By Dr. Mark Esposito, Dr. Alessandro Lanteri and Dr. Terence Tse

The Covid-19 pandemic has been a major disruptor for tried and tested approaches to strategy and an accelerator of new emerging approaches. In this article we present two research-based frameworks of emerging approaches to strategic decision-making. The first, DRIVE (Tse and Esposito, 2017), is a macro-level framework that maps the contextual megatrends shaping the socio-economic ecosystem. The second, CLEVER (Lanteri, 2019), is a meso-level framework that describes the drivers of successful strategy implementation. Jointly, the two frameworks constitute the foundation of a new strategic architecture that empower firms to identify growth opportunities and successfully organize to pursue them in the turbulent, post-pandemic world economy.

The Covid-19 pandemic has been a major disruptor for tried and tested approaches to strategy. More specifically, it acted as an accelerator of two emerging approaches: digital transformation (Soto-Acosta, 2020) and sustainability (Barbier and Burgess, 2020). Even as the pandemic still impacts our lives and livelihoods, companies are stepping up their efforts and new imperatives and business models are emerging every day, as a form of validation of new organizational practices and norms. The pandemic has not only changed our perception of the world but equally accelerated our adoption to new forms of work and production which are becoming visible by the day.

A new survey reveals that 38 percent and 31 percent of managers answered, “we need to re-evaluate” and “we are taking steps to change”, respectively, when responding to how the coronavirus event is affecting their decisions on digital transformation (EY, 2020). In another study, 70 percent of executives surveyed in Austria, Germany and Switzerland claimed the pandemic had pushed them to accelerate the pace of digital transformation within their firms (Malev, 2020). In a survey of almost 1,600 CEOs from 83 countries, 25 percent of the respondents strongly agreed that “climate change initiatives will lead to significant new product and service opportunities for [their] organisation” (PWC, 2020). And in a private conversation with a senior McKinsey’s partner, it was stated that most of the firm’s clients have witnessed an acceleration of roughly 6-7 years in average, on the efforts of digital transformation across industries, sectors and geographies. So, the change did not just allegedly happen, it did happen from the experience of what we have been able to assess in our own practice of educators, consultants and advisors.

These findings are not surprising: companies that are more aggressive in digitizing their activities are more likely to end up achieving superior economic performance (Bughin et al., 2017) and those that actively manage a wide range of sustainability indicators are better able to create long-term value for all stakeholders (Funk 2003).

How do business leaders seize these opportunities?

A strategic architecture

While the challenges with new normal is always related to the ability to identify existing frameworks that could help and the synthesis of some of the issues we are facing, in this article we present two research-based frameworks of emerging approaches to strategic decision-making that jointly help decision makers to identify growth opportunities and successfully organize to pursue them in the turbulent, post-pandemic world economy. These frameworks were originally designed by aspiring to future fitness, in integrating adaptable and flexible thought processes in their functioning. They were designed as non-exhaustive instruments, purported to grasp the flow of the times in which we are living, rather than advocating seminal theory within 3 levels of critique utilized to best capture the entropy of events, in an ever-complex world, where linear models of distribution are less and less functional to the purpose of prediction and forecast.

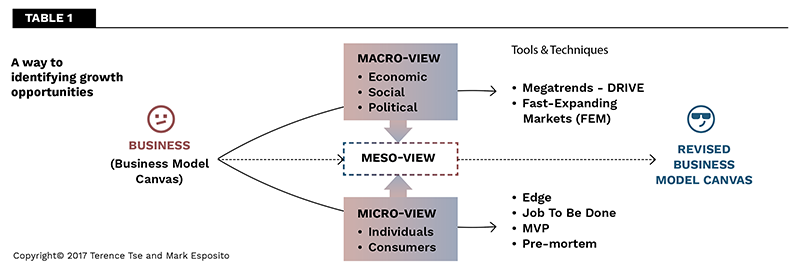

The macro level of analysis taps on the contextual need to assess the environment and the nature of the forces that are shaping the conditions for business and public policy to operate. From the scanning of the externalities to the detection of grassroot movements, to the discovery of growth models undetected by traditional economic indicators (Esposito, Tse, Soufani, 2013), this level of analysis is needed to determine magnitude and direction of the trends.

The meso level of analysis refers to the institutional and intermediated level of the economy in which a necklace of entities is operating as connectors between forces at the macro and execution on the micro. The meso level provides opportunities for formulation of strategy, ideation of business models which probe markets and reconfigure systems. It is an important aspect of how systems become purposeful.

The micro level involves the most active agents in the economy, such as consumers and individuals, who make decisions on the foundations of limited information, sentiments and access to opportunities. It is where markets get validated and where decision making blends theoretical assumptions with projectable actionability and where the socio-economic system enables itself.

The first of these frameworks, DRIVE (Tse and Esposito, 2017), is a macro-level framework that maps the contextual megatrends shaping the socio-economic ecosystem and the trajectories emerging from it. The second, CLEVER (Lanteri, 2019), is a meso-micro level framework that describes the drivers of successful strategy implementation and provides access to a series of actionable levers which can turn vision into reality.

Understanding how ’DRIVE’ brings the macro level of analysis to life

During the research conducted, we have observed, pivoted, and researched several points of junction, where the current trends of the present set the trajectory for events to occur in the future, and we believe that these elements carry significance. In the vast ocean of knowledge, information, and data, we find that there are five undercurrents that can give us some directions as to how the future would unfold. These five paths aren’t exclusive or exhaustive. Most are likely just a minimal representation of all undercurrents that interplay with the shaping forces of our societies, but with this in mind, we have narrowed the research down to five megatrends, which we call the DRIVE framework, consisting of the following:

- Demographic and Social Changes

- Resource Scarcity

- Inequalities

- Volatility, Scale, and Complexity

- Enterprising Dynamics

We believe that each of these megatrends is unique in its own right, but, in combination, they can present a fairly comprehensive picture of what the future holds and help us picture a future in the making. Let’s look at them under each individual lens, to best understand the overall purpose of the conceptual framework.

Demographic and Social Changes

At the center of any future state are people. It is now a known fact that the populations in the developed world are both shrinking and aging, partially a result of the combination of very high life expectancy and very low fertility rates. This is particularly visible if we tap on the visuals of any population pyramid today, which is an easy, albeit serious, effort to envision how populations are distributed by gender and segments of age, from zero to 85+. Interestingly, it was called a pyramid because it implied that children, the base of the population pyramid, are more numerous than elderly, hence the renowned shape. But from a glance of global population pyramid today, versus a comparison of population pyramid in 1970, the differences are astounding. Children are yet the most populous group in our societies, but only by marginal units. The pyramid is changing in shape and converging more into a dome, so to say—fatter at the bottom up to 50 years of age and thinner from 50 and above, but definitely far from resembling a pyramid at best. Projections show that the majority of populations of developed countries will be over 40 years old by 2030, with Japan reaching an average of 52 by then, followed by Italy and Germany. Less obvious though, the same is happening in the developing economies. Take China, for instance. Even though the Middle Kingdom has a younger population (35.4) today than the United States (37.4), by 2030 this will be 42.1 compared to 39.5—China’s aging population is going to “catch up” with the developed world (Roland Berger Strategy Consultants, 2015). Most emerging economies remain young, however.

The most youthful are those of the sub-Saharan region. For example, the average age of Nigerians is 15 years old in 2013. Yet, by 2030, the average age of the country would only be 15.2 years old!

The implications of such demographic shifts can be huge and destabilizing at best. While the developed world will be facing challenges such as maintaining and sustaining the social security systems and financing pensions, because of an influx of its elderly population, the developing ones will have to be able to provide education and access to basic health care to youngsters as well as create jobs for them. On a global basis, as people are getting older, the world ’ s population will plateau for the first time in human history. A worrying implication is that there will be insufficient labor power to support the old-age pensioners (Dobbs, Ramaswamy, Stephenson, & Viguerie, 2014). With the labor pool shrinking, the only way to maintain economic growth is to continuously invest in raising productivity and competitiveness, away from natural resources and more toward models of economic efficiency that do not resort to intense factors of production, to extract value. This not only requires companies to increase their efforts—and capital—in making investments, at least in the medium term, but this could also put governments in a dilemma. What is needed are more liberal economic and business policies, as past experience has shown that productivity significantly increases in industries that are unprotected and can freely compete, coupled with a modern fiscal system that reinvests taxes into logistics, mobility, and public services. Yet in times of uncertainties, governments are more inclined to erect trade barriers and pursue protectionism, or to alienate the electorate with short-term austerity measures, which distance countries even further from this template of increased productivity—the exact opposite to what should be done to make the future better (Godin & Mariathasan, 2014 ).

As people are getting older, they are also converging: more and more people are living in cities. In 1950, the urbanization ratio in China was 13%. Today, roughly half of the country’ s population lives in cities and the government plans to push that to 70% by 2025 (Johnson, 2013 ). There is a good reason for having more city dwellers: greater urbanization is shown to have a positive effect on gross domestic product (GDP) development. In fact, countries with the highest urbanization ratios are showing the greatest GDP per head of the population (Johnson, 2013 ). Moreover, countries with high populations and levels of urbanization tend to have the strongest GDP growth (Dobbs et al., 2011 ). And while this may seem to be challenged by the progressive hybridized work agenda around the world, there is reason to believe that the recent developments due to Covid19 will not alter or change the course of action of an inexorable intensification of urbanization in the years to come.

Resource Scarcity

Urbanization and the continuous growth of world’ s population size would put a lot of pressure on the use of resources because cities and resources to run them are always co-related. But after years of resource exploitation, dating back from colonialism to our days, resources are now rapidly depleting and dropping in quality, or at least the availability cycle is undermined (Tse, Esposito, & Soufani, 2014 ). Resource scarcity, inevitably, represents another megatrend. Many people relate resource scarcity to energy, thinking that the world would run out of fossil fuels soon. It is true that fossil fuels are nonrenewable.

But there are reasons why the worry is unwarranted. First, there is a huge amount of reserves that is yet to be inventoried. Second, there are always wind and solar energy, which, in addition to the associated sensitivity to shift to clean energies, have become largely available also because of the climatic changes. Water and food, on the other hand, are different stories. At the current consumption rate, according to the World Wildlife Fund (n.d.), it is possible that by 2025 two-thirds of the world’s population may face water shortages. It is not just a matter of not quenching thirst.

As cities becoming ever more urbanized, the increased requirements on sanitation would put further pressure on the use of water and beyond, in what we see as strings of co-related shortages. At the same time, most companies’ value chains would also be deeply affected by water scarcity, across regions, but more so, where manufacturing is still the key driver of production. It takes, for instance, with an average car containing about 2,150 pounds of steel, this would mean over 300,000 liters of water is needed to produce the finished steel for just one car (Grace Communications Foundation, n.d.).

Lately, circular economy, also known as the “cradle-to-cradle” model, is gradually gaining more and more traction as the model of the future, and, hopefully, its inherent regenerative modus operandi will gain more and more ground, carving space for a needed shift to circularity. This is where we believe there will be a dedicated focus towards a sustainability transformation, which will rise from the ashes of the phoenix, in this case, our old models of productions that have been grounded to zero during the pandemic.

Inequalities

The world seems to have woken up to the issue of inequality when the French economist Thomas Piketty (2013) argued in his bestseller that the unequal distribution of wealth in the developed countries has become more so in recent years and since then, it didn’t get any better. The increasing pressure on the systems and the gap becoming inexorably larger, coupled by structural dysfunctions caused by the degrees of implications inferred by the pandemic, our world is more unevenly distributed now than ever. In the past 30 years, the incomes of the wealthiest have surged into the stratosphere (and the higher up in the income hierarchy one is, the greater the increase has been), while the incomes of the large majority have stagnated. This has led to a level of inequality in wealth in the developed world not seen since the eve of the Great Depression (Piketty, 2013). Income inequality—while a serious dysfunction of how wealth should be distributed—is, unfortunately, not necessarily the most acute of the socioeconomic gaps we have analyzed. In fact, just as worrying is that the phenomenon that the middle-income class is gradually disappearing. In the United States, while productivity and GDP have continued to grow, middle-income earners have been making less over time: the percentage of households earning 50% of the average income has decreased from 56.5% in 1979 to 45.1% in 2012 (Bernstein & Raman, 2015).

Worst yet, this “hollowing out” is not only confined to the United States; the same phenomenon is also observed in 16 European countries around the same period (Goos, Manning, & Salomons, 2014). This, as it turns out, is the consequence of automation and computerization (more below). While the middle-class disappearing may suggest a rebalance of wealth toward either poor or rich people, the story behind may present bleaker aspects and nuances. Middle class in modern civilizations is the bearing engine of our economic outputs. In dry terms, it is where GDP is ultimately produced. If the middle class slims itself to the level of becoming marginally relevant, repercussions in the standards of living must be anticipated as likely to happen. The framework doesn’t exclusively mention income inequality as the sole form of inequality, but we tend to believe that a series of socio-economic inequalities are on the rise, even if what seems allegedly to be non-financial matters, such as life expectancy, access to education, gender opportunities, or simply access to healthcare. This is why we believe that the repercussions of widening inequalities in various dimensions of our societies, especially when very little effort has been made to stop it, could greatly impact our future, inferring a trajectory we hope to be able correct, prior to its full deployment in our societies.

Indeed, the current pandemic is most likely going to drive inequality further as a result of the so-called K-shaped recovery: large companies and public-sector institutions with direct access to government and central bank stimulus packages will make some areas of the economy recover fast but leave others out. This comes at the expanse of small and medium-sized enterprises, blue-collar workers, and the dwindling middle class (Bheemiah, Esposito and Tse, 2020). It must be noted that technologies alone are not necessarily solution to reverse this situation. Technologies needed to be complemented with the right government policies and company practices in order to be address these inequality concerns.

Volatility, Scale, and Complexity

The world has not been a tremendously exciting place in terms of economic growth for most of the past two millennia. Such growth really started to accelerate only after the Industrial Revolution. The invention of steam power in mid-eighteenth century, followed by the emergence of internal combustion engine, electricity, and household plumbing about a century later, brought significant economic growth to the world’ s economy (Gordon, 2012).

More recently, the revolution that caused our economy and productivity to take off once again was the advent of Internet technologies (Brynjolfsson & McAfee, 2014). One of the most observed writers in this field, Jeremy Rifkin ( 2011 ), speaks about a third industrial revolution, when the fledging of existing platforms or engines—namely, the energy, communication, and mobility drivers— converge. Indeed, what makes the online technology different from—and far more powerful than—other revolutionary technologies within this integrated view of converging models in the past is the fact that it acts a glue to different types of devices and technologies, often leading something that is novel. Things have changed since then and from the incremental nature of technologies, hassled by the concerns raised by the Moore’s Law, we see today that new forms of deeptech are generating more and more combinatorial outputs and these outputs are giving rise to new priorities ahead.

One outcome emerging from the combined use of these technologies is robotics, which have recently reached a point of intelligence at which they will be able to help humans in every kind of industry, in ways previously unimaginable. The penetration of robotics into regular activities is increasing as we speak, with examples of robotics applied also to biology, in what futurists call the “fourth industrial revolution,” where the combination of biology, robotics, and digital may become a new integrated reality of products and services.

The technological tipping point has been the development of advanced sensors. This has given robots the ability to sense and interpret the world around them (Williams, 2016 ). Just as important is the arrival of cloud computing. Previously, robots would have to learn all by themselves as individual entities. With the possibility of linking them all up to a single source, learning by one can be easily shared with the others. This puts robotics on a very steep learning curve and hence faster developments (Ross, 2016 ). The rise of robotics could, like the earlier Internet revolution, lead to the development of new ecology around robotics, providing plenty of new opportunities. The fast-paced technology development would require businesses to be adaptive, but above all, capable of synthesizing and integrating elements that may learn quicker than the programmer would have ever imagined. And we are just getting started.

Enterprising Dynamics

Technologies are not just fundamentally changing the way we live; they are also reshaping how businesses work. While our research on volatility demonstrates clear orientation toward combinatorial modus operandi, other parts of the world—namely the emerging economies—are living this reality by contextualizing many of these technologies to serve local markets. To many people in the West, China is often viewed as a country unable to innovate and prone to acquiring existing technology from others. This reflects perhaps a natural response that China’s stellar economic rise is partly due to the country’s inclination to assimilate existing Western products and, worse yet, sell fake goods. Yet such view underscores the fact that many people confuse innovation with invention. The Middle Kingdom may not be very good at coming up with products based on its own ideas, but this does not mask the truth that in certain areas it has been doing business with such a level of novelty that Western companies should take as reference. Whereas businesses in the West and Japan remain strong in engineering— and science-based innovation, Chinese firms excel themselves in the customer-focused and efficiency-driven sorts (Woetzel et al., 2015 ). This might sound trivial at first glance, but we imagine that it would be rather difficult in the United States or United Kingdom for online platforms to extend into financial services without running into regulatory concerns or competition from incumbents such as banks (Tse, 2015). Naturally, Western companies do not stand still. Companies of all sizes are taking on new and different entrepreneurial dynamics. For instance, a London-based translation company is now much more of an information technology (IT) integrator with a small set of translation activities. This is not only because computers and software can now do most of the translation; this is also due to large multinational clients demanding full IT integration to their systems. In this instance, these corporations require the translation company to translate all of their invoices into different languages automatically, and all of these must be conducted seamlessly on their platforms. In some cases, while the business model is new, the customers can often tweak it to add a new dimension to the business model, customizing it in some way at every interaction. Compared to the past, one would know if there is actually a demand only when it gets to the stage of getting ready to sell the product to customers. But the entrepreneurs would have to come up with concept, build a prototype, raise the funding, conduct market research, manufacture and hold inventory, and find sales channels and negotiate with them, all of which consumes an enormous amount of time and money. As more and more businesses are now conducted online, it can be expected that there will only be more dramatic and speedier changes in business models and value chains in the years to come.

Discovering the CLEVER way to enact on the meso/micro level of the economy

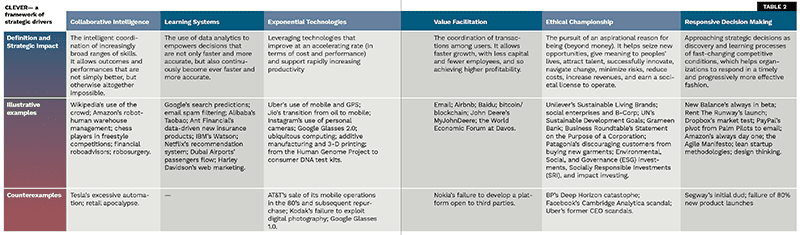

Moving the level of analysis to the meso-level, CLEVER is a framework of strategic drivers, that is the forces that offer strategic advantages and — therefore — trigger strategic change. These six drivers are:

- Collaborative intelligence

- Learning systems

- Exponential technologies

- Value facilitation

- Ethical championship

- Responsive decision making.

The first three elements of the framework represent the ‘hard’ features—the technological components—the following three capture decision-making and managerial styles. Table 2 reports the definition and strategic advantages of each driver, as well as illustrative examples and counterexamples.

Collaborative Intelligence

Collaborative Intelligence refers to the intelligent coordination of a broad range of skills. It is a strategic driver that allows outcomes and performances that are not simply better, but otherwise altogether impossible.

A good example of the power of Collaborative intelligence is the online open encyclopedia Wikipedia. Its content originates from a vast community of contributors from different backgrounds, each of whom offers their own knowledge on a broad range of topics. Some contributors volunteer their editing and reviewing skills. Wikipedia also assign separate tasks to automated bots and to humans, so that each perform the tasks they are most qualified for. For example, bots verify whether new content is plagiarized. They can rapidly compare the percentage of text that identical to that already published elsewhere, and quickly raise a warning if the percentage is too high. Such important work would be too time consuming for humans. However, bots are incapable of editing the text to avoid plagiarism. So, if necessary, a human can step in and execute an informed correction. The diverse skillsets of many humans (a crowd) and bots achieved what human experts alone could not.

Collaborative intelligence does not emerge by simply bundling together different skillsets, but ultimately depends on the process of coordinating them (Malone, 2018; McAfee, 2010). Some examples of Collaborative intelligence are the combination of the skills of humans and machines (Daugherty and Wilson, 2018), the power of the crowds with diverse skillsets, experiences, expertise, and origins (Surowiecki, 2005), and open innovation (Chesbrough, 2003) that leverages knowledge and resources that are both internal and external (e.g., consumer feedback, competitors, universities) to an organization.

Learning Systems

Learning Systems consist in the use of data analytics to process large amounts of data to gain insight and make superior, automated decisions. Even with the simple forms of learning and automation (Davenport and Ronanki, 2019; Iansiti and Lakhani, 2020) in use nowadays, it is a strategic driver that empowers decisions that are not only faster and more accurate, but also continuously become ever faster and more accurate.

At the core of this strategic driver are Machine Learning (ML) algorithms that explore patterns among vast stores of diverse data—ranging from demographic information to spending habits, from social interactions to online search history, from geolocation to personality…—and identify statistical correlations between inputs and some relevant outputs. This way, when they are given new inputs they can quickly and cheaply predict the corresponding outputs (Agrawal et al., 2018).

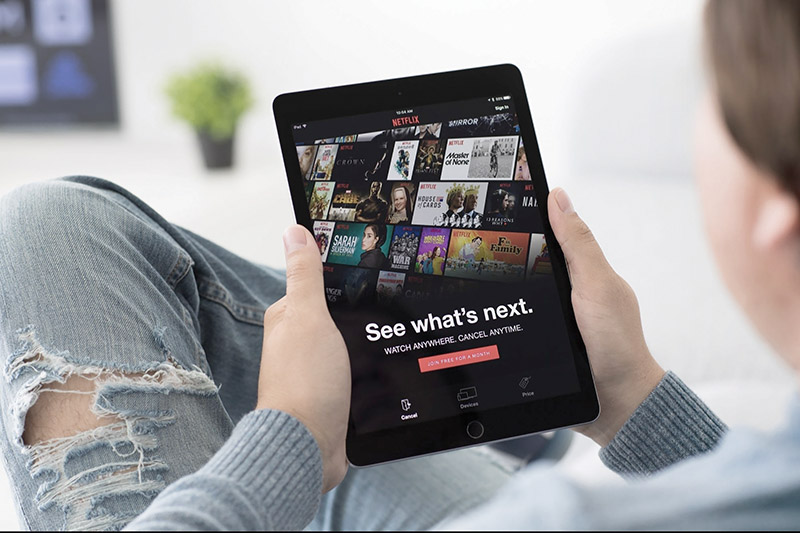

A good illustration of Learning Systems is the video content producer and distributor Netflix. They gather large amounts of data about the viewing behavior and preferences of their subscribers. Netflix’s algorithms can then predict what content each viewer is likely to enjoy each time they login. These algorithms are so accurate that 80 percent of the content streamed on the platform comes from recommendations (Plummer, 2017).

Other content producers shoot a pilot episode before producing new series, in order to test it with its target audience, and gather feedback that helps predict future viewership. Netflix does not shoot pilots. It uses data to choose what new content to produce. Viewers’ ratings of different content, genres, and actors suggested the very successful remake of the “House of Cards” series (Carr, 2013). The success rates of traditional pilot-tested TV shows are 30-40 percent. Netflix original shows’ are 80 percent (Orcan Intelligence, 2018).

Exponential Technologies

Exponential Technologies consists in the leveraging of technologies whose performance improves at an accelerating rate and so support rapidly increasing productivity. Digital technologies — such as digital sensors, computing power, and blockchains — improve very rapidly and the performance improvement of each new version of the technology is greater than all the cumulated improvements until that point.

For example, in November 2019, the best camera phones on the market had a resolution ranging between 12 megapixels (MP) and 48 MP (Wired 2019). Soon thereafter a 108 MP camera phone was released (Kelion, 2019). Similarly, 5G connectivity is expected to transmit data one hundred times faster than the previous 4G standard. As 5G is being rolled out, 6G is already poised for release, with an anticipated connectivity one hundred times faster than 5G.

Besides the speed of release and the accelerated improvements, digital technologies integrate into and reinforce each other, a process called convergence that results in rapidly increasing productivity (Camerona et al., 2005). These accelerating digital technologies are poised to transform “the way we work and consume (commerce), our well-being (health), our intellectual evolution (learning), and the natural world around us (environment)” (Segars, 2018, p. 4). If digital technologies continue improving at this accelerating rate, over the next twenty years we will experience a degree of innovation comparable to that experienced over the last century (Kurzweil, 2001).

Value Facilitation

Value Facilitation refers to the coordination of transactions among users, via a platform (Parker and Van Alstyne, 2016). In a market exchange, value is created between buyers and sellers completing transactions. These platforms do not create value; they facilitate transactions that create value. Value Facilitation is a strategic driver that allows faster growth, with less capital and fewer employees, and so achieving higher profitability. This way, value creation is largely curated by users, often using spare capacity or underused assets. Since users create value for each other (Katz and Shapiro, 1986), the more users participate in a platform, the more valuable the platform becomes. Seven of the world’s twelve largest companies by market capitalization operate a business model of this type (Hirt, 2018).

For example, Airbnb does not directly engage in value creating exchanges. It facilitates exchanges that create value between hosts and guests. Launched in 2008, Airbnb listed one million properties by 2015 (Hagiu and Rotham, 2016), and by 2020 it surpassed seven million listings (Airbnb, n.d.). Marriott, the largest hotel company in the world, took fifty-eight years to get to one million rooms and reached 1.2 million rooms only in 2020 (Trejos, 2018).

Ethical Championship

Ethical Championship refers to the pursuit of an aspirational reason for being beyond money. It is a strategic driver that helps seize new opportunities, give meaning to peoples’ lives, attract talent, successfully innovate, navigate change, minimize risks, reduce costs, increase revenues, and earn a societal license to operate. All this is reflected in the financial bottom line, as companies with a purpose outperformed the S&P 500 by a factor of 14 between 1998 and 2013 (Sisodia, 2014).

Most people believe that “capitalism as it exists today does more harm than good in the world” (Edelman, 2020, p. 12). Curbing the negative side effects of capitalism by embracing Corporate Social Responsibility, or CSR (Carroll, 1991) or meeting a triple bottom line (Elkington, 1994) is not enough. The next, bolder step, requires the deliberate pursuit of dual goals—financial sustainability and positive social and environmental impact (Battilana et al., 2019; Dacin et al., 2011)—to ensure business becomes a force for good.

For example, consumer goods multinational Unilever has a portfolio of over 400 brands, including household names like Axe, Knorr, Lipton, Magnum. In the early 2000’s it began transforming some of its brands, associating them with a purpose. The first such case is Dove, a skin care brand, which started celebrating the natural beauty of every woman, instead of promoting idealized beauty standards embodied by airbrushed models, which cause many girls and women to feel insecure about their appearance. Dove stopped using professional models for its campaigns and instead hired women in a wide range of skin colors and body shapes, to pass the message that real women, with stretchmarks and all, are beautiful. Six months after launch, sales went up 700 percent. Today, Dove is Unilever’s biggest brand. Unilever kept investing in brands with purpose, which it calls “sustainable living brands.” By 2017, more than half of Unilever’s top performing brands were sustainable living brands. Moreover, these brands with purpose grew 46 percent faster than the other brands and account for 70 percent of Unilever’s revenue growth.

Responsive Decision Making

Responsive Decision Making consists in approaching strategic decisions as discovery and learning processes in fast-changing competitive conditions. It is a strategic driver that helps organizations to respond in a timely and progressively more effective fashion to uncertainty. Some examples of Responsive Decision Making are dynamic capabilities (Teece et al., 1997); a learning culture (Garvin, 1993); the lean startup (Blank, 2013; Ries, 2011) and hypothesis-driven learning (Eisenmann et al., 2014) and design thinking (Brown, 2008; Martin, 2009).

To remain successful in fast-changing competitive landscapes, assets must be reconfigured and redeployed and both internal and external structures must be redesigned. Yet, it is not enough to reorganize. Reorganization itself must be reimagined to fit turbulent environments.

For example, GE developed the Durathon battery following an agile approach (Blank, 2013). It began approaching potential customers to explore their needs and expectations, iteratively developing and testing prototypes that, while not ready for the market, helped gather invaluable feedback. In the process, GE abandoned some of its original target customers, identified new market niches, and validated the viability of its Durathon battery before its manufacturing plant was ready. If it had followed the traditional waterfall approach, it would have built a production facility to roll out the new product and then it would have started selling it, only to find out that some of its target customers were ‘wrong,’ and so it would have wasted large resources and then had to fix its offering, at a much greater cost and possibly too late.

Conclusion

To successfully navigate the upheaval caused by the Covid-19 pandemic, business leaders must reconsider their strategy. Two of the key strategy questions they must answer are: where their company will play and how will it win (Lafley & Martin, 2013). This article provides two research-based frameworks to answer these two critical questions.

When answering the first of these questions, DRIVE assists decision makers in tracking the megatrends that shape the competitive landscape and in identifying major emerging opportunities, which traditional tools for strategic planning might only capture when it is too late. For the second questions, CLEVER maps the drivers of strategic advantage decision makers should leverage to maintain a competitive edge. Jointly, the two frameworks constitute the foundation of a new strategic architecture that empower firms to identify growth opportunities and successfully organize to pursue them in the turbulent, post-pandemic world economy.

Although they’ve only been published for less than five years, our frameworks have now been taught in several graduate programs in business schools around the globe and have become the cornerstone of many executive education programs and consulting projects. Despite these accolades, these frameworks do not aspire to be perfect. In turbulent times, with multi-causal patterns and non-linear trajectories of change, the future cannot be predicted. So, even equipped with the DRIVE and the CLEVER frameworks, decision makers might still face sudden black swans and wildcards that lead to unexpected circumstances and rapidly shifting competitive scenarios.

Frameworks should instead be judged for their usefulness. In the years spent researching and refining our frameworks, we have witnessed firsthand how they have been applied in dozens of companies across industries and geographies. Business leaders can use the two frameworks to understand where strategic opportunities emerge, to find inspiration for strategic action, and so ensure their organizations become stay future-ready in the post-pandemic era.

About the Authors

Dr. Mark Esposito is a socio-economic strategist and bestselling author, researching the Fourth Industrial Revolution and Global Shifts. He works at the interface between Business, Technology and Government and co-founded Nexus FrontierTech, an Artificial Intelligence company. He is Professor of Business and Economics at Hult International Business School and serves also as a clinical professor at Arizona State University’s Thunderbird Global School of Management where he oversees the 4IR Initiative. Since 2011 he has been equally a faculty member at Harvard University’s Division of Continuing Education. He is an advisor to the Prime Minister Office in the UAE and a Policy Fellow at UCL’s Institute for Innovation and Public Purpose. He has authored/co-authored over 150 publications, 11 books, among which 2 Amazon bestsellers: Understanding how the Future Unfolds (2017) and The AI Republic (2019). His next book “The Great Remobilization: Designing A Smarter World” with Dr. Olaf Groth and Dr. Terence Tse, will be published in 2022 by MIT University Press.

Dr. Alessandro Lanteri is Professor of Strategy and Innovation at ESCP Business School, he also teaches in executive education programs for Saïd Business School at University of Oxford and London Business School.

An expert educator, he helps executives and students understand emerging technologies like AI and blockchain, and seize the opportunities of turbulent environments. Alessandro works with multinationals, governments, International Organizations, startups and family businesses across five continents. His research regularly appears on top international publishers, including Harvard Business Review and MIT Technology Review outlets, LSE Business Review, World Economic Forum Agenda and Forbes. His latest book “CLEVER. The Six Strategic Drivers for the Fourth Industrial Revolution” became a no.1 Amazon bestseller. His next book, “Innovating with Impact,” will be published in 2022 by The Economist.

Dr. Terence Tse is a professor at Hult International Business School and a co-founder and executive director of Nexus FrontierTech, an AI company. He has worked with more than thirty corporate clients and intergovernmental organizations in advisory and training capacities. In addition to being a sought after global speaker., he has written over 110 published articles and three other books including the latest Amazon best seller, “The AI Republic: Building the Nexus Between Humans and Intelligent Automation“. His next book “The Great Remobilization: Designing A Smarter World” with Dr. Olaf Groth and Dr. Mark Esposito will explore the post pandemic designs as we prepare for the great reset.