The corporate office consists of the CEO and the corporate functions. It is the main vehicle for delivering corporate added value. Yet corporate functions often underperform and corporate offices often fail to add value. We argue that this is because CEOs focus most of their attention on portfolio strategy and business issues and give too little attention to guiding and leading their own business – the corporate office.

Surprisingly many CEOs give too little attention to the corporate functions that make up their corporate office. This is because they consider their main priority to be business issues. This lack of attention is well illustrated by the corporate CEO of a global consumer goods company who cancelled a major project aimed at clarifying the role of the corporate functions with the words “I do not have time for this at present. We have too many pressing business problems to afford the luxury of gazing at our corporate centre navels.”

The lack of attention by CEOs to corporate functions is evident in our research on how heads of corporate functions develop strategies for their functions. We asked these leaders whether the CEO or an executive committee member briefed them thoroughly when they were appointed to lead the function. Surprisingly many said they were given little guidance. In more than 40 interviews with functional heads who report directly to the CEO, only a few had been briefed about the corporate-level strategy and the role that the function was expected to play in this strategy.

Some corporate functional heads were given the job without any guidance. Others were expected to develop a strategy for the function based on interactions with the executive committee. Some were appointed because they were known to have special skills at centralising or decentralising or setting up shared services or improving functional performance, but often still received little direct guidance. This appears to be an embarrassing critique of corporate CEOs. But, is it? Is it important for CEOs to provide the heads of corporate functions with clear guidance and, if it is, why do they fail to do so?

[ms-protect-content id=”9932″]The purpose of this article is to explain why it is important for CEOs to give more attention to their corporate functions. We provide three reasons: corporate functions help provide the guidance and constraints that enable the corporate office to add value; without some unifying work by the CEO the work of corporate functions will not be coordinated; left to their own devices corporate functions can be bureaucratic and costly. We will close with some thoughts on how CEOs can become more involved in designing corporate functions and in monitoring their performance.

Corporate functions help deliver corporate strategy

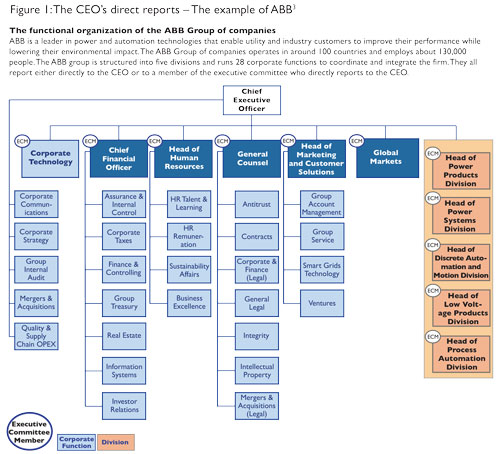

Most large companies are organised into business divisions that report to a corporate office.1 The corporate office houses the corporate CEO and a number of corporate functions, such as Finance, Human Resources, Information Technology, Legal, Communications, etc. Of the managers who report directly to the corporate CEO, about half of them are heads of businesses, while the other half are heads of corporate functions.2

While corporate CEOs also need to keep an eye on the businesses, their main responsibility is to define and implement the corporate strategy.4 The corporate strategy involves making decisions in three areas:5

• which businesses and market sectors to focus on,

• what guidance and constraints to give to the business divisions so that they perform better as a collective than as independent entities (the added value), and

• how to organise the corporate office and corporate processes to ensure that the guidance and constraints are provided and the value added.We observe that most corporate strategy processes focus on the choice of businesses, on the strategies for those businesses and on how much to invest in each business. Little attention is normally paid to the added value question or to the organisation and processes of the corporate office. This is not to say that there is no discussion on these organisational issues; it is just uncommon for the discussion to be part of the corporate strategy process.

This businesses-based view of corporate strategy creates confusion between corporate-level strategy and business-level strategy. While portfolio strategy is clearly a task for the corporate strategy process, decisions about the strategy each business should pursue and the amount each business should invest are essentially business-level strategy issues,6 not corporate-level strategy issues. In other words the management teams of each business should be proposing the strategies to optimise the positioning of their businesses.

The role of the corporate office is to interact with the management teams of the businesses (guidance and constraints) in ways that help them perform better than they would as independent companies.7 Hence, once the portfolio decisions have been made, the next part of the CEO’s business should be to define how the corporate level helps business managers perform better than they could unaided.

It is worth focusing on this point a little longer. The justification for a corporate whole is the extra performance that can be created over and above that of the individual businesses – the added value.8 Without added value, the corporate office is an extra cost burden on the businesses. In other words, articulating this added value should be a critical agenda for the CEO. Without clarity on the sources of added value, the extra value is unlikely to be created, and managers in corporate functions will not have clear goals around which to develop their strategies.

Once the sources of added value are clear, the final part of the CEO’s business should be to define the executives, skills, functions and processes of the corporate office that will ensure that the value is added. In other words, the CEO should provide guidance to corporate functions so that they can be part of the delivery process for the corporate added value.

So why does this not happen? Why are corporate strategy processes biased towards portfolio decisions? Why is so little attention given to the sources of added value and the role of corporate functions in delivering the added value?

In a parallel research project, we uncovered more than a dozen reasons. These ranged from distractions, such as new governance requirements; issues that arise in the businesses that require immediate attention; political difficulties with regard to reviewing corporate functions; and uncertainty about the best way to define the added value of the corporate office and align the functions behind this added value. However, one of the most common reasons was that CEOs (and corporate strategists)9 do not see the three parts of corporate strategy as equally important. They focus on portfolio and investment decisions, and do not feel the same responsibility for defining the added value of the corporate office or for designing the corporate functions: they do not see the corporate office as an essential part of their own business.

Corporate functions often develop idiosyncratic strategies

Our research also showed that the way corporate functions develop their strategies is highly dependent on the personality and experience of the head of the function rather than on an understanding of the corporate strategy. We found that they developed their functional strategies in a variety of idiosyncratic ways.

Some functional strategies were driven by experiences that the head of the function had had in previous jobs with other companies. As one head of IT explained: “I have always pushed for central control of infrastructure and IT operating systems because this is the only way I have found to raise standards, increase standardisation and control costs.” In contrast, in another company the head of IT suggested the opposite: “Undoubtedly, decentralised IT processes help keep costs down. Once you centralise, each system runs at the same high standards which results in gold-plated projects that do more than the businesses need.”

Other functional strategies were driven by what the business divisions were willing to accept: “You should start by winning the trust of the business divisions. I don’t like to launch any initiative without the full support of the businesses.” In other cases, the head of the function assessed the situation, identified areas in which he or she believed the function could add value and presented the corporate executive committee with a plan of activities for approval.

These processes may have all resulted in good functional strategies. However, with these idiosyncratic approaches the strategies of different corporate functions are unlikely to be aligned. None of our interviewees suggested that they had developed their functional strategy in collaboration with other corporate functions.

Unless the CEO gives more attention to corporate functions, there is little chance of achieving alignment within the corporate office and of delivering the coordinated “guidance and constraints” to business divisions that is needed to create the corporate added value.

Corporate functions can become bureaucratic and costly

Corporate functions can be a major source of under-performance.10 Left to their own devices, corporate functions, like the rest of us, tend to pursue their own agendas. Believing in the importance of their function, managers look for ways to increase their influence and impact. This can cause functions to set policies, introduce processes and build staff that seem sensible from a functional perspective but impose burdens and constraints on businesses that make it harder for them to succeed. “I am from head office and I am here to help you,” is a widely recognised joke. This is because business divisions the world over have experienced well meant but misguided interference from head office functions.

Our research uncovered numerous situations in which the current head of the function explained that, before he or she arrived, the previous function was underperforming. As one head of HR pointed out “When I joined I was told we had a great performance management system. But when I went out to the businesses, I got a Gallic shrug. They had no connection with the system. Someone in HR had created this huge system that was not understood or used properly.”

Left to their own devices, corporate functions can seek to make their job easier. They standardise processes to simplify the work they need to do. They restrict services to reduce peaks and troughs. They impose constraints on businesses so that they have less variation to deal with. These actions can all lead to efficiency gains within the corporate function, but they can also create difficulties for the businesses. Often the costs imposed on the businesses are greater than the savings in the corporate function.

Left to their own devices, corporate functions can become inefficient. They add staff, fail to raise standards and resist change. As the late Sumantra Ghoshal used to comment: trying to make something happen in some companies is like walking through Calcutta in the monsoon. He compared this to walking in the woods near Fontainebleau in spring. “In one environment, every step saps your last resources of energy. In the other, every new vista brings new energy and excitement.”

How CEOs can pay more attention to corporate functions

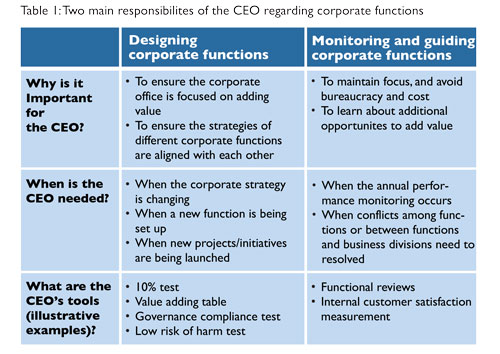

Unless CEOs give more time to corporate functions, they will not be aligned with the corporate strategy, they will not be well coordinated, and they will be prone to underperformance. So what should CEOs do? The following suggestions are based on our view of corporate strategy and on insights we have gained from those companies that appear to be doing a better job of managing corporate functions. We distinguish between designing the function and monitoring the function once it has been designed.11

Designing corporate functions

CEOs can ensure that the corporate strategy process generates clarity about the sources of corporate added value. One way to do this is to insist that the corporate strategic plan defines a handful of sources of added value, often as few as three, that meet the 10% test: each source of added value is expected to increase the market capitalisation of the overall company by at least 10% above what it would be without the corporate office.12

An example of added value that meets the 10% test is Jack Welch’s requirement in the 1980s that GE’s business divisions generate credible plans to become the global No. 1 or No. 2 in their markets. Those that failed the challenge were fixed, sold or closed. This “guidance” caused the management teams to move their sights from local US markets to global markets and helped GE transition from a strong US company to a world leader.

Another example is the advice Barry Diller, CEO of Interactive Corp, gave his young internet businesses, such as Expedia and Hotels.com. He encouraged them to negotiate harder with suppliers. Moreover, he backed this up with a willingness to lead some of the negotiations himself. As a result, he helped many of his businesses cut their costs by 20-30%.

With a short list of big sources of added value, the CEO can use a simple table to help align the design of corporate functions. The table shows the large sources of added value down the left column and lists the main corporate functions along the top row. In the table’s text boxes, the contribution that each function makes to each source of added value can be defined. Sometimes, there is no contribution. Sometimes all the functions make some contribution. By clarifying the part each function plays in each of the main sources of added value, the CEO is providing guidance for the design of the corporate function.

Once the added value role of each function is clear, functional heads can consider additional layers of functional activity. One source of additional activity comes from non-discretionary items, such as financial reporting, and controls, such as internal audit. Because functions often attach more importance to their functional controls than is warranted from a commercial perspective, CEOs should check that these non-discretionary and control activities are really needed. In one company, the CEO requires that each function lists all the mandated policies or controls it will impose on the business divisions, and submits them each year for him to sign off.

The final layer of functional activity involves smaller sources of added value, such as central payroll, accounting services or a planning services unit. These activities do not meet the 10% test, but they can still add value. Here, it is important that the CEO challenges each of these activities to make sure that they do not create any negative side effects for the business divisions. Because the gains are less than 10%, the CEO should take no risks. If there is a chance that these activities will harm the businesses, they should be eliminated.

By helping define the major sources of added value, by checking that non-discretionary and control activities are necessary and by excluding any additional activities that may have negative consequences for the businesses, the CEO can guide the design of the functions in the corporate office.

Monitoring corporate functions

There are forces at work that cause corporate functions to lose focus, build bureaucracy and interfere with business divisions. This is especially true in the current environment as many companies are increasing their degree of centralisation.13 As a result, the CEO and executive committee need to continuously monitor these functions.

CEOs can employ many different tools. For example, corporate functions can be asked to annually present their functional plans so that their peers and the heads of the major businesses can challenge and review them. The agenda of the annual planning process is often crowded with reviews of business plans. Therefore, reviews of corporate functional plans can be carried out at a different time of the year or spread throughout the year. The timing of the review is not critical; the annual discipline of being challenged is the objective.

Another possibility is to regularly score the satisfaction level of each business division with each corporate function. Since the main role of most corporate functions is to add value to the businesses it is helpful to survey the businesses to assess their satisfaction. In one company, the CEO insisted that the businesses provide monthly feedback on a new central marketing team that he had set up. Monthly feedback is not likely to be appropriate for all functions, but it may be beneficial when a new function is set up. For mature functions an annual satisfaction scorecard helps create an objective benchmark against which the annual functional review can take place.

Corporate functions need the CEO’s attention

Over the last few years, many companies have created centralized functional activities and corporate functions have become more influential. This, however, does not seem to be reflected in the attention CEOs devote to corporate functions. Creating a high performing corporate office is not an easy task. This is partly why many CEOs pay too little attention to this topic. One CEO explained, “I have not tackled the corporate functions because I do not want to open this political minefield. Once you launch a review of the corporate centre you unleash dangerous forces.”

However, the performance of the corporate functions is at least as important to the success of the overall company as the performance of a large business division. Moreover, corporate functions make up the CEO’s personal team. Each divisional management team has a business to run. The CEO’s business is the running of the central team to ensure that, together, the “guidance and constraints” given to the business divisions add value. By ensuring that the corporate strategy process defines the main sources of corporate added value and by linking functional plans to these sources of added value, CEOs can improve the performance of corporate functions and enhance the value of their companies.

About the Authors

Andrew Campbell is one of three directors of the Ashridge Strategic Management Centre, which is a research centre devoted to issues concerning the management of multi-business companies. His current work programme includes directing research projects, running management programmes on strategy, lecturing to large and small audiences and acting as a consultant to client companies.

Sven Kunisch is a senior research fellow and lecturer at the University of St.Gallen (Switzerland) and formerly a visiting fellow at Harvard Business School. His main research interest is strategic management, particularly corporate strategy. He has published several articles on a variety of strategy topics and co-edited three books, most recently From Grey to Silver—Managing the Demographic Change Successfully.

Günter Müller-Stewens is a professor and the managing director of the Institute of Management at the University of St.Gallen (Switzerland). His research interests centre on corporate strategy, mergers and acquisitions and the strategy process. He has co-authored several strategy books, most recently Corporate Strategy & Governance. He is the academic director of the master of strategy and international management (SIM) programme at the University of St.Gallen, which is ranked number 1 in the Financial Times’s global ranking.

References

1. For example, see: Chandler A. D. (1962), Strategy and Structure: Chapters in the History of the American Industrial Enterprise. MIT Press: Cambridge, MA. Strikwerda J. and Stoelhorst J. W. (2009), ‘The Emergence and Evolution of the Multidimensional Organization,’ California Management Review 51(4): 11-31.

2. Neilson G. L. and Wulf J. (2012), ‘How Many Direct Reports?,’ Harvard Business Review 90(4): 112-119. For more information on functional managers see: Guadalupe M., Wulf J. and Li H. (2012), ‘The Rise of the Functional Manager Changes Afoot in the C-Suite,’ The European Business Review (May-June): 9-13. Menz M. (2012), ‘Functional Top Management Team Members: A Review, Synthesis, and Research Agenda,’ Journal of Management 38(1): 45-80.

3. Source: ABB website (accessed 2013-02-06): http://www.abb.com/cawp/abbzh252/0d19f10409ed9884c1256aed0048503a.aspx.

4. For more general information on the roles of the CEO, see: Finkelstein S., Hambrick D. C. and Cannella Jr. A. A. (2009), Strategic Leadership: Theory and Research on Executives, Top Management Teams, and Boards. Oxford University Press: Oxford.

5. Porter M. E. (1987), ‘From Competitive Advantage to Corporate Strategy,’ Harvard Business Review 65(3): 43-59. Goold M., Campbell A. and Alexander M. (1994), Corporate-Level Strategy: Creating Value in the Multibusiness Company. Wiley: New York, NY.

6. Porter M. E. (1980), Competitive Strategy. Free Press: New York. Porter M. E. (1985), Competitive Advantage. Free Press: New York.

7. Chandler A. D. (1991), ‘The Functions of the HQ Unit in the Multibusiness Firm,’ Strategic Management Journal 12: 31-50.

8. Campbell A., Goold M. and Alexander M. (1995), ‘Corporate Strategy: The Quest for Parenting Advantage,’ Harvard Business Review 73(2): 120-132. Collis D. J. and Montgomery C. A. (1998), ‘Creating Corporate Advantage,’ Harvard Business Review 76(3): 71-83.

9. For recent research on the chief strategy officer, see for example: Breene R. T. S., Nunes P. F. and Shill W. E. (2007), ‘The Chief Strategy Officer,’ Harvard Business Review 85(10): 84-93. Menz M. and Scheef C. (forthcoming), ‘Chief Strategy Officers: Contingency Analysis of their Presence in Top Management Teams,’ Strategic Management Journal, 1-22.

10. Campbell A., Goold M. and Alexander M. (1995), ‘The Value of the Parent Company,’ California Management Review 38(1): 79-97. Empirical research has shown a huge variety in the performance of the corporate parent. See for example: Collis D. J., Young D. and Goold M. (2007), ‘The Size, Structure, and Performance of Corporate Headquarters,’ Strategic Management Journal 28(4): 383-405. Nell P. C. and Ambos B. (forthcoming), ‘Parenting Advantage in the MNC: An Embeddedness Perspective on the Value Added by Headquarters,’ Strategic Management Journal http://ssrn.com/abstract=2050359.

11. In a companion article, we suggest an alternative approach. See Campbell A., Kunisch S. and Müller-Stewens G. (2012), ‘Are CEOs Getting the Best from Corporate Functions?,’ MIT Sloan Management Review 53(3): 12-14.

12. This logic is similar to the logic applied in centralization decisions. See: Campbell A., Kunisch S. and Müller-Stewens G. (2011), ‘To Centralize or Not to Centralize,’ McKinsey Quarterly 2011(June): 1-6.

13. Kunisch S., Müller-Stewens G. and Collis D. J. (2012), Housekeeping at Corporate Headquarters: International Trends in Optimizing the Size and Scope of Corporate Headquarters, Survey Report. University of St.Gallen/Harvard Business School: St.Gallen/Cambridge. Also, see: Rajan R. G. and Wulf J. (2006), ‘The Flattening Firm: Evidence from Panel Data on the Changing Nature of Corporate Hierarchies,’ Review of Economics & Statistics 88(4): 759-773. Wulf J. (2012), ‘The Flattened Firm: Not as Advertised,’ California Management Review 55(1): 5-23.