")

Globally, more than 15,000 businesses accept Bitcoin. To date, high flyers such as Microsoft, AT&T, Starbucks, Gucci, and Shopify accept Bitcoin in one form or another. As an executive or, for that matter, as an individual and investor, should you embrace crypto or shy away from it?

“Happy Birthday, Mr Bitcoin“

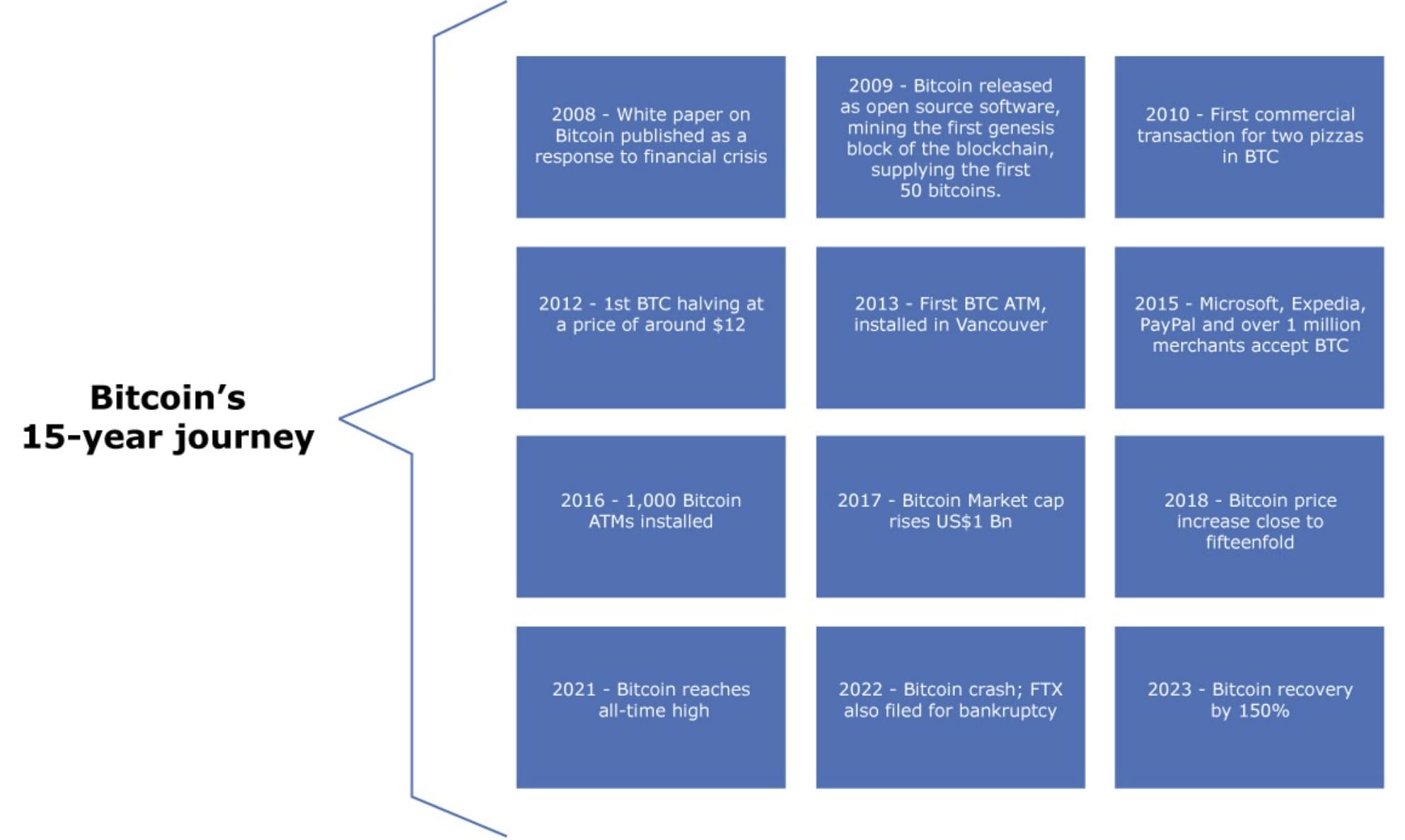

Bitcoin, and cryptocurrencies in general, are peer-to-peer payment networks in which the verification of transactions is decentralised outside of a third “official” party, such as a central bank. Bitcoin has notably just passed the 15-year milestone after its principles were disseminated in a white paper in late October 2008, by Satoshi Nakamoto. In 15 years, the story of Bitcoin is nothing short of a saga (see figure 1), moving to a price of US$12 by 2012, and to US$40,000 more than 10 years later.

Is Bitcoin only a difficult teenager or will it move to adulthood, outside speculation and bubble? The fact that countries are slowly adopting Bitcoin as a legal currency or that massive or high-profile funds such as Ark Invest and BlackRock are applying for a Bitcoin spot EFT are possible testaments to its legitimacy.

The jury is still out. Bubbles have clearly happened in the short lifetime of Bitcoin, and are likely to coexist with fundamentals, depending on the timeline. Further, on the scepticism side, 2022 saw the failure of Celsius and Voyager and foremost FTX after Bitcoin crashed by 80 per cent. Even if it recovered and increased by 150 per cent in 2023, the current price is still about US$25k from its peak by November 2021.

On the optimistic side, though, we once remarked that the demand for Bitcoin is getting stronger and correlates with economic factors that are linked to fundamentals such as inflation expectations, among others. Similarly, on the supply side, one can note that the Bitcoin ecosystem has been around for years now and, while it has seen very large dips (such as after 2013 and 2017), it has always bounced back – stronger. This resilience is a fortiori remarkable when the ecosystem has miners rather exposed, given that their activities are closely linked to the price of Bitcoin, since they own a large stock of Bitcoin in order to ensure the best liquidity in the field and to be able to profit from a significant market rise should the blockchain market turn bullish again. Even during the recent crash in 2022, the gross margins of mining layers such as Argo or Marathon remained largely healthy, above 80 per cent (or at the top of range compared say to SaaS businesses), with operating margins higher than 50 per cent in a sharp downturn scenario, which is significantly above any type of business.

The relevance of bitcoin: three filters

So are cryptocurrencies “useless” bits or are they really useful? We propose three lenses as a way to make sense of the crypto mania.

Empirical evidence

Question: Is there a link between the price of Bitcoin and the potential intrinsic value of the Bitcoin economy?

Let’s start with a few points about how Bitcoin works. First, the supply of Bitcoins is totally inelastic, determined by a protocol, with a fixed issuance schedule that is halved every four years, up to a final amount of 21 million Bitcoins. Second, a new Bitcoin is accompanied by a block that is valid only by virtue of a protocol such as proof of work that someone (the miner) has committed a certain amount of computing power. Agents on the Bitcoin network compete to have their transactions included in the first blocks. Computing power is measured in hashes per second.

These two characteristics of the Bitcoin economy imply that:

- the limited supply of Bitcoins can be anti-inflationary compared to the supply of money from central banks. (Just look at what happened post-COVID after governments issued lots of money to finance economies, and how that created massive inflation afterwards, and that the Bitcoin price should be positively correlated with the supply of money.)

- if the Bitcoin price represents a rational representation of the monetary utility of a medium of exchange, store of value or unit of account, we should observe some relationship between the Bitcoin price and the token velocity (which represents the exchange value) and the stake ratio (which represents the value of the store for long-term holders).

- if Bitcoin is a valuable network, its price should be linked to its users and the hash rate.

As far as point a) is concerned, all you have to do is look at the narrow dynamic between money supply and Bitcoin price growth. However, the correlation is not causal. With regard to points b) and c), a large body of academic research shows that Bitcoin prices evolve as a value network and are the cause of Granger hash rates. Similarly, Bitcoin prices are correlated with staking and velocity ratio.

Socioeconomic data

Question: Can Bitcoin become a powerful social network, even if it’s backed by limited original value?

In fact, and contrary to popular belief, economic history shows many cases where money has been created, even in the absence of an intrinsic source of value. The vast majority of them were, in fact, born of the codification of pre-existing, shared interpretations of debt and credit relations within societies.

Lynette Shaw’s recent work is fascinating, because it shows that, even in the absence of a shared, explicit understanding of Bitcoin’s value, the practical necessity of achieving widespread adoption has finally laid the groundwork for a confrontation with the inevitably social demands of establishing a new currency. Nor should we forget that Bitcoin is unprecedented in its leverage of digital communities, giving it global reach. This is also what my former McKinsey colleagues (Arthur Armstrong and John Hagel, 1996) had long anticipated as online communities, being the most powerful social force of the Internet.

Logical proof

Question: Can Bitcoin prices be uniquely defined as an equilibrium resulting from the behaviour of a rational agent?

Bitcoin has been the subject of numerous economic models. One strand of research has argued that the Bitcoin community can effectively act as a rational force against discretionary government seigniorage. As a private currency, Bitcoin acts strategically as a tool to prevent governments from abusing their citizens.

Another line of research has been to reproduce Lucas’s rational expectations equilibrium in models where the currency would be, as some claim about Bitcoin, necessarily worthless. These economists show that such a unique rational equilibrium can exist, providing theoretical support for the claim that cryptocurrencies are forms of money. Furthermore, the logic may also imply that a central bank, government or active political intervention is not required to stabilise the value of the “supposedly worthless” cryptocurrency, if the protocol can be designed to support a unique equilibrium, in effect replicating the Fisher equation of money

What does the jury have to say?

The above arguments in favour of Bitcoin have the merit of existing.

But are those arguments convincing? Taken separately, they all carry caveats. For example, when it comes to logical proofs, models are just models, and Lucas’s reproduction of general equilibrium is an elegant piece of mathematical work, but it may not take into account the fact that cryptocurrencies are far more volatile than these types of models suggest. According to our own research, long-term cointegration seems to take 5-7 years, implying that equilibrium is at best latent and not visible in a dynamic market such as Bitcoin. Secondly, the use values of cryptocurrencies, such as inflation hedges, etc., always depend on the prior establishment of Bitcoin‘s value by others.

In general, however, the three lenses are highly complementary and demonstrate the strength of the argument that Bitcoin is probably much more than a bubble. In particular,

- cryptocurrency is just one case of blockchain. Blockchain itself is a meta-technology that could democratise finance, for example for real estate, just as cryptocurrency could do in developing markets.

- more importantly, the fact that cryptocurrencies can indeed provide a counterweight to excessive state seigniorage puts governments on a quest for excellence. If this is all that Bitcoin manages to do, it does meet its original aim of ensuring that we are less at the mercy of poor inflationary policy measures.

As an executive, the above suggests that crypto may be more than thin air. There is possibly a lot still to see in order to embrace cryptos, such as other companies have started to do for transactions. After all, those companies represent barely 0.01 per cent of total companies worldwide. Nevertheless, taking an active role in crypto may allow a company to learn and experiment with blockchain, creating a strong optionality for a future of even more decentralised ecosystems.

About the Author

Jacques Bughin is CEO of MachaonAdvisory and a former professor of management who retired from McKinsey as senior partner and director of the McKinsey Global Institute. He advises Antler and Fortino Capital, two major VC/PE firms, and serves on the board of a number of companies.