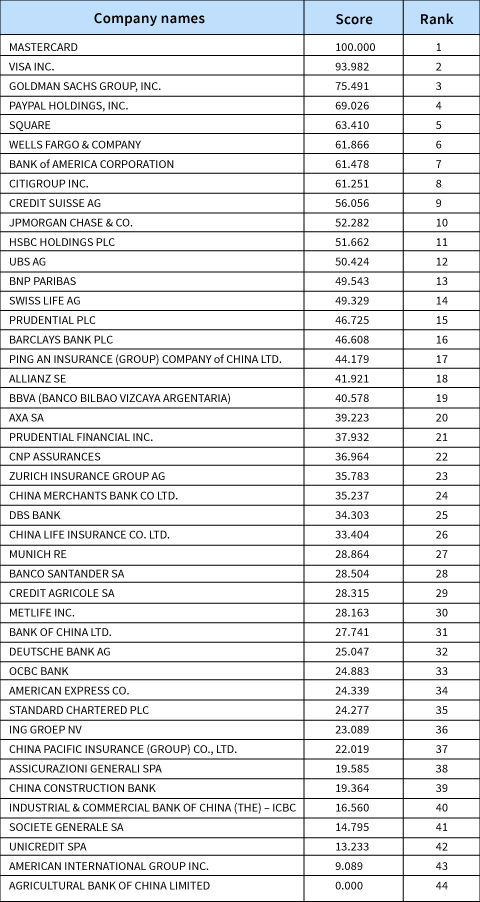

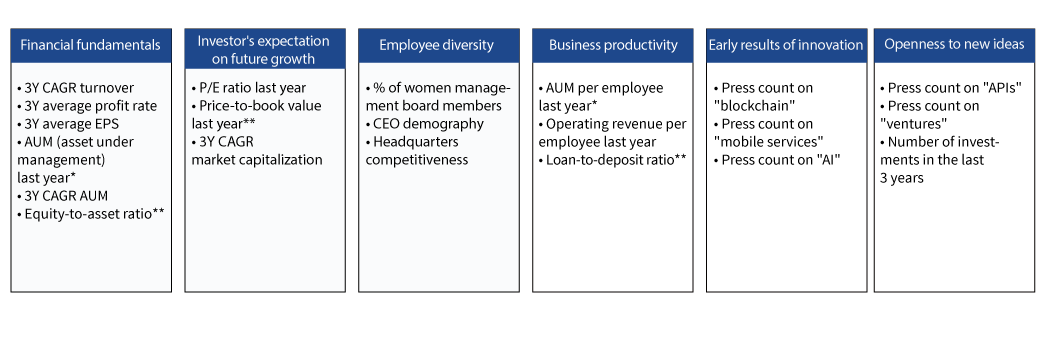

And so at the IMD business school, we track how likely a firm will successfully leap to a new knowledge discipline in its effort to prepare for the future. This IMD ranking measures companies in each industry sector using hard market data—data that is publicly available and has objective rules—rather than relying on soft data, such as polls or subjective judgments of raters. We measure fundamental drivers that fuel innovation, such as the health of a company’s current business, the diversity of its workforce, its governance structure, the investments it has made against its competitors, the speed of its product launches, and so on. Using an objective composite index that accounts for these drivers, table 1 measures the readiness of each of the listed financial institutes to leap to a new frontier of know-how and is specifically relevant to the financial sector: robo-advisors and artificial intelligence, cryptocurrency and blockchain, mobile banking and mobile payment, corporate venture and application programming interfaces (APIs).

Unsurprisingly, the leap readiness index in table 1 listed a few household names of fintech developers. PayPal, a digital payment firm that turns 20 this year, and Square, which processes credit card payments for street stalls, coffee stands, and fancy farmers’ markets, both sit on top of the ranking. More surprising are the incumbents, who are able to grow just as fast. None are retail banks, who supposedly enjoy the advantage of “being close to consumers” and are able to “amass mountains of user data.” The leading incumbents, it turns out, are the legacy infrastructure builders: Visa and Mastercard.

Since the dawn of the smartphone era, too many new entrants that provide payment methods—Apple Pay, Google Wallet, Square, PayPal, Vimeo, and Revolut, just to name a few—have all proven themselves powerful innovators who could design offerings that consumers crave and have thus carved out segments of the market away from the credit cards that retail banks issue. And in the face of these new entrants, the only proven strategy that Visa and Mastercard can rely on to maintain the relevance of their legacy infrastructure is to bypass their own plastic, de-emphasising and destroying the very physical embodiment of their offering that had been so cherished for decades, and to allow these disruptors to connect to their own toll road. If you can’t beat them off, let them join.

It should therefore come as no surprise that at the Apple event in March this year, during which the Apple card was announced, one would have noticed in that “subtle off-white coloring” and “the tasteful thickness of it” was the Apple logo emblazoned in all its minimalist design, promising breakthrough features such as no fees of any kind and A.I. software that actively encourages users to avoid debt and provides recommendations to pay it off quickly. Sharing space on that minimalist design on the back side of the card are the logos of Goldman Sachs—the underwriter—and Mastercard. Not even Apple can shake off the legacy network.

And it’s not just Apple, PayPal, Square, Samsung Pay, Google Pay, Facebook Credits, Stripe, and even Coinbase, a cryptocurrency upstart—all work with Visa and Mastercard. In other words, no fintech can disrupt anything unless they pay a toll fee to the old boys’ network. The reason is simple: an interface standard has emerged that has made Visa and Mastercard so simple and powerful to work with that their vast networks are irresistible for any fintech: application programming interfaces.

In the simplest of terms, an application programming interface, or API, is an official set of rules and guidelines that facilitates the exchange of information between two pieces of software. These software routines, protocols, and tools can therefore allow third parties to tap into Visa and Mastercard’s infrastructure. “While many legacy bank players have been hesitant to see Visa as primarily a technology company,” observed Gilles Ubaghs, senior analyst of financial services technology at Ovum, “the recent launch of Visa’s Developer platform, . . . with a host of APIs offering a full mix of payment functionality, all built on Visa’s underlying core network, Visa is opening up its full capabilities directly to the broader digital ecosystem.”

The major breakthrough here, then, is the realisation that a product’s best feature will never be invented in-house. Visa and Mastercard realise that killer apps must be invented by third parties, who are closer to their own customers. The same can be said of Steve Jobs: No matter how perceptive he was about consumer desires, he couldn’t have possibly predicted that some of the most prominent functions of his iPhone would be used to hail a cab (Uber) or to take pictures that would be automatically erased (Snapchat). No single company could have come up with both of these killer apps. Product design decisions are always enhanced with input from varied, independent sources. For someone who runs a legacy infrastructure, the best strategy is to allow others to discover new usages for the existing system while reinventing it by setting a new standard for the industry.

It might happen one day that credit cards will disappear, but Visa and Mastercard will still be ubiquitous, still making all the hard parts of sending and receiving money around the world look easy.

Now, what’s the leap your company must make?

Notes * For payment companies, we use “the amount of transactions” as a proxy. **We treat payment companies differently than other financial service companies. All of our 21 indicators are hard data; that is, they are publicly available in company websites, annual reports, press release, news, and special reports on topics such as corporate social responsibility. For press counts data, we consulted Factiva, a global news database that covers various premium sources, and counted the number of press releases on each trending topic that was identified previously in this sector for the past 3 years (2016–2018). The data was also supplemented by third-party data sources from Crunchbase, which specialises on the topic of corporate venturing. To calculate the index, first, we collected historical data for each company. Then we performed calculations for each indicator (e.g., 3Y CAGR) before we standardised the criteria data. Next, we aggregated indicators to the six main factors and then determined the overall ranking. For the purpose of comparison, we ranked each company from 1 (best) to 44 (worst) on a scale of 0 to 100.

[/ms-protect-content]

About the Authors

Howard Yu is the author of LEAP: How to Thrive in a World Where Everything Can Be Copied (PublicAffairs, 2018), LEGO professor of management and innovation at the IMD Business School in Switzerland, and director of IMD’s signature Advanced Management Program (AMP). A native of Hong Kong, he earned his doctoral degree from Harvard Business School.

Howard Yu is the author of LEAP: How to Thrive in a World Where Everything Can Be Copied (PublicAffairs, 2018), LEGO professor of management and innovation at the IMD Business School in Switzerland, and director of IMD’s signature Advanced Management Program (AMP). A native of Hong Kong, he earned his doctoral degree from Harvard Business School.

Jialu Shan is a Research Associate at The Global Center for Digital Business Transformation – An IMD and Cisco Initiative.

Jialu Shan is a Research Associate at The Global Center for Digital Business Transformation – An IMD and Cisco Initiative.