By Niccolò Pisani and Omar Toulan

Whereas facts suggest that German companies are among the best equipped and most active to pursue global growth, they offer limited insight to determine the real extent to which these companies are truly global. This article aims to offer a data-driven, rigorous, and comprehensive assessment of their actual degree of internationalisation and compare it with the one of other large enterprises based in the rest of the world.

Being global brings strong strategic advantages to companies. In comparison to firms whose scope is limited to their home countries, global corporations are able to access more customers, acquire privileged resources, establish partnerships with foreign counterparts, reach scale and scope economies in their global operations, and take advantage of cross-country arbitrage opportunities. Having said that, being global also entails additional costs and creates specific challenges to companies. Global corporations need to manage complex networks of inter-firm relationships that span beyond national boarders, face unfamiliar risks in relatively less-known host environments, and struggle with the persistent challenge to locally adapt while preserving consistent global processes.1

Despite the challenges associated with global operations, to expand internationally is nowadays more critical than ever, especially for large companies based in developed economies, as opportunities for growth reside primarily in emerging markets.2 To be able to reap the benefits of the big shift of economic activity to emerging economies, corporations need to rethink their global footprints and remain on top of all the changes that such shift is implying in the international competitive landscape. These include the need to compete against new international players primarily based in emerging economies, access new foreign customers, reconsider their organisational structures to fit the changing environment, and develop global-leadership competencies.3

Within Western Europe, German companies have been traditionally considered leaders in keeping up with technological- and market-related environmental changes. On the industrial side German manufacturers are known to be at the technological frontier. Country-level data gathered by UNCTAD also corroborate that German companies are among the most internationally-oriented.4 Germany is in fact one of the largest exporters in the world.5 Whereas these facts suggest that German companies are among the best equipped and most active to pursue global growth, they offer limited insight to determine the real extent to which these companies are truly global. Are German companies more globalised than firms based in other countries? Stated otherwise, are German companies leading the way in terms of adopting a true global footprint to keep up with the big shift of economy activity to emerging economies?

German companies appear as more nationally- and home region-oriented than Western European companies included in the FG500. This also implies that German companies’ global orientation is weaker than their Western European counterparts.

To provide an answer to these questions, we collected data on the 100 largest corporations based in Germany according to their turnover and calculated multiple indicators to determine their actual degree of internationalisation. To be able to contextualise the findings obtained vis-à-vis other large corporations located in other countries, we repeated the same analysis for the world’s 500 largest firms as included in the Fortune Global 500 (FG500) and compared the results obtained. Whereas the 100 largest companies based in Germany obviously have an average lower annual turnover than FG500 firms, all companies included in both samples can be categorised as “large” enterprises according to “Eurostat” and are therefore comparable for the purpose of our study.6,7

Several works in the field of international business have classified the degree of firm-level internationalisation adopting various measurements and indicators that range from the distribution of firms’ sales to the degree of nationality diversity in their top management teams.8 To offer a comprehensive assessment of the extent to which German companies are internationally-oriented, we considered multiple dimensions in our analysis and thus focussed on sales, assets, shareholders, board of directors, and top management teams.

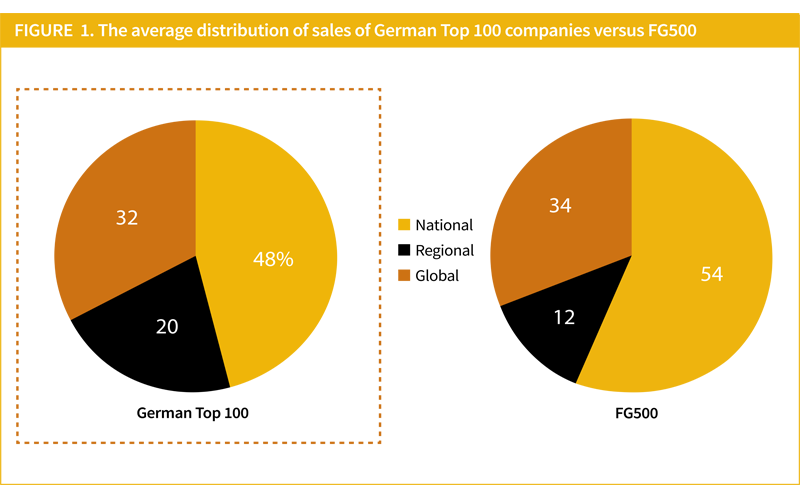

In relation to sales, we gathered information on the geographic distribution of revenues reported in each company’s annual report9 and distinguished among sales within the firm’s home-country (national), international but within the home region (regional), and outside the home regional boundaries (global).10 The comparison (see Figure 1 previous page) shows that German companies’ average revenue distribution is similar to the one of the average FG500 firm with respect to the propensity to go global. Having said that, differences arise when looking at the proportion of national and regional sales. Whereas German corporations tend to be relatively less nationally-oriented than their FG500 counterparts, they show a greater propensity to operate within their home region, this being the likely result of the high level of regional integration within the European Union.

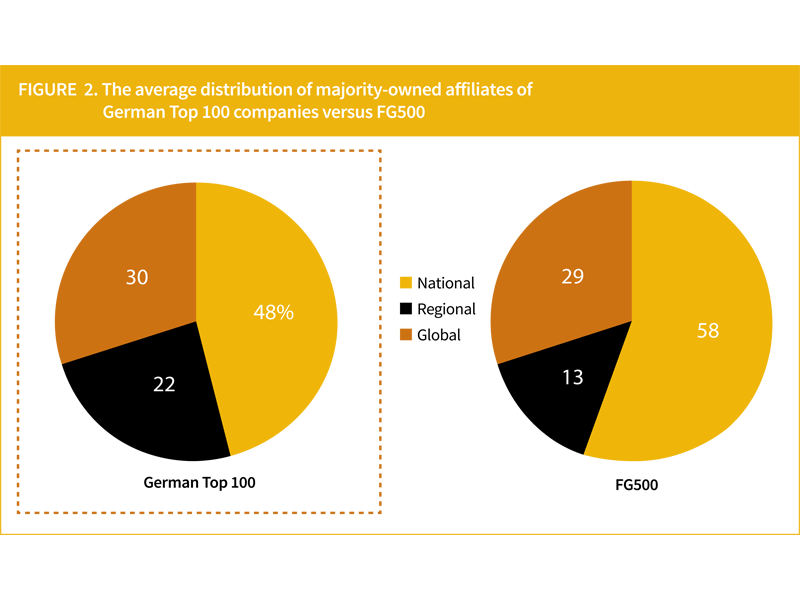

We then considered the geographic distribution of subsidiaries and thus created a dataset that included all majority-owned affiliates of the 100 largest German firms (over 19,000 data points) and did the same for the companies included in the FG500 (the resulting dataset for the FG500 sample comprised over 67,000 data points). We calculated the distribution for each firm in the two samples and reported the resulting averages in Figure 2 above. The pattern that emerges is comparable to the one obtained relative to the distribution of sales. Whereas significant differences are noticeable in the national versus regional orientation, the propensity to locate majority-owned affiliates outside the home region is practically identical in both samples.

Within Western Europe, German companies have been traditionally considered leaders in keeping up with technological- and market-related environmental changes.

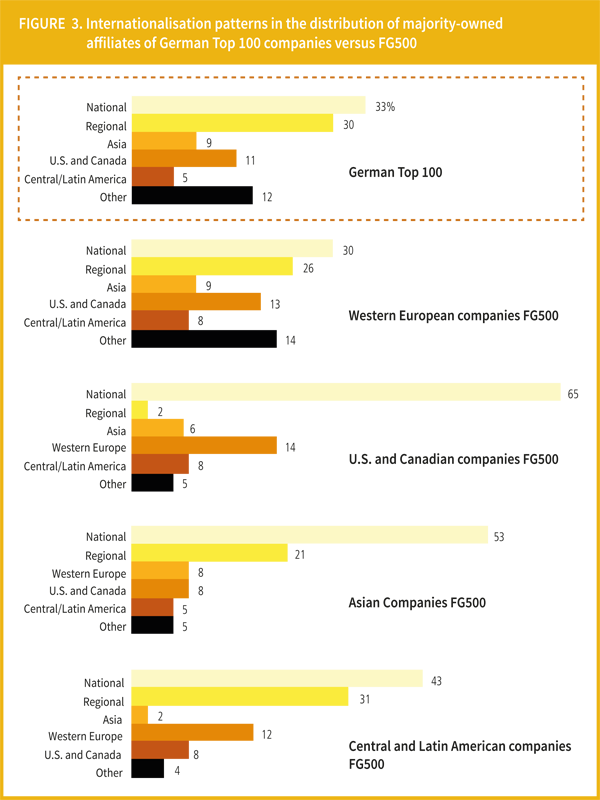

More pronounced dissimilarities materialise when considering the overall distribution of all majority-owned affiliates and differentiating among the region of origin of FG500 firms (see Figure 3 next page). German companies appear as more nationally- and home region-oriented than Western European companies included in the FG500. This also implies that German companies’ global orientation is weaker than their Western European counterparts. Looking at the specific propensity to establish majority-owned affiliates outside Europe, German corporations have a relatively higher portion of majority-owned affiliates in the Asian region than North American corporations and, to an even greater degree, of Central and Latin American companies. It is worth of note that FG500 companies based outside Western Europe all report a much stronger national orientation than German companies, with U.S. and Canadian companies locating up to 65% of their majority-owned affiliates at home. Overall, the analysis based on majority-owned affiliates suggests that German firms are among the most active internationally, but not considerably more than Western European companies included in the FG500.

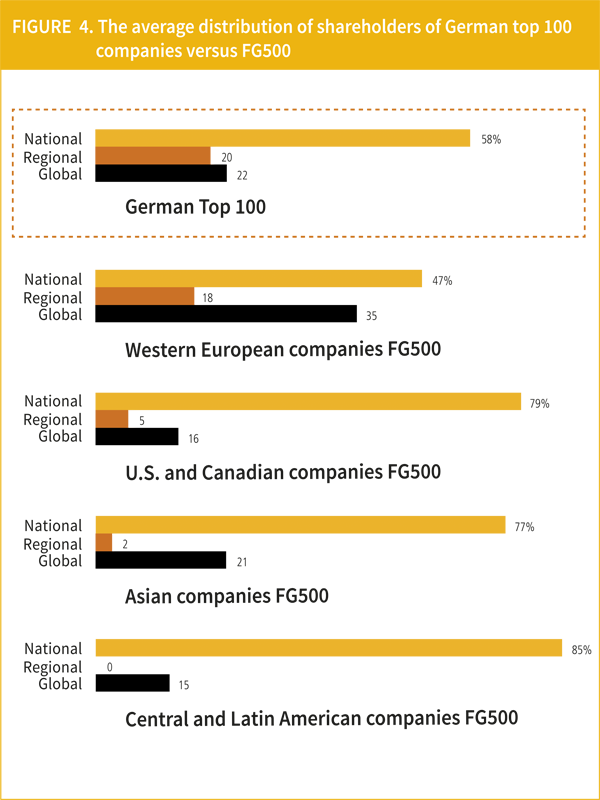

We also considered shareholders’ nationality as their geographic distribution may provide a useful indicator to understand the international orientation of firms. For this purpose, we collected data on the country of origin and total stake owned for each of the main shareholders of the 100 largest German corporations and did the same for all the companies included in the FG500. Data for the German sample were available for 73 firms (377 companies for the FG500 sample) and led to the creation of a dataset with over 2,900 data points (over 24,000 for the FG500 sample).11 The results obtained (reported in Figure 4) show that German companies have, on average, a significantly higher share of national shareholders when compared with their Western European counterparts. Moreover, our findings also illustrate that the portion of shareholders coming from outside the European Union is substantially smaller than the one of the largest Western European corporations included in the FG500. This may be associated with the fact that whereas stock exchanges in other Western European countries have merged creating larger platforms (e.g., Euronext), global investors need to access Deutsche Börse to acquire equity of German-based companies. Looking at the average geographic distribution of the largest corporations based in other world’s regions, our findings illustrate a marked predominance of national ownership, with intra-regional ownership losing relevance when moving away from Western Europe. Given the overall marked home-country bias reported across all regions, the findings we obtained suggest that the average distribution of shareholders may not be the most insightful indicator to grasp nuanced differences in the internationalisation patterns of large corporations.

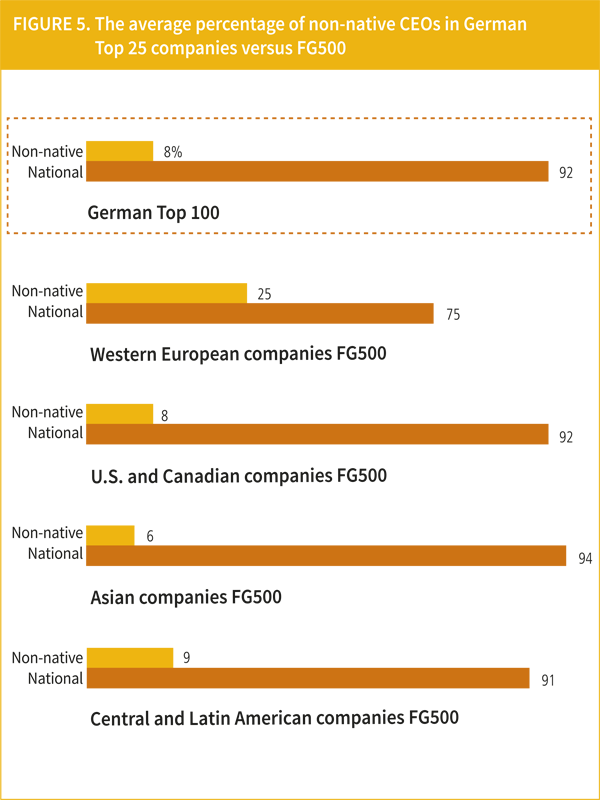

Recent research has highlighted that the C-suite of the world’s largest corporations is not as globalised as conventional wisdom may suggest.12 Looking at CEOs’ country of origin for example, only nearly 13% of companies included in the FG500 had a non-native CEO, i.e. whose main nationality was different from the country where the corporation had its headquarters. Figure 5 below reports the average percentage of non-native CEOs in the 25 largest corporations based in Germany and compares it with their FG500 counterparts. Our findings indicate that German companies have a much smaller propensity to hire a non-native CEO than other Western European corporations. Their likelihood of hiring a foreign national (8%) is equivalent to the one of North American companies, and anyway meaningfully inferior than the overall FG500 average (13%). One potential explanation for this result may be linked to the fact that German companies primarily use German as reference language in their headquarters, making it very difficult for international CEOs to be hired unless they are fluent in German. Not surprisingly, 70% of the non-native CEOs in Western European companies included in the FG500 are based in the U.K., Netherlands, and Switzerland – three countries where English is commonly used in the headquarters of large corporations.

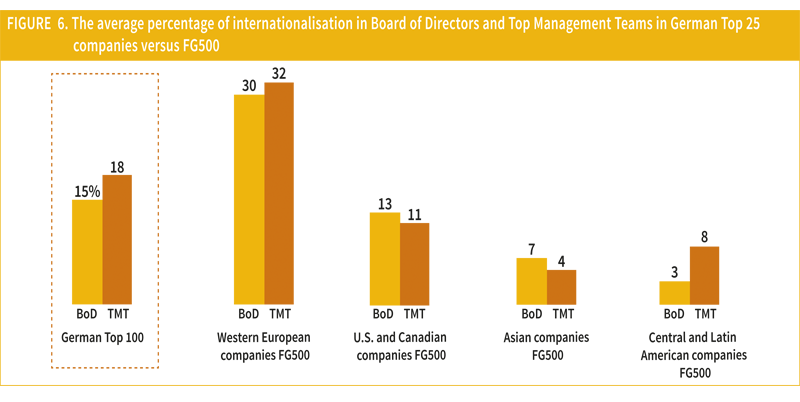

While CEOs’ results suggest a relatively limited exposure to foreign markets in terms of hiring key executives, we looked at the composition of both boards of directors and top management teams to investigate whether this pattern was confirmed. Thus, we gathered data on the nationality of each member of the board of directors and top management team of the 25 largest German corporations and did the same for the FG500 sample. Our findings (see Figure 6) show that German board of directors and top management teams are substantially less internationalised than their Western European counterparts, this being the likely result of the language barrier issue discussed in the previous paragraph. In relation to the North American sample, our results show that U.S. and Canadian companies continue to have a strong home-orientation when it comes to decide the composition of boards of directors and top management teams.13 Overall, the average degree of internationalisation of German companies’ corporate elites appears as more similar to the North American sample than the Western European one. In particular, companies based in the U.K., Netherlands, Switzerland, Belgium, Finland, Ireland, and Luxembourg report an average percentage of internationalisation that is greater than 35% in both their board of directors and top management teams.

German companies have, on average, a significantly higher share of national shareholders when compared with their Western European counterparts.

Our analysis shows that the 100 largest German corporations are less internationalised than Western European firms included in the FG500. Their pattern of internationalisation is rather similar to the average FG500 company with respect to sales and location of majority-owned affiliates, with their distribution being very comparable to other Western European companies especially with respect to their global orientation. In relation to their equity base, our results indicate a relatively strong predominance of national investors. This may partially explain the marked prevalence of German nationals in their board of directors and top management teams as well as their lower-than-average propensity to hire non-native CEOs. Thus, even though country-level data indicate that German firms are among the most active internationally via strong exports of their products and substantial foreign direct investments worldwide, our in-depth analysis of the 100 largest German companies shows that their degree of globalisation remains relatively limited on multiple accounts and anyway not greater than large companies located in other countries, especially within Western Europe. Of course, these averages mask major variations across individual companies. Moreover, the aim of this study was not to determine whether Germany’s largest corporations should be more or less international than what they currently are. The objective of our work was to offer a data-driven, rigorous, and comprehensive assessment of their actual degree of internationalisation and compare it with the one of other large enterprises based in the rest of the world. To this end, our findings suggest that, as much as FG500 companies are not as global as one may imagine,14 the same can be argued for Germany’s largest corporations.