Are you planning to invest in Ethereum? If yes, then you must know what the exact potential of Ethereum is.

Ethereum is not just a cryptocurrency; instead, it is more than that. It is full-fledged technology, which is capable of changing the business world. Moreover, like any other technology, it has its benefits and challenges.

Therefore, in this blog, you will find some of the benefits and challenges of Ethereum and use cases that can prove why Ethereum is better than other technologies.

Let’s start with stats first!

Ethereum development company statistics say, 96% of the business owners are not aware of Ethereum. Besides, according to Etherscan, 49% of all the transactions with the Ether cryptocurrency are executed within smart contracts.

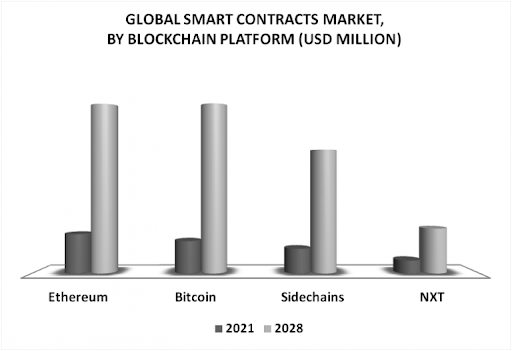

Ethereum accounted for a 36.28% market share in 2020, valued at USD 52 million and projected to grow 23%.

Ether is the token of the Ethereum network, which is focused on disrupting contract law. – Cameron Winklevoss

Therefore, if you are still unsure about this technology, then keep reading.

Top 9 Benefits of Ethereum Smart Contracts Development for Businesses

With the recent surge in cryptocurrency valuation, many businesses are now exploring Ethereum smart contracts development. If you are also planning your enterprise blockchain application, here is an insight into how this technology can help to grow your business exponentially.

1. Reduction in operational costs of an organization:

Companies can reduce their operational cost with ethereum smart contracts. It is the most efficient way to automate your transactions. The manual processing of data takes up a lot of time and requires human effort, increasing costs.

Automation helps to reduce these costs. For example, insurance companies have substantial operational expenses. A majority of their work is on paper-based documentation. As a result, there is a high likelihood of errors occurring during this process due to human error or misinterpretation.

Ethereum smart contracts will ensure that all the business logic is automated, thereby reducing errors to zero. Hence, it reduces down processing time as well as improves efficiency & accuracy.

2. Better transparency of transactions within the business ecosystem:

When you are developing Ethereum smart contracts for business purposes, it is essential to understand that the transactions will be visible to all users on the blockchain. This means that intermediaries like auditors and accountants can quickly analyze your data whenever required.

Any updates made by you can also be viewed by anyone who has access to this information. Moreover, any new entries added by employees (transactions) would need the approval of managers.

3. Improved identity management system:

With blockchain technology, it is possible to manage users within your organization. You can easily create & maintain individual identities on the Ethereum network for employees assigned various tasks. This means you can check throughout their tenure in the company.

For example, you can use this system to restrict access to sensitive parts of your organization (like financial reports). Any requests made by employees will be authorized through smart contracts.

Hence, everyone’s identity is quickly & conveniently verified & mapped to the tasks they perform. This way, you can control access to critical information within your company.

4. Better supply chain management:

Vitalik Buterin, the inventor of Ethereum, says it is a platform to “build many applications that have not been invented yet.”

Hence, this means that there are limitless possibilities for future business ventures. One such application that Ethereum can offer is supply chain management. You can connect suppliers, manufacturers, and distributors with a robust backend database in a completely decentralized & transparent way.

It will be easier to monitor inventory at all times, along with complete transparency about where physical products come from and where they are going. Hence, it can potentially fix the problem of fake products and stolen merchandise.

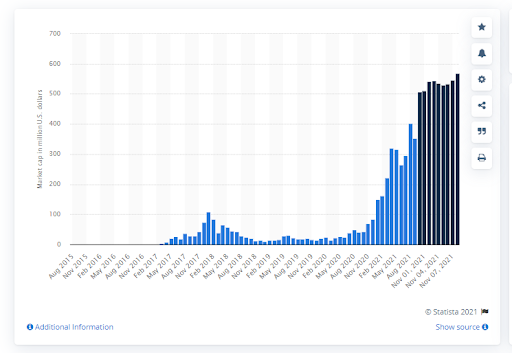

Over 250 billion U.S. dollars were invested in Ethereum in April 2021, reaching new highs. (Statista)

5. Reduction in fraud cases and risk within the business ecosystem:

Frauds in business transactions are common. Moreover, it is difficult to track down the perpetrators due to a lack of transparency about where money has been exchanged and where it finally ends up. But with ethereum smart contracts, you can easily monitor all transactions that take place in your business ecosystem.

You can easily create a smart contract between two parties that involve sharing of funds, whereby you can take care of & remember the following points:

- The cryptography of sensitive data

- Maintaining a complete history of transactions so that there is complete transparency

- Eliminating the need for intermediaries like auditors and accountants

6. Improved customer satisfaction and loyalty programs to increase retention rates:

Today, whether it’s small or big-budget, companies compete to operate to retain their customers. With Ethereum smart contracts, you can take the game to a whole new level.

You can ask an Ethereum development company to develop loyalty programs by implementing them on an Ethereum based platform like AdChain. It will ensure that you know all about your customers. The points earned by them through various loyalty programs can be converted into tokens that can be redeemed at any point in time.

Moreover, it is not limited to just one business platform, and users have the option of using these tokens across different platforms as well.

7. Faster and more efficient business services:

One of the primary reasons for companies to go for blockchain technology is to process business transactions faster. Moreover, this helps them get an edge over their competition since blockchain allows instant settlement of assets between two parties.

Hence, you can offer your customers a quick & easy way to complete any business transaction with minimal errors. You can also use Ethereum to provide more business services on one single platform!

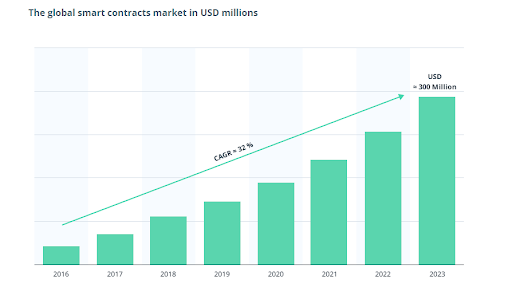

In a recent report from Market Research Future, the global smart contracts market is forecast to reach $300 million by the end of 2023, with a 32% CAGR.

8. Better monitoring of end-users within the business ecosystem:

According to Accenture, only 8% of companies are satisfied with the data they have on their end-users. The rest, 92%, want more information about end-users which can help them improve business operations.

Ethereum based platforms offer a whole new way of looking at things since you can establish relationships between end-users and businesses in an entirely different way!

All transactions & interactions take place through smart contracts, ensuring that no information is leaked about these users. User identities are entirely anonymous, but their behavior is recorded for future analysis.

Additionally, Statista figures estimate that the cryptocurrency Ethereum will be processed one million times daily in 2021.

9. Better analysis of data from different channels through centralization:

Businesses need to understand how their products and services are performing in the market. The traditional approach to understanding this behavior involves hiring an army of people to conduct various surveys and other forms of analysis. Further, this is a resource-intensive process that requires time and planning before any kind of data can be collected.

But with Ethereum, you can get almost real-time information from all your channels & customers through one platform! You will have complete centralized access to all your data which can help you make more intelligent business decisions faster.

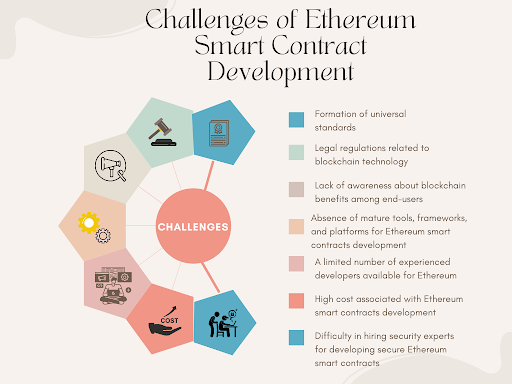

7 Challenges of Ethereum Smart Contract Development

As interest in smart contracts grows, so does the demand for developers who know how to create them. But there are some critical challenges associated with this type of development.

Knowing about them can help you better prepare yourself when you start your Ethereum smart contracts development projects in the future. Besides, here are seven of the most common challenges that smart contracts developers will face shortly.

Challenge #1: Formation of universal standards at the business level

It is essential to understand that smart contract technology is still in its infancy. Even now, there are no universal standards for what it means to write a “good” or even an “acceptable” smart contract.

One group of developers may see the implementation of certain functions as completely unacceptable, while other developers may find those same functions perfectly acceptable. This leads to potential problems when different teams develop ideas about “reasonable” behavior within the blockchain platform.

Challenge #2: Legal regulations related to blockchain technology are still evolving in different countries globally

With the growing interest in smart contracts, we can probably expect to see more and more governments trying their best. They are trying to offer clear and valuable legal guidelines and restrictions. But, still, regulatory uncertainty is one of the biggest barriers to Blockchain adoption.

At the moment, there is no legal standard for blockchain technology in the world. It is challenging to determine how a court might deal with a contract dispute involving blockchain-based development if the two parties live in different countries, the case will run smoothly.

As you know, these types of issues can end up taking years or decades to resolve through traditional legal channels.

Challenge #3: Lack of awareness about blockchain benefits among end-users within an organization

Unless the end-user understands why blockchain technology is beneficial, they are unlikely to support its development or use. According to a Blockchain development company survey, almost one-third of companies said their employees lack a full understanding of the value and significance of blockchain technology.

Besides, most of these companies (64%) said their employees lack competence for an operating understanding of blockchain technology. Only 34% of respondents reported that their employees understood this technology’s basic value and significance.

Challenge #4: Absence of mature tools, frameworks, and platforms for Ethereum smart contracts development

The lack of mature development tools, frameworks, and platforms for Ethereum is one of the developers’ biggest obstacles in building blockchain-based applications. We’ve already seen several startups release smart contract platforms like BlockApps STRATO and Parity.

However, these platforms are still far from complete. Furthermore, developers will also need to consider that smart contracts are still a relatively new technology. So expect to see some significant changes within this space in the coming years.

Challenge #5: Limited number of experienced developers available for Ethereum smart contract development projects

The overall number of experienced Ethereum smart contract developers is small, as it is with any new and emerging technology. According to a developer survey, only about one-third of developers said they had previous experience working with cryptocurrencies.

Besides, there’s no guarantee that enough people can work on Ethereum-related initiatives among these developers. Even if you do find a few developers with blockchain experience, they may not be able to work with your organisation’s preferred programming language because Ethereum smart contracts are written in Solidity.

Challenge #6: High cost associated with Ethereum smart contracts development

Ethereum smart contracts are not entirely free to develop. While some essential development tools are available for free, the associated gas costs can add up quickly.

For example, suppose you have a team of Ethereum developers working on Ethereum-based applications that require specific types of data from outside sources or blockchain-based APIs. In that case, the associated network fees will end up being quite costly.

Challenge #7: Difficulty in hiring security experts for developing secure Ethereum smart contracts

Since Ethereum-based smart contracts are decentralised and immutable, you’ll also need to keep in mind that these types of applications will be tough to upgrade once they’re deployed.

This means that developers must spend a significant amount of time analysing the initial requirements and designing secure smart contract components from the start. Just because you can quickly build a blockchain-based application doesn’t mean that it will automatically be safe.

While several high-quality security plugins are available for Ethereum development, not every company will have the resources or funds to hire a dedicated team of security professionals.

5 Best Use Cases of Ethereum Smart Contracts

One of the biggest drivers of Ethereum’s growth over the past few years has been the emergence of smart contracts. However, it can still be challenging to understand why they matter, especially in the real world.

We’ll discuss 5 of the best use cases of Ethereum smart contracts in practice right now, from managing virtual property to running online advertising networks to processing legal documents and more.

1. Banking & Financial Services Contracts

With an Ethereum contract, banks can code their services as transactional protocols and deploy them as decentralized applications (DApps). International payments and lending can be made efficiently without a middleman or counterparty risk.

Many banks are already exploring these possibilities by building blockchain labs and developing PoCs using smart contracts. For example, last year, CBA (Commonwealth Bank Australia) tested a smart contract with IBM on a private version of Hyperledger Fabric built by IBM and Digital Asset.

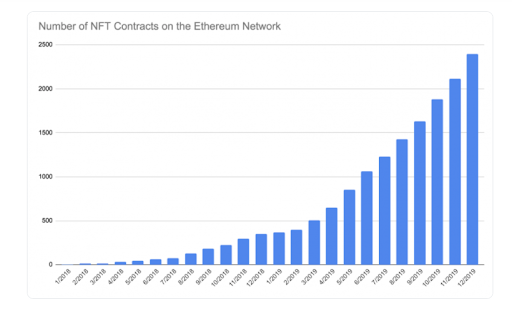

2. Non-Fungible Tokens on Ethereum

ERC-721 is an Ethereum smart contract standard for non-fungible tokens. Each token is one-of-a-kind, similar to a unique snowflake or thumbprint. Tickets are often used in gaming scenarios, where each token stands for something different, like a specific weapon or armor piece that’s difficult to trade with other players.

Additionally, because each token is one of a kind, it can be sold on virtual marketplaces for money.

Did you know? The number of mainnet ERC721 contracts has increased exponentially in the last year as new developers enter the space, reaching 1,000s.

3. Escrow services on Ethereum network

Escrow services enable secure payments on several platforms. The very nature of a smart contract ensures that funds are only transferred when certain conditions are met. So if you want to buy some item from an e-commerce website, you can make a payment using an escrow service.

If you’re buying concert tickets, that money will only be released to the seller once you arrive at your seat or redeem them for merchandise.

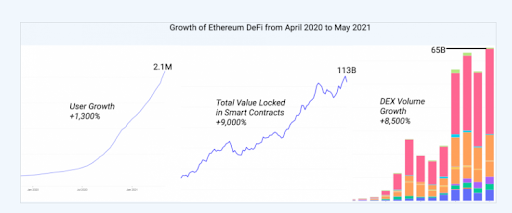

4. Decentralized finance (DeFi) growth on Ethereum network

Decentralized finance (DeFi) is an ultimate relatively new concept, even though it’s been around for nearly four years on public blockchain networks like Ethereum. It has become trendy in 2019 thanks to growth drivers such as low-interest rates.

And improvements made on user experience thanks to software developed by non-profits and startups with funding from venture capital firms.

According to Wang’s report, total value locked (TVL) increased 64 times to $52 billion in Q1 2021 decentralized finance (DeFi) data compared to Q1 2020 stats. Since then, the total amount of DeFi has risen by another $20 billion.

5. IoT device management using Ethereum Smart Contracts

Ether is a rising star in smart contracts. The use cases that it offers for Internet of Things devices management are worth thinking about. It’s been used as a backbone for several blockchain-based IoT systems, including Slock.it and RSK Labs. With Ether, you can manage your IoT devices from an Ethereum wallet.

Most importantly, there is no need to install third-party software or face security issues with your system’s security breaches via online applications/servers.

Wrapping Up!

To conclude, Ethereum is a complex technology with many applications in the real world. To help you understand more about its benefits, we have showcased some of its best use cases.

It’s been an excellent year for Ethereum, and its future remains bright. If you are interested in Ethereum and thinking about Ethereum Smart Contracts Development, then hire a smart contract development company in India like PixelCrayons.

Such a company has the expertise to deliver top-notch ethereum smart contracts development services. Indeed, we hope this article helps you understand the basics of Ethereum and its applications better.

FAQs

Q1: What are smart contracts and their benefits?

A1: As defined, smart contracts are self-executing contracts in which the terms of the agreement between buyer and seller are directly written into code lines. There exists a distributed, incorruptible blockchain network that contains the code and the agreements.

Talking about the benefits, they are numerous. They include:

- Security- Smart contracts are safer than traditional contracts, where all parties involved have different parts of the contract. Smart contracts enforce and facilitate the terms of an agreement automatically.

- No need for a third-party or intermediary- In addition to that, smart contracts eliminate the need for intermediaries as their rules are applied by software code everyone can see. Moreover, this allows transactions to be carried out in an efficient and trustless environment.

- Transparency- All information is encrypted and hashed using cryptography because it is a public ledger. Therefore there’s no need to rely on someone else’s version of the truth or data that can be manipulated later.

- Trust- The whole process is automated and decentralized, so there’s no need to trust the other party in the transaction.

- Cost- Finally, smart contracts help businesses save on transaction costs since they significantly reduce the number of intermediaries needed for an agreement to take place between two parties.

Q2: What are ethereum smart contracts used for?

A2: Ethereum is a blockchain platform that facilitates the creation of smart contracts. These applications run on Ethereum’s blockchain with all the rules and regulations built into the given application.

Ethereum smart contracts are used for multiple purposes. Here are some examples:

- Token Creation- You can create tokens for the Ethereum blockchain with smart contracts. They are used to issue and distribute the tokens between users who’ve participated in an ICO, for example.

- Crowdfunding- Another use case is crowdfunding platforms. These platforms allow individuals to invest in startups’ products with cryptocurrency through token sales or ICOs.

- Managing IoT devices- Ethereum provides you with a platform for managing your IoT devices. For instance, it allows communication between sensor data to produce an automated machine responding to specific phenomena or events.

Q3: How do I create a smart contract in Ethereum?

A3: To develop an Ethereum smart contract, you need to hire Ethereum smart contract developers. Then, they must be able to write code for the application.

To create a smart contract, you need to follow these steps:

- Define business rules- This is essential since it will define the specific terms necessary for every transaction. For instance, if someone is willing to send money to another person or group of people, that needs to be written into the business rules of the smart contract.

- Code- The developer will then add code to enable the functionality of the application. In some cases, you may need separate modules depending on how your contract is going to work.

- Decentralized- For you to make the blockchain smart contract development services useful, it has to be decentralized. As such, it needs its cryptocurrency so that transactions can take place between two anonymous parties without any intermediary.

- Deployment- Finally, you just need to release the contract into the Ethereum network. You can choose a specific blockchain where it will reside or go for a public one so that anyone connected to the network can use it.

Q4: How do I hire an ethereum smart contract developer?

A4: There are many ways to find an Ethereum smart contract developer, but the best way is to go for top development firms with a history of working on blockchain projects.

They should have a good understanding of cryptography and be able to work on distributed and decentralized applications. Plus, they should also have experience in writing smart contracts.

Disclaimer: This article contains sponsored marketing content. It is intended for promotional purposes and should not be considered as an endorsement or recommendation by our website. Readers are encouraged to conduct their own research and exercise their own judgment before making any decisions based on the information provided in this article.