By Gregory DeYong, Hubert Pun and Carol Lucy

Copycats are every industry’s nightmare. Consumers are becoming more budget-conscious and many start to favour generic products than brand names. Major companies should implement rational measures to guarantee profit against product-stealing and low-cost copycats. Consumer behaviour should also be taken into consideration to retain their old customers and acquire new ones.

One is an utter luxury; the other is a necessity of life. Although the fashion and pharmaceutical industries are worlds apart in terms of products, both face a very similar challenge – copycats who sense an opportunity to produce lower-cost versions of the original product. In the case of pharmaceuticals, the production of generic versions of popular medications is a common event once the patent protection of the developer expires. In 2016, generic pharmaceuticals accounted for over $100 billion of the total spending on medicines in the United States.1 For fashion designers, the burgeoning fast-fashion industry excels at taking hot new designs and quickly making them available to the masses. In either case, a firm that spent its time and resources to develop a unique product sees its hard-won advantage eliminated by a copycat. At the same time, consumers are faced with a choice – purchase the expensive original or take a chance on the low-cost version.

Whether we view copycats as predatory imitators who steal designs for their own profit or as a type of Robin Hood, bringing hyper-expensive products into reach for the masses, the question of how a designer of new, innovative products should react to the threat of copycats is still valid. Despite extensive lamentation by fashion designers, enforcing copyright claims against fast-fashion retailers remains both difficult and rare.2 Similarly, pharmaceutical manufacturers face not only patent expiration, but also significant risk of public backlash if they are perceived as limiting supplies to consumers.

A prime example is the recent outcry against Mylan over its pricing of the emergency allergy treatment, EpiPen. Facing imminent FDA approval of a generic version of the EpiPen (from generic drug titan Teva Pharmaceutical Industries, Ltd.), Mylan shocked consumers and regulators by dramatically raising prices of its EpiPen product (by over 400%). This led to accusations of price gouging, particularly when FDA’s approval of Teva’s product was delayed, leaving Mylan with a virtual monopoly. Many observers offered explanations for the price increase, ranging from price gouging to condemnation of the pharmaceutical patent process itself. However, it is also possible that Mylan’s move was a rational reaction to an impending generic version of the EpiPen. In another situation involving Teva, Valeant Pharmaceuticals International dramatically raised the price of its Syprine medication (from $652 to $21,267) in 2015 as its patent protection neared an end. According to the New York Times, “When Teva Pharmaceuticals announced recently that it would begin selling a copycat version of Syprine – an expensive drug invented in the 1960s – the news seemed like a welcome development for people taking old drugs that have skyrocketed in price.”5

However, their hopes were dashed when Teva priced the product at $18,375 per 100 pills, significant savings, but a huge increase over the price charged for the brand name drug just five years earlier.

With the advent of widespread generic pharmaceuticals, many other examples of major pharmaceutical companies attempting to protect their valuable brands and patents can be identified. In 2007, AstraZeneca sued a group of seven generic drug makers over alleged infringements on the AstraZeneca patent on the cholesterol drug, Crestor ®.6 AstraZeneca has been fighting an ongoing legal battle against generic versions of the drug, recently losing an effort to extend its market exclusivity by arguing that Crestor® was entitled to consideration as an “orphan drug” as it can be used to treat a rare high cholesterol condition in children.7 Similarly, in 2013, a U.S. biotech firm, AbbVie, sued an Indian firm, Dr. Reddy’s Laboratories (DRL) over the latter’s application to produce a generic version of the AbbVie drug, Zemplar. In 2016, the British pharmaceutical firm Indivior faced allegations that it had attempted to reestablish a monopoly on suboxone (used to treat heroin addicts) by developing a new delivery mechanism for the medication. Indivior then claimed this should entitle it to renewed patent protection from generics, which it had lost in 2009 as its exclusive rights to the tablet form of suboxone expired. One issue the copycat firms faced in this case was that the customers had switched to the new form of suboxone (a dissolvable strip) and were reluctant to return to the tablet form.

Similar accusations are often bandied about in the fashion world. Major fashion designers are excoriated for their high prices, leading many to portray fast-fashion copycats as performing a valuable service by bringing fashion designs to budget-conscious consumers. These copycats have developed the fast-fashion market as firms such as Forever21 and Zara have become specialists at avoiding litigation while delivering products that closely resemble high-end fashion goods offered by firms such as Burberry. Of course, fashion designers complain about seeing their creativity stolen by unscrupulous retailers who are only out to make a fast profit. Could it be that the apparent tension in the fashion industry is again just a rational reaction by firms?

[ms-protect-content id=”9932″]

• In 2000, an association of generic pharmaceutical manufacturers (Generic Pharmaceutical Association – GphA) was formed to advocate for the manufacturers of generic pharmaceuticals

• Over 90% of United States prescriptions are for generic versions of medications3

• Dozens of pharmaceuticals currently protected by patents will lose that status in the next few years4

• Patent protection may be extended for pharmaceuticals with changes in indication, strength, dosage form or if the medication is found to be useful for pediatric applications4

• “The real deal won’t be sold in stores for half a year, but Forever21 can have a much more wallet-friendly copycat version on the shelves in three weeks”9

The Problem

The main essence of a copycat is taking advantage of the investment of another firm. Rather than building its own market, the copycat attempts to capture a portion of an existing market developed by the original firm. Before the copycat’s product is available, the original manufacturer may face no actual competition, but savvy consumers can foresee the possibility of a copycat in the future. Some consumers may be willing to wait until a later time when both versions of the product are available in anticipation of a lower price for the original product (to better compete with the copycat) or the entry of an acceptable copycat with a budget-friendly price.

The copycat’s decision process is relatively simple – enter the market if it is possible to do so profitably. At times, the copycat may need to consider that the manufacturer will take defensive steps such as limiting marketing expenditures (to avoid building a market only to have it stolen by the copycat) or lowering prices to make the copycat’s niche unprofitable, but in many cases the manufacturer is unwilling to take such drastic steps.

For the manufacturer, the decision process must answer three questions:

1. How good should the product be?

2. How much to invest in advertising and other activities to increase the number of consumers who will want the product?

3. What price to charge for the product (before and after the copycat enters the market)?

As in most situations, these decisions must be made in an uncertain world and each decision has an impact on all the others. For example, investing to build a large market may allow (or even require) the manufacturer to charge a higher price. On the other hand, charging a higher price in a large market makes that market attractive to the copycats, who can more easily charge a lower price to capture the budget-conscious consumers.

This situation has been modelled,10 and in many cases, what seems like an irrational or opportunistic decision by the manufacturer may actually be the best course of action. Although manufacturers bemoan the low quality of copycats, it is generally undesirable for a manufacturer to compete head-to-head with a copycat who offers a product of similar quality at a comparable price. In the case of fashion clothing, this can lead the designer to improve the quality and, in some cases, raise the price of goods when a copycat is imminent. Similarly, it is plausible that the best response for Mylan (or any pharmaceutical manufacturer) to the impending approval of a generic version of a profitable product is to raise prices and essentially abandon the low-end of the market while establishing a quality differentiation with the low-cost competitor. In fact, a recent study of prescription drug prices11 found that a group of twenty-five leading pharmaceuticals had shown a dramatic increase in price for the brand name product (7-9% per year) but that overall prices for these drugs had dropped significantly because of the introduction of low-cost generic versions, which quickly captured most of the market. The same study found that average daily cost of treatment fell by an average of 27.5% after a generic version had been available for twelve months.

• How much time, effort and money to spend on product development

• How much to spend on advertising and other market-building activities

• Product pricing – before and after the potential entry of a copycat

Competitive Scenario

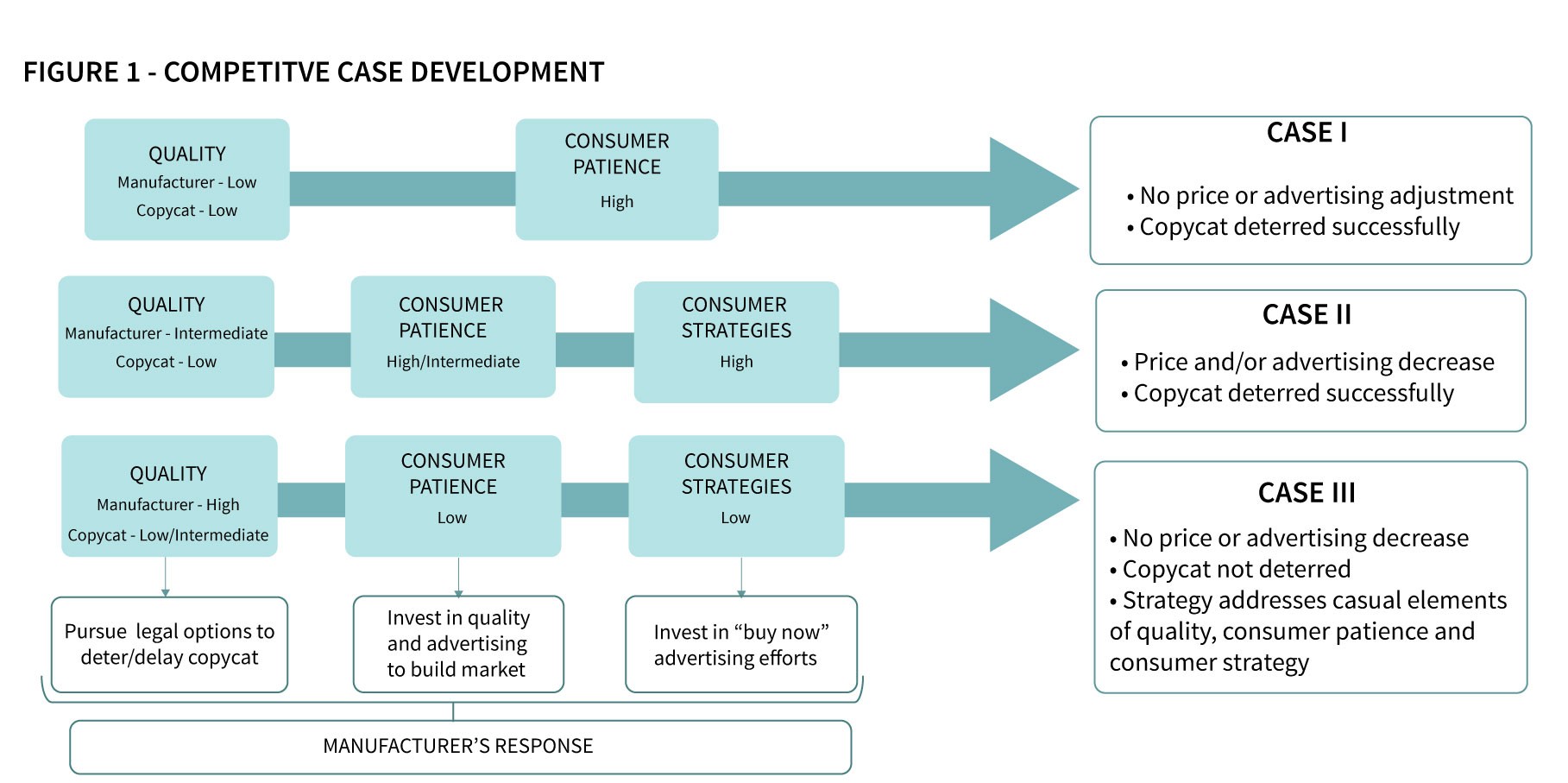

The copycat threat is not unique to fashion goods, pharmaceuticals, or any other industry. We can apply the same analysis to any situation where copycatting takes place. In a more general setting, imagine a manufacturer of a unique product facing the future threat of a copycat. The manufacturer (and consumers) can foresee the possibility of a lower-cost competitor entering the market at some time in the future. The manufacturer, therefore, must determine product characteristics (in particular, quality) as well as advertising and pricing of the product before, and potentially after the market entrance of the copycat. The copycat, in turn, must decide how to price and position the low-cost version of the product. Our research has shown that, for the manufacturer, three possible outcomes are possible. In the best case, the threat of retaliation by the manufacturer (lowering prices, decreasing advertising) is sufficient to deter the copycat from entering the market. In this case, the manufacturer need not make any actual changes to product, pricing, or advertising. We will refer to this as case I – credible threat. Unfortunately, at times, the manufacturer is not able to deter the copycat with threats alone. Instead, in this situation (case II – actual threat), the manufacturer must actually absorb the negative consequences of strategy adjustments (lower prices, reduced advertising, and/or reductions in quality) to reap the benefits of keeping the copycat out of the market. In the final possibility (case III – ineffective threat), even adjustments to strategy are insufficient to deter the copycat. Instead, the manufacturer must adapt to sharing the market with a new competitor, particularly if legal recourse is unavailable. Specific circumstances where these three cases arise include the following:

• When the similarity between the original and copycat product is high, the copycat will face intense price competition from the manufacturer (a price war as each undercuts the other repeatedly). Since this will ultimately lead to an unprofitable situation for the copycat, the manufacturer does not have to make any adjustment to advertising or prices. The threat of a price war is sufficient to deter the copycat in this case I situation

• When the manufacturer’s product is more desirable than the copycat, but not dramatically so, it is often profitable for the manufacturer to adjust advertising (lower) and pricing (lower) to deter the copycat from entering the market. The copycat can be discouraged from even entering the market, as discussed in a case II outcome.

• When the differences between the two products are highly significant (for instance, a high-end fashion label compared to a discount retailer), the copycat is unlikely to face price competition, as it is not profitable for the manufacturer to lower prices to a level that will deter the copycat from entering the market. Therefore, the copycat can claim the low-end niche as its own with little interference (economically) from the manufacturer. The manufacturer is forced to rely on legal means (such as copyright enforcement) to combat the copycat. This is a case III outcome.

• Case I – the mere threat of retaliation (in the form of lower prices and reduced advertising) by the manufacturer deters the copycat from entering the market.

• Case II – an actual adjustment in prices and/or advertising by the manufacturer deters the copycat from entering the market.

• Case III – the manufacturer cannot profitably make a sufficient adjustment to prices and/or advertising to deter the counterfeiter. The manufacturer abandons the low-quality portion of the market to the copycat.

Interestingly, in the case II situation, a higher degree of similarity can lead to higher profits for the manufacturer because smaller reductions in price will be needed to deter the copycat. This allows the manufacturer to charge a higher price while still keeping the market to itself. However, a manufacturer who develops a superior product may be a victim of its own success. The copycat can claim the low-cost end of the market from a manufacturer who is unwilling or unable to lower prices on its high-value product.

• To preserve the advantage of reaching the market first, Nike employs security guards, cameras and a secondary, outer wall to prevent samples or blueprints of future products from being stolen12

• Luxury fashion brands such as Burberry and Gucci are investing in supply chain strategies to shorten time-to-market13

• Pharmaceutical firms can extend the patent protection for drugs by developing new delivery mechanisms or having the drug named as an “orphan drug” to gain special patent extensions

The willingness of consumers to wait for the copycat product has essentially the same effect as a shorter (or longer) delay before the copycat enters the market. When consumers are willing to wait for the eventual copycat, the manufacturer may be able to deter the copycat with real (or threatened) price decreases in the future (case I or case II). A manufacturer that cannot credibly make this threat will face the eventual entry of the copycat (case III).

Competitive Phases

Another key aspect of the manufacturer/copycat competitive environment is the length of time needed for the copycat to enter the market. Prior to the copycat’s entry, the manufacturer can be seen as having a monopoly. The advantages of reaching the market well before copycats are demonstrated by the lengths that firms (e.g. Nike) will go to protect their designs12 and the investments they will make to improve the responsiveness of their supply chains (e.g. Burberry).13 In fact, a long monopoly period can serve as a deterrent to copycats as most consumers will have already purchased by the time the copycat enters the market.

In general, the manufacturer will invest in both quality improvement and advertising when consumers are impatient. This allows the manufacturer to sell to a large group of impatient consumers during the monopoly phase (before entry of the copycat) while simultaneously attracting consumers after entry of the copycat (with the improved quality of the genuine product).

If the copycat is able to react more quickly, the monopoly period is reduced to a shorter time. The manufacturer must make an adjustment to advertising and pricing to deter the copycat (case II). However, as the copycat’s delay becomes even shorter, the manufacturer no longer benefits from the combative effects of low prices and advertising. Instead, the manufacturer will raise first period prices (to increase revenues from the smaller pool of consumers who purchase very early) and lower second period prices to compete with the copycat (case III).

Consumer Behaviour

The manufacturer and copycat are not the only players in this game. We also must consider consumer patience and the level of strategic behaviour displayed by consumers. Each of these plays an important part in identifying the strategies of the manufacturer and copycat.

Consumer patience – patient consumers are willing to wait for a more attractive deal (lower prices) in the future, while impatient consumers will purchase immediately. A high proportion of impatient consumers are generally detrimental to the copycat. Impatient consumers will generally purchase early (before the copycat product is available) and those who do not purchase early are often unwilling to pay a retail price that the copycat will find attractive. This leads to a case I scenario for the manufacturer.

When more consumers are patient, the copycat is less likely to be deterred by consumer characteristics alone. Instead, the manufacturer must make an adjustment to advertising and pricing to deter the copycat (case II). However, the range of consumer patience that rewards the manufacturer for this behaviour has its limits. At some point, the copycat can no longer be deterred because too many consumers are willing to wait for the copycat product. At this point, the manufacturer no longer benefits from the defensive effects of low prices and advertising. Instead, the manufacturer will raise first-period prices (to increase revenues from the smaller pool of impatient consumers) and lower second-period prices to compete with the copycat (case III).

Consumer strategy – when consumers have sufficient information about the future (such as announcements of forthcoming generic pharmaceuticals or memories of prior years when fast-fashion versions of designer clothing have been introduced), they can anticipate the eventual entry of the copycat into the market. This should be beneficial to the copycat, but this is not universally true. In fact, the copycat benefits from consumers becoming more strategic only if consumers are also impatient or if nearly all consumers are highly strategic. This counterintuitive result is the result of spillover from the manufacturer to the copycat. When consumers are less strategic, the manufacturer has a greater incentive to build the market through advertising (but this leads to more potential consumers for the copycat as well). Additionally, the manufacturer will also increase prices, leaving more room for the copycat to compete. At the same time, when consumers are impatient, the manufacturer will not sacrifice early revenue (by lowering monopoly period prices) for the ability to deter the copycat later. In general, our model shows that the manufacturer can benefit from increasing consumers’ impatience by instilling in them a “buy now” mentality by advertising, for example, to extol the immediate benefits of ownership.

Evaluation

With our findings in mind, we now examine several recent scenarios to evaluate both the situation and strategies employed.

Fashion

As a manufacturer of very high-quality/high-status clothing, Burberry is unlikely to be willing to make the downward adjustments in price and advertising necessary to allow it to deter copycats. In fact, Burberry is most definitely not going to sacrifice its profits and market size just to keep fast-fashion firms from emulating them. This is particularly true because fast-fashion firms such as Forever21 and Zara have low fixed costs and their advertising expenditures are low.8 Accordingly, Burberry’s best strategy begins with maintaining separation between themselves and the copycats, as there is no way to make a credible or actual threat that is sufficient to deter the copycats. This adaptation begins with quality (both actual and perceived) and naturally extends to pricing as well. Burberry’s worst nightmare would be a price war with Zara (enforcing the threat). Burberry’s next steps depend upon the nature of their consumers. The primary consumers for high-end fashion goods are known to be quite impatient; as they derive a good portion of their utility early in the season by having the latest fashions at the time they are available (e.g. wearing the latest summer clothes when summer begins). However, these consumer characteristics lead to a favourable situation for low-cost copycats who can quickly enter a market. Specifically, Burberry will advertise to build the market, and is able to charge a high price in the first phase (before introduction of the copycat) because some consumers are willing to pay a premium to own the product early. However, the combination of a large potential market with a significant number of consumers who are unwilling/unable to pay the premium price sets the stage for a successful copycat (after the copycat has been able to produce its version of the product). Unfortunately for Burberry, the combination of impatient consumers and its own unwillingness to sacrifice profits solely to deter a copycat make it impossible to avoid the copycats. Even worse, as copycats become faster and faster at producing their products, strategic consumers are more likely to be willing to wait the relatively short time to purchase a competing product at a steep discount. Burberry’s best strategy is to maintain a significant quality advantage over the copycats (which the copycats are not likely to challenge for fear of entering into a price war) and to try to lengthen the time between introduction of their own product and the inevitable emergence of copycats. Burberry’s efforts at streamlining its supply chain and shortening the time between runway and retail shelf (to zero in their strategic plan) are well-designed.

Pharmaceuticals

In the pharmaceutical market, Mylan faced a somewhat different challenge. In the winter of 2016, it was very likely that a generic version of the EpiPen (produced by Teva) would be approved by the FDA. This placed Mylan squarely into our two-phase scenario. Prior to FDA approval, Mylan had a virtual monopoly, but consumers could anticipate the eventual transition to a market with both the Mylan and a generic version of the product. The situation for Mylan was similar, but not identical, to the problem faced by Burberry. Mylan had a high-quality product and consumers could certainly be considered to be impatient (few consumers are willing to wait long for such a life-saving device). However, given the broad acceptance of generic versions of brand name pharmaceuticals, it is hard to argue that Mylan would enjoy an overwhelming quality differentiation compared to its future competitor (the generic version of pharmaceuticals is still supported by FDA approval). Instead, it is likely that consumers would view the Mylan product as having high quality and the generic alternative as having acceptable quality. For the copycat, this is the best possible outcome. Mylan, with an impatient set of consumers and a high-quality product, is unwilling to reduce its revenues (through price and/or advertising reductions) to deter the copycat. This leaves the copycat free to enter the market and also leaves considerable room (in terms of price and quality) for the copycat to carve out a niche. In this case (where the manufacturer cannot economically discourage a copycat), the manufacturer’s first-period (monopoly phase) price will be high. After the copycat enters the market, the manufacturer will be forced to drop prices precipitously to compete for the remaining price-sensitive patient consumers or must limit itself to those few consumers with a high valuation for the brand name product that are willing to continue to pay high prices. Accordingly, Mylan was making the wise choice – raise prices while in the monopoly situation to maximise profits with an eventual decrease to compete with a low-price copycat when that situation arises.

As events developed, however, the generic version of the product was not approved by the FDA. This left Mylan prepared for a copycat (poised to lower prices and aggressively compete with the newcomer) but with no reason to actually implement this strategy. Instead, Mylan faced accusations of price gouging and abuse of its monopolistic market position. With no competitor, there was no force pushing Mylan to lower its prices. However, the threat was still real, and therefore Mylan’s best strategy (from an economic perspective, but definitely not in terms of public relations!) was to treat this as an extended first-period phase and to maintain high prices in anticipation of an eventual case II situation.

The patent infringement case filed by AbbVie was ultimately dismissed and the U.S. Department of Health and Human Services approved the DRL abbreviated new drug application14, allowing them to produce a generic version of AbbVie’s Zemplar® product. DRL announced the introduction of its generic version of Zemplar® in September of 2016.15 At approximately the same time (October, 2016), the U.S. FDA announced the approval of a capsule version of Zemplar® for treatment of pediatric patients16, leaving AbbVie with a new outlet for its brand -name product.

Finding itself in a case III situation, AstraZeneca has pursued an extended (over 9-year) legal battle to maintain its exclusivity on Crestor®. Although it is impossible to foresee precisely how the availability of generic forms of Crestor® may be priced, the example of alpha-beta blockers (used to reduce high blood pressure) shows that in the first 12 months of generic availability, the daily cost of treatment fell by 75.5%.11 If Crestor® follows this pattern, AstraZeneca may find itself unable to compete on a cost basis with the copycats and will instead be forced to rely on those few consumers who will pay a high price for brand name Crestor®.

Conclusion

While we have discussed these results in terms of two specific industries (pharmaceuticals and high fashion), our results can be applied to a wide variety of scenarios. Most importantly, we have seen that many accepted strategies (reducing time-to-market through supply chain redesign, increasing product quality, encouraging consumers to “buy now” etc.) could have beneficial results when a firm is facing the threat of copycats.

In our specific examples, Burberry is a victim of its own success. Its high quality and loyal consumers make it difficult (or impossible) to make the sacrifices in product margin and/or prestige that would be necessary to deter copycats from introducing their own version of its products. Accordingly, Burberry’s only recourse is to try to increase the time it has to sell its products without competition (by speeding up its supply chain) and to pursue possible legal recourse when copycats are too faithful in their reproductions.

Mylan, on the other hand, may have had the bad fortune (in terms of public perception) of having its competitors thwarted by legal action. While Mylan took the prudent step of raising prices during the period where it did not face a competitor, the failure of this competitor to emerge left Mylan with a public relations disaster as it had no opportunity or impetus to take the subsequent step of decreasing prices to engage in price competition with its now non-existent competitor. Therefore, Mylan was left in the uncomfortable position of defending what was likely designed to be a temporary price increase, which became more or less permanent. A further illustration of Mylan’s need for a lower-price competitor is the recent revelation that Mylan itself has introduced a low-cost version of the EpiPen to compete with its own product and Teva’s generic version of the Epipen was finally approved by the FDA in August, 2018.17

Our study, and these examples, shows the complexity of the problem faced by firms, which must compete with low-cost, low-overhead competitors. In Figure 1, we capture the mechanisms of how quality, consumer patience, and consumer strategy lead to each of the three cases (and their related deterrence strategy). Figure 1 also includes examples of the manufacturer’s recourse for case III scenarios.

[/ms-protect-content]

About the Authors

Gregory DeYong is an Assistant Professor at Southern Illinois University. His research focuses on production scheduling, purchasing, and counterfeit products.

Gregory DeYong is an Assistant Professor at Southern Illinois University. His research focuses on production scheduling, purchasing, and counterfeit products.

Hubert Pun is an Associate Professor at the Ivey Business School (Western University). His research interests include co-opetition, counterfeiting product, and how blockchain can be used as an enterprise solution.

Hubert Pun is an Associate Professor at the Ivey Business School (Western University). His research interests include co-opetition, counterfeiting product, and how blockchain can be used as an enterprise solution.

Carol Lucy is an Assistant Professor at Emporia State University. Her research interests include entrepreneurship, organisational behaviour, and small business management.

Carol Lucy is an Assistant Professor at Emporia State University. Her research interests include entrepreneurship, organisational behaviour, and small business management.

References

1. Statista (2016). U.S. Pharmaceutical Industry – Statistics & Facts, retrieved from https://www.statista.com/topics/1719/pharmaceutical-industry/ on September, 17, 2018.

2. Lieber, C. (2018). Fashion brands steal design ideas all the time. And it’s completely legal. Vox, April 27, 2018. Retrieved from https://www.vox.com/2018/4/27/17281022/fashion-brands-knockoffs-copyright-stolen-designs-old-navy-zara-h-and-m on July 11, 2018.

3. Bowlus, J. (ed.). “Industry Explorations: United States Pharmaceuticals 2015.” Global Business Reports, 2015. p. 12. Available from https://www.gbreports.com/publication/united-states-pharmaceuticals-2015.

4. National Pharmaceutical Services, “Drugs coming off patent by 2022,” Available from https://www.pti-nps.com/nps/wp-content/uploads/2017/04/NPS_Drugs-Coming-Off-Patent-by-2022-Web.pdf.

5. Thomas, K. (2018). Patients Eagerly Awaited a Generic Drug. Then They Saw the Price. The New York Times, February 23, 2018. pp. B1.

6. Barriaux, M. (2007). Financial: AstraZenenca to sue copycat drug makers. Guardian Financial Pages, December 13, 2007.

7. Pollack, A. (2016). AstraZeneca pushes to protect Crestor from generic competition, The New York Times, June 27, 2016. Retrieved from https://www.nytimes.com/2016/06/28/business/astrazeneca-pushes-to-protect-crestor-from-generic-competition.html?_r=0 on April 4, 2017.

8. Hansen, S. (2012). How Zara grew into the world’s largest fashion retailer. The New York Times Magazine, November 9, 2012. Retrieved from https://www.nytimes.com/2012/11/11/magazine/how-zara-grew-into-the-worlds-largest-fashion-retailer.html on September 17, 2018.

9. Frost, A. (2014). Forever 21, H&M, Zara, Uniqlo: Who’s Paying for our Cheap Clothes? Retrieved from https://groundswell.org/forever-21-hm-zara-uniqlo-whos-paying-for-our-cheap-clothes/ on October 19, 2018.

10. Pun, H., & DeYong, G. D. (2017). Competing with Copycats When Customers Are Strategic. Manufacturing & Service Operations Management,, 19(3), 403-418.

11. Berndt, Ernst R., and Murray L. Aitken. “Brand loyalty, generic entry and price competition in pharmaceuticals in the quarter century after the 1984 Waxman-Hatch legislation.” International Journal of the Economics of Business, 18, no. 2 (2011): 177-201.

12. Schmidle, N. (2010). Inside the Knockoff-Tennis-Shoe Factory, The New York Times Magazine, August 19, 2010.

13. Milnes, H. (2018). Speed-to-market: How luxury brands are picking up the pace of production cycles. Glossy, January 8, 2018.

14. United States Department of Health and Human Services, ANDA204910 Approval, August 17, 2016. Retrieved from https://www.accessdata.fda.gov/drugsatfda_docs/appletter/2016/204910Orig1s000ltr.pdf on July 11, 2018.

15. Business Wire (2016). Dr. Reddy’s Laboratories announces the launch of Paricalcitol injection in the U.S. market. Retrieved from https://www.businesswire.com/news/home/20160919005798/en/Dr.-Reddys-Laboratories-Announces-Launch-Paricalcitol-Injection on July 18, 2018.

16. Department of Health and Human Services (2016). Supplement Approval, Retrieved from https://www.accessdata.fda.gov/drugsatfda _ docs / appletter /2016 / 021606Orig1s016,s017ltr.pdf on October 26, 2018.

17. U.S. Food & Drug Administration (2018). FDA approves first generic version of EpiPen, retrieved from https://www.fda.gov / newsevents / news room / pressannouncements / ucm617173 . htm on October 26, 2018.

")