Home loans remain the primary financing channels for property purchases. But loanable amounts are capped, and you might need more than the available amount to buy your dream home. The solution? A jumbo loan.

Some lenders offer jumbo loans for properties with higher price tags. However, the guidelines and requirements, including a borrower’s credit score, are often more stringent and higher than conforming loans.

So what’s the difference between the two, and why is your credit score important when applying for a jumbo loan? Let’s find out.

Conforming Loan Vs. Jumbo Loan: What’s The Difference

The primary difference between the two is that jumbo loans aren’t guaranteed by government-backed lenders, except for the Veteran Affairs (VA) jumbo loan. This means it’s riskier for financing agencies if the borrower defaults or can no longer pay.

-

Higher Loan Limits

While conforming loan limits vary from county to county, recent figures peg the ballpark figure at USD$726,200. If you need to borrow more than that, a jumbo loan might be a smart idea.

In some areas, borrowers can access as high as USD$5 million. However, the conditions, limits, and terms for such a financing scheme vary from lender to lender, alongside the property’s location. If you’re getting Florida jumbo loans, it’s best to shop around and compare.

-

Heftier Downpayments

As such, jumbo loans require larger downpayments of around 20%, a few times more than the 3% for conforming loans.

-

Potentially Larger Costs And Interests

Similarly, jumbo loans often have higher interest and closing costs than traditional mortgages. Because of higher down payment requirements, a borrower may skip paying for private mortgage insurance (PMI), calculated based on property value and lender’s guidelines.

If you need to purchase a costlier home, whether to live in or as an investment, and have a stable income, a jumbo loan might be a good option.

Jumbo Loan Requirements

Because of the risks involved, not all banks offer jumbo loans. If your bank doesn’t offer this type of mortgage, you can always look for other private lenders.

As with other conventional loans, it’s important that you know what you’re getting into.

Here’s what to expect if you’re getting a jumbo loan:

-

Stricter Guidelines And Documentation Requirements

Jumbo loan lenders typically ask for income and other documents to ensure a borrower’s financial capacity and stability. These may include personal and business documents like bank statements, property titles, income slips, tax returns, and proof of investment, to name a few.

-

Cash Reserves And Assets

Unlike conforming loans, jumbo loan borrowers will be asked to submit financial records indicating they can cover at least one year’s mortgage. They should have cash reserves on top of a stable income as an added guarantee that they can avoid foreclosure even in times of financial emergencies.

-

Higher Income Qualifications

A consistent income stream, whether from a high-paying salary or a high-earning business or investment, increases your chances of getting approved. By showing a stable income history, lenders will see you as a low-risk borrower, becoming more confident in your repayment capacity.

-

A Low Debt-To-Income Ratio

Lenders will look at your debt-to-income ratio (DTI), which represents the portion of your income meant for debt payments. Jumbo loan financiers have different caps. However, a good rule of thumb is to keep your DTI as low as possible to achieve a better outcome.

-

A Credit Score Of Over 700

As you may expect, lenders require borrowers to have an impeccable credit score. If 620 is acceptable for most conforming loans, jumbo loans generally require a rating of at least 700 to qualify. You should study and build your credit score first before getting one.

Why You Need To Boost Your Credit Score

Lenders are quite restrictive in approving jumbo loans because it’s a high-risk loan product. In 2022, for example, the rejection rate for jumbo loans was almost 12%, per Inside Mortgage Finance—representing a slight increase compared to 11.2% a year before.

Of the requirements above, your credit score is the one where you have the most control. Your credit history provides information to your potential lenders about your character, and the higher the rating you have, the better. Besides increasing your chances of getting approved, a higher credit score could get you better terms and lower interest rates.

How To Build A Good Credit Score

To ensure you qualify for a jumbo loan and enjoy certain perks the lender offers, you should build your assets, income, and credit score. Here are some tips:

1. Analyze Your Credit Report

Ask for an annual credit report for free from any of the major credit reporting companies. Doing so helps you understand where your credit strengths and weaknesses lie. In doing so, you can boost your credit score to your advantage.

- What affects your credit score?

Several factors influence your credit score. First, you must possess ample credit history displaying a low credit card balance, on-time loan or rental payments, and minimal inquiries for new credit from lenders. Conversely, high amounts of unpaid loans, missed payments, and debt collection lawsuits can dramatically pull down your rating.

2. Give Your Credit History A Boost

You’ll most likely get rejected for a jumbo mortgage if you have a thin file. Look for ways to boost it by exploring programs offered by credit bureaus. Such schemes collect payment data that typically does not include your credit history. These include bills payments, rentals, and banking history.

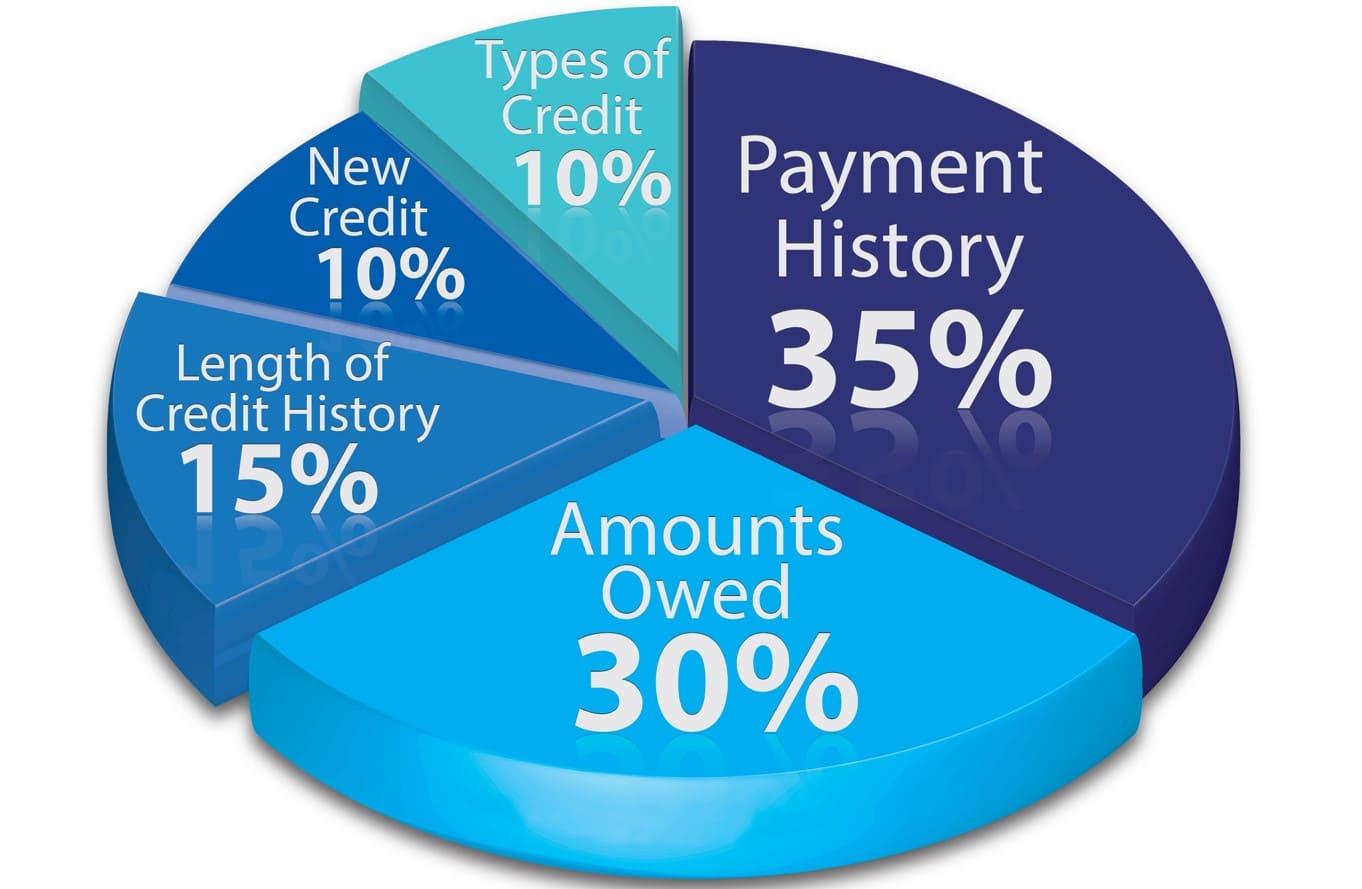

Ask the organizations offering such service to determine whether the information can affect your Fair Isaac Corporation (FICO) score. To the uninitiated, most lenders check a borrower’s FICO score to determine their creditworthiness. Scores are determined using the following elements: payment history, current level of indebtedness, credit history, new credit inquiries and accounts, and the borrower’s credit mix.

3. Manage Credit Payments Strategically

Increase your creditworthiness by paying your debts on time. Late payments could earn you penalty fees and hurt your credit score. You can set alarms for credit dues or automatically arrange payment deductions from your account.

If you’ve charged your bills and purchases to your credit card, make sure to pay the full amount or exceed the total monthly bill to avoid paying high interest rates. Additionally, you may consider consolidating your debt to lower your cumulative interest fee. Just ensure you’re diligent with your payments.

4. Maintain A Low Credit Utilization Rate

Credit utilization rate refers to the percentage of the amount you’ve borrowed with your total credit limit. Keeping a low utilization rate means you’re managing your current debt and finances well.

As mentioned, it pays credit card and loan dues in full monthly. Lower utilization ratios are always better, so keep yours below 30% to have a favorable impact on your credit score. Consider keeping some of your credit cards active even while you’re not using them now. They help increase your available credit and lower your utilization ratio.

5. Hold Off On New Credit Applications

Don’t apply for a new loan, credit card, or other loan type while your jumbo loan application is processed. Credit history requests concerning a loan or credit applications will likely pull your credit score down, giving lenders the impression that you’re in financial stress and, therefore, a high-risk borrower.

Final Thoughts

With heftier amounts involved and no strong guarantees of repayment, extending a jumbo mortgage is riskier than conforming loans. As such, lenders would like to reduce these uncertainties by financing exclusively for qualified borrowers. This makes it more challenging to get approved for a jumbo loan.

A high credit score and ample credit history are two primary tools lenders use to assess your borrower risk level and credit management capacities. By showing you excel in both aspects, you’re in the right direction toward purchasing your high-value property.

Disclaimer: This article contains sponsored marketing content. It is intended for promotional purposes and should not be considered as an endorsement or recommendation by our website. Readers are encouraged to conduct their own research and exercise their own judgment before making any decisions based on the information provided in this article.

: What Foreign Investors Need to Know")