By Fredrik Weissenrieder and Daniel Lindén

Adapted from Redesigning Capex Strategy

Capital expenditures are at the heart of any company’s future. Unfortunately, almost all industrial companies get capital expenditures (capex) wrong. Why? Because capex projects aren’t considered within a broader perspective of the company’s long-term strategy, its total production footprint, customer expectations, and the overall marketplace.

In this article, we explain the right way to create a long-term capex strategy.

The Problem Starts Here

Different companies have different ways to measure the value of a capex project. Some use net present value (“NPV”) or an internal rate of return (“IRR”) while others may simply use payback periods or some mix thereof. Regardless of how they gauge performance, every company we’ve ever worked with or heard of uses metrics based on one common principle: the difference (or “delta”) between a production asset’s cash flow with the capital expenditure and the asset’s cash flow without it.

A Hypothetical Example

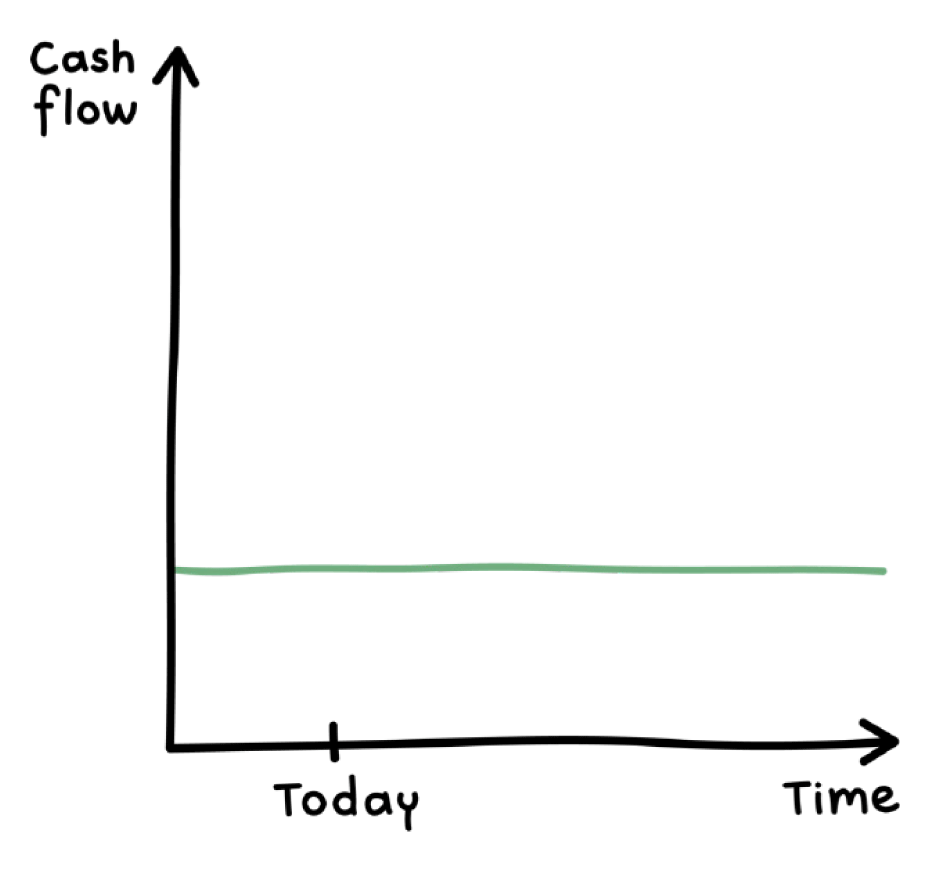

We’ve found the most straightforward way to explain why cash flow deltas are misleading is to use a simplified illustration of a hypothetical company with three production sites. Let’s say Quality Pulp Manufacturing, Inc. has three pulp mills. Its Baton Rouge, Louisiana, mill has been in operation for about twenty years. Quality Pulp assumes the mill will maintain its operations for the foreseeable future as it has over the last twenty years. When we graph its normalized cash flows over the last few years and project them into the future, it results in the following graph:

The executives at Quality Pulp expect that Baton Rouge will require a number of capexes over time. Machinery and equipment wear out, the market expects a certain level of quality, and so forth. In fact, the company has already made several such investments.

The mill manager sees that quality has become a real issue for his customers. No one at the corporate office is surprised when the manager submits a capex request. Between discounts, re-runs, and losses to the competition, the mill’s performance is down. “But,” the manager says, “with this capex, things will go back to normal.”

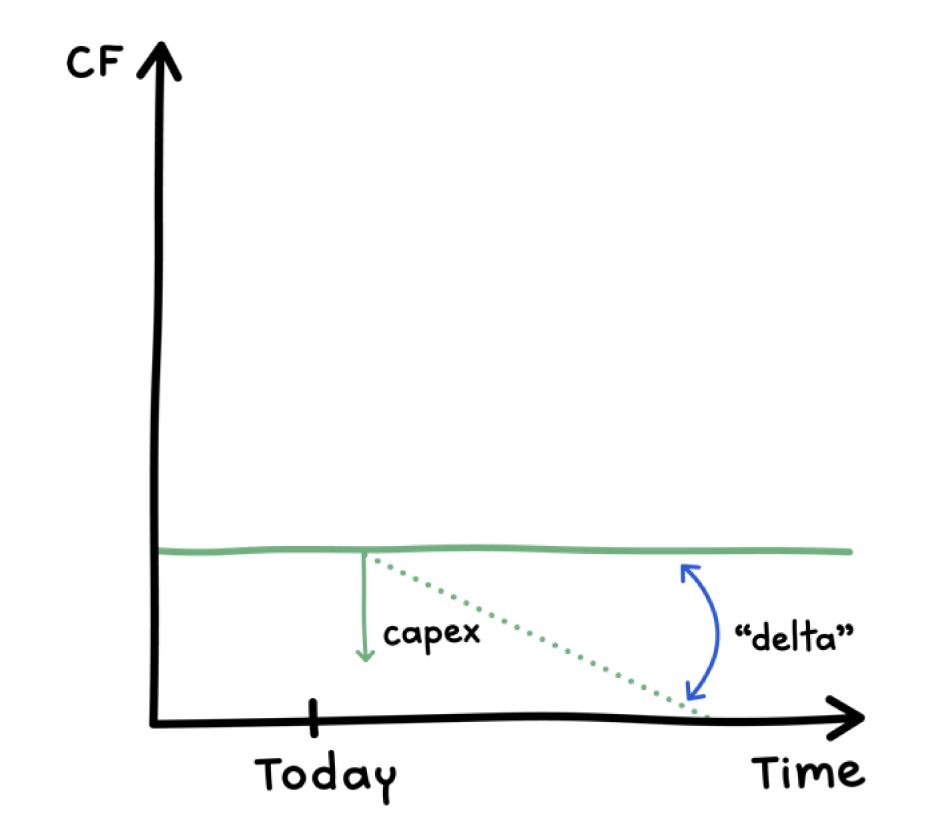

Corporate has two options. They can deny the request, in which case the mill’s cash flow will soon decline, and without any further intervention, the mill itself will eventually become obsolete. Or they can allocate a portion of the capital budget for this capex request. This will allow Baton Rouge’s cash flow to continue as it has been.

The following graph shows the cash flows of the two different options. If corporate had denied the request, cash flow would have fallen (as depicted by the dotted line). Or they could make a one-time capital expenditure to maintain nominal cash flow. The difference between the two cash flows is called the delta.

The number crunchers at Quality Pulp convert the capex cash flow delta into today’s equivalent value and arrive at a net present value (NPV) of $30. (This $30 could mean $30,000 or $30 million; these calculations scale to any size capex project.) The number crunchers also find that the project has a payback of twenty-four months.

There’s a known quality issue, a positive NPV, and a quick payback: To everyone involved, this looks like a good capex decision. Corporate approves and earmarks the funds in the coming year’s capex budget.

Another Capex Request

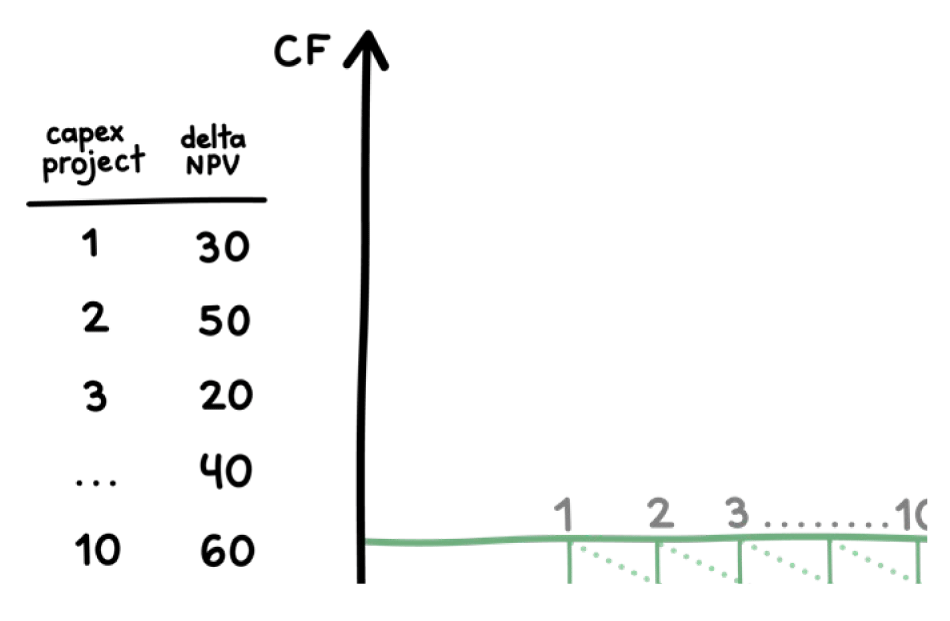

Three months later, the mill manager submits another capex request. The wood yard has an issue that’s beginning to become a real cost problem. The company goes through the whole capex analysis process again. The result shows a positive cash flow delta with a solid NPV of $50 and a payback of thirty months. Corporate approves the request.

This pattern continues over the next two years. The screens need to be replaced. An evaporator needs to be refurbished. A conveyer needs to be upgraded. Each time, corporate faces the stark choice: Do nothing and let cash flow fall. Or make the investment to maintain it. The NPV total of these projects is $200, representing the accumulated benefit from all capex projects.

If we were to graph those ten projects from today’s vantage point, we see that without each subsequent capex invested, Baton Rouge’s cash flow will fall. The site will eventually become obsolete. But none of these capexes fundamentally improves the mill’s performance. Each one merely postpones its obsolescence.

Let’s Look At The Bigger Picture

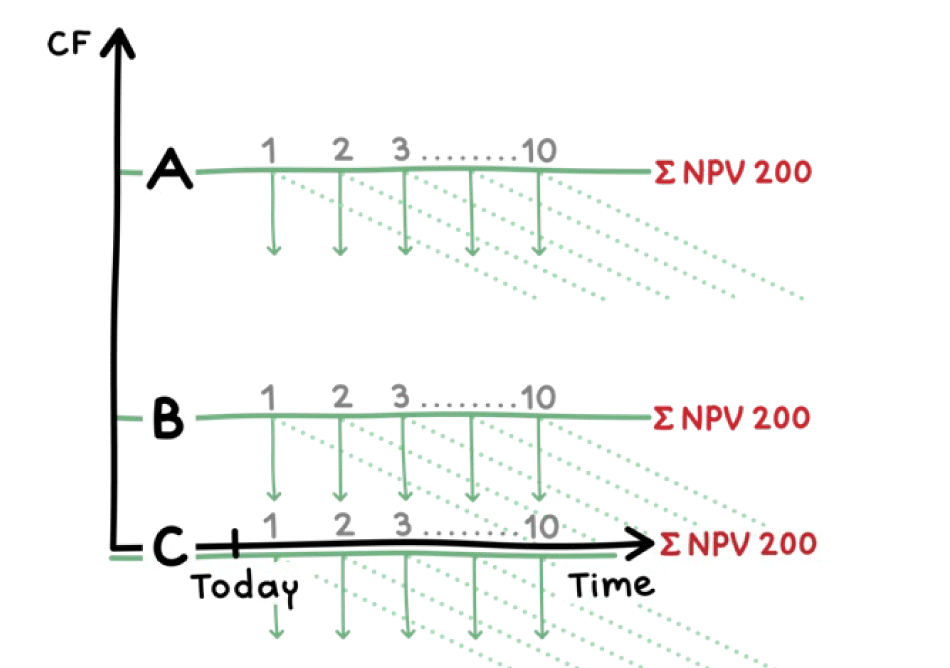

Now let’s look into the investment proposals of Quality Pulp’s two other production sites. Quality Pulp has another mill in Cleveland, Ohio. It has run for sixty years. Although the company has approved most of its required capexes, the mill simply can’t compete against the industry average. Its normalized cash flow going forward is calculated to be virtually zero. However, to maintain operations at an acceptable quality, the company must continue to allocate part of its capital budget for repairs and maintenance.

All of its requested capexes are the exact same as Baton Rouge’s: same capex amounts, same cost savings, same energy consumption improvements, same quality gains, same safety and environmental compliance costs, same productivity gains, etc. Logically, the differences between Cleveland’s normalized cash flows and its otherwise declining cash flows—that is, the deltas—for the exact same projects will be the exact same as in Baton Rouge.

Therefore, Cleveland will have the same NPV for its capex projects as Baton Rouge: $200. Now let’s add the third mill in Albuquerque, New Mexico. The company built this greenfield site just ten years ago. Its state-of-the-art technology makes the mill’s performance a leader in the industry. Again, holding all factors but one constant results in identical cash flow deltas totaling $200. When we add Albuquerque to our graph, we see:

Are All Capex Projects Created Equal?

According to today’s approach to capex, these three mills provide the same value from all of their capex projects. Their required capex needs have the exact same cash flow deltas. It doesn’t seem to matter which capexes the company approves; their NPVs are identical. Yet Cleveland generates zero cash flow for the company and Albuquerque generates most of Quality Pulp’s revenue. How can this be? And, again, how does the $200 in NPV relate to the value of the sites?

Looking at the illustration above it should be clear: Delta NPVs on capex calculations have no mathematical relation to the value of a site or business. Absolutely none whatsoever. Yes, we’ve oversimplified this example, but this only puts the problem in stark contrast. From a capital budgeting process, all three of these sites are equally good investments because they measure performance by differences in cash flows—not actual cash flow.

A More Accurate Picture

A more accurate picture of how the capex requests for these three particular facilities would show up in the standard capital allocation process would look something like this:

In a sixty-year-old mill like Cleveland, cash flows will decline much more quickly without an intervening capex than in a much younger mill like Albuquerque. That means the gap between fixing the problem vs. not (i.e., the cash flow delta) will be much wider in Cleveland than in Albuquerque. If Cleveland implements the quality enhancing capex project, the mill might save $10 in annual removed rebates and regained volumes.

That sounds impressive, but it’s only because the company is replacing a piece of equipment from the 1980s with its cutting-edge equivalent. That is, the calculation has a poor starting point; the mill was already in a poor position to begin with. If Albuquerque were to upgrade the same ten-year-old piece of equipment, the mill might only save $5 because they were in a rather good position to begin with.

Cleveland’s capex projects look as impressive as they do only because the mill is so old. Since Quality Pulp fixes a large problem every time they do something there, they close the gap from a currently poor situation to bring it up to state of the art. These types of sites create larger cash flow deltas, resulting in higher NPVs. The greater the delta, the quicker the payback. That’s how the flawed math works. But again, none of these capex investments will improve the site’s overall cash flow. At least, not at any substantial level. Value has not been created, only rescued. Cleveland’s capexes simply maintain its zero cash flow. Everything else in Cleveland (probably 99% of the asset’s replacement value) will keep aging further.

Furthermore, because Cleveland is an aging mill, it will have more capex needs than Baton Rouge and certainly more than Albuquerque. There are more liability issues, more replacements due to age and quality needs, and more safety and environmental regulations they’re behind on. The more capex needs it has, the higher the site’s sum of its capex projects’ NPVs. Going by the larger deltas and the greater number of capexes needed, Cleveland’s capex NPVs could add up to something more like $400. This, despite creating no value for Quality Pulp’s shareholders.

This amount does not in any way reflect reality, of course. Each capex request is calculated the same way, one by one in isolation…which means the same cash flow is now paying off two capex projects. You can see in the picture how the areas of the cash flow deltas overlap. Each capex project uses the same cash flows to justify its value. This is the equivalent of remortgaging a home in a second bank and then a third.

With every new capex request, the calculations ignore the “debt” from the previously requested capex projects. The same revenue stream must now pay for two capex projects, despite the fact neither increased cash flow. The payback period for the first and second projects have to be updated. If both projects had a payback period of two years and the mill’s cash flow stream had to be evenly divided between them… that would mean the first project’s “debt” would take longer than two years to pay off. The second project couldn’t be paid back in two years if half the cash went to cover the first project. With half the cash flow, it would take twice as long.

Contrast that to Albuquerque. The site is only ten years old. As such, it operates at near its life cycle’s peak performance. The gap between its post-capex cash flow vs. no-capex cash flows are fairly small. It has few safety and environmental issues. There are fewer benefits to upgrading its equipment and machines since most of the mill is still state-of-the-art. There may be a few opportunities, but these capexes can never compete with the short payback projects from Cleveland and Baton Rouge. With smaller deltas, the sum of its capex delta NPVs is much less. A star performer like Albuquerque would probably have a capex total of NPVs closer to $100.

Even though Cleveland is all but obsolete, the conventional approach to capex says it’s the best investment. Even though Albuquerque’s revenues are practically propping up the company, the conventional approach says to disregard it completely. Altogether, Quality Pulp Mfg.’s capex plans for each mill are inversely correlated with each mill’s value. The better a site performs, the less capexes it needs; the worse a site performs, the more capexes there are and, therefore, the higher the value of its capex plan. The company’s approach to capex magnifies Cleveland’s “opportunities” and minimizes Albuquerque’s needs and contributions.

Where Should the Company Invest?

According to the company’s capex process, Quality Pulp should invest the lion’s share of its capex budget in Cleveland…so that the mill can continue to generate no cash flow. Its capex process does not highlight this zero cash flow reality, however, because it’s difficult to see it when viewing capital allocation decisions project-by-project instead of as an interconnected system. In truth, the only way for a capex project to create value in Cleveland would probably be a complete rebuild of the mill or adding significant capacity, but that project would have a long payback and couldn’t compete with smaller, incremental capexes with shorter paybacks. Conversely, the company’s capex process says they should invest the least in Albuquerque…despite it being the best-performing site and generating most of the company’s cash flow.

Adding Liquidity to the Mix

So far, we have talked about one aspect of cash flow: the valuation aspect. When a company is financially challenged, a second aspect of cash flow becomes important: the liquidity aspect. Seeking to maintain or improve liquidity, during these times company executives prioritize capex projects with even shorter paybacks. A site like Cleveland looks like the go-to mill for capex projects, since this site will “rescue” the company in these rough times. Money will come back quicker if capex is spent in Cleveland, and this can be used to repay loans. A site like Albuquerque is even further neglected.

The term “payback” itself is misleading, to say the least. It is not about payback. In truth, the company will never recover its investments in Cleveland even if all assumptions come into play. All capex projects’ NPVs and short paybacks are actually realized from a post-completion review point of view, but the company will never see any money come back. How can it with a site that generates no cash flow? That value is simply gone; there is no payback in terms of money. The company will never recoup its capital invested, much less ever see Cleveland contribute much (if anything) to overall company cash flow.

The amount of capexes required to keep the site in operation exceeds the site’s overall cash flow. When we review our clients’ production sites, we almost always find at least one site projected to have virtually zero cash flow in the near future. Even then, sometimes only if the company is lucky: We’ve seen a vast number of sites where the capexes required, in combination with a declining EBITDA margin, resulted in a negative net cash flow.

This is how poor companies go bankrupt. They spend their last dime on their worst assets because that’s where they believe they will get money back the fastest. The more quickly they recoup their investment, the more quickly they can pay off debt and/or make a capital investment somewhere else. The faster payback, the faster cash flow. At least, that’s what they think.

Our example here assumes the data and calculations are 100% correct. Reality is more complicated, but that only obscures the true picture. The complexity of the real world doesn’t change the fundamental fact: Cash flow deltas direct more resources to underperforming assets and divert more resources away from high-performing ones.

The problem is that cash flow deltas are relative. A cash flow delta doesn’t share a fixed reference point with other deltas; it uses itself as its reference. The delta measures the difference between “cash flow with capex” and “cash flow without capex.” This means that an effective cash flow delta will practically always return a positive delta even for an asset with a negative cash flow. That’s how the math works.

Some companies avoid the worst decisions by additionally relying on some “gut feelings” when making decisions. In our view, this isn’t any worse than following today’s capex process…when looking at a portfolio of perhaps one or two sites. But for companies with multiple sites (certainly more than three), gut feelings cannot be relied on. The C-suite must follow a process, if for no other reason than governance and accountability.

This article is adapted from REDESIGNING CAPEX STRATEGY: A Groundbreaking Systems Approach to Sustainably Maximize Company Cash Flow by Fredrik Weissenrieder and Daniel Lindén, pages 13 – 26, published by McGraw Hill, September 2022.

This article is adapted from REDESIGNING CAPEX STRATEGY: A Groundbreaking Systems Approach to Sustainably Maximize Company Cash Flow by Fredrik Weissenrieder and Daniel Lindén, pages 13 – 26, published by McGraw Hill, September 2022.

About the Authors

Fredrik Weissenrieder, co-author of REDESIGNING CAPEX STRATEGY, is the founder and CEO of Weissenrieder & Co., a global capex strategy consultancy and tech company, based in Sweden. In 1994, he developed a fundamentally different approach to industrial capital allocation and is today a recognized global leader on the topic. To learn more, visit: https://weissr.com/

Fredrik Weissenrieder, co-author of REDESIGNING CAPEX STRATEGY, is the founder and CEO of Weissenrieder & Co., a global capex strategy consultancy and tech company, based in Sweden. In 1994, he developed a fundamentally different approach to industrial capital allocation and is today a recognized global leader on the topic. To learn more, visit: https://weissr.com/

Daniel Lindén, co-author of REDESIGNING CAPEX STRATEGY, is the COO of Weissenrieder & Co. Since 1999 he has helped refine Weissenrider’s groundbreaking approach to industrial capital allocation. He oversees the company’s consulting teams as well as the team developing the consultancy’s SaaS service Weissr® Capex, the world’s first application integrating capex budgeting, management, and strategy. To learn more, visit: https://weissr.com.

Daniel Lindén, co-author of REDESIGNING CAPEX STRATEGY, is the COO of Weissenrieder & Co. Since 1999 he has helped refine Weissenrider’s groundbreaking approach to industrial capital allocation. He oversees the company’s consulting teams as well as the team developing the consultancy’s SaaS service Weissr® Capex, the world’s first application integrating capex budgeting, management, and strategy. To learn more, visit: https://weissr.com.